Oil pulls back as risk aversion takes hold, despite US supply disruptions

Crude oil prices have pulled back in recent days, unable to capitalize on hurricane-related supply disruptions in the US, as the broad-based risk aversion in the markets and concerns over a potential slowdown in China dwarfed everything else. For oil to resume its broader rally it may require fresh and major supply disruptions beyond Iran, or a material de-escalation in the Sino-American trade conflict, which currently seems unlikely.

Hurricane Michael hit the United States mainland on Wednesday, making landfall in Florida and leaving a trail of destruction in its wake. Considering the geography of the region, nearly 42% of crude oil production was shut down in the Gulf of Mexico, as companies evacuated offshore drilling rigs. Yet, despite dominating news headlines, the impact on oil prices was modest, at best. This hails from the fact that 42% of the Gulf of Mexico’s lost output equates to merely 6.5% of total US production, hence representing just a “drop in the bucket” in the big picture. The Gulf’s diminishing importance is owed to the surge in onshore shale production in recent years, which has eclipsed offshore drilling in terms of total output.

Separately, the key speculative factor that has pushed prices up in recent months, sanctions on Iran, was downplayed lately by reports suggesting the US is considering whether to grant some countries a waiver. The sanctions will go into full effect on November 4, but Washington has hinted it may temporarily excuse nations that have already begun reducing their trade with Iran, to give them more time to find alternative sellers.

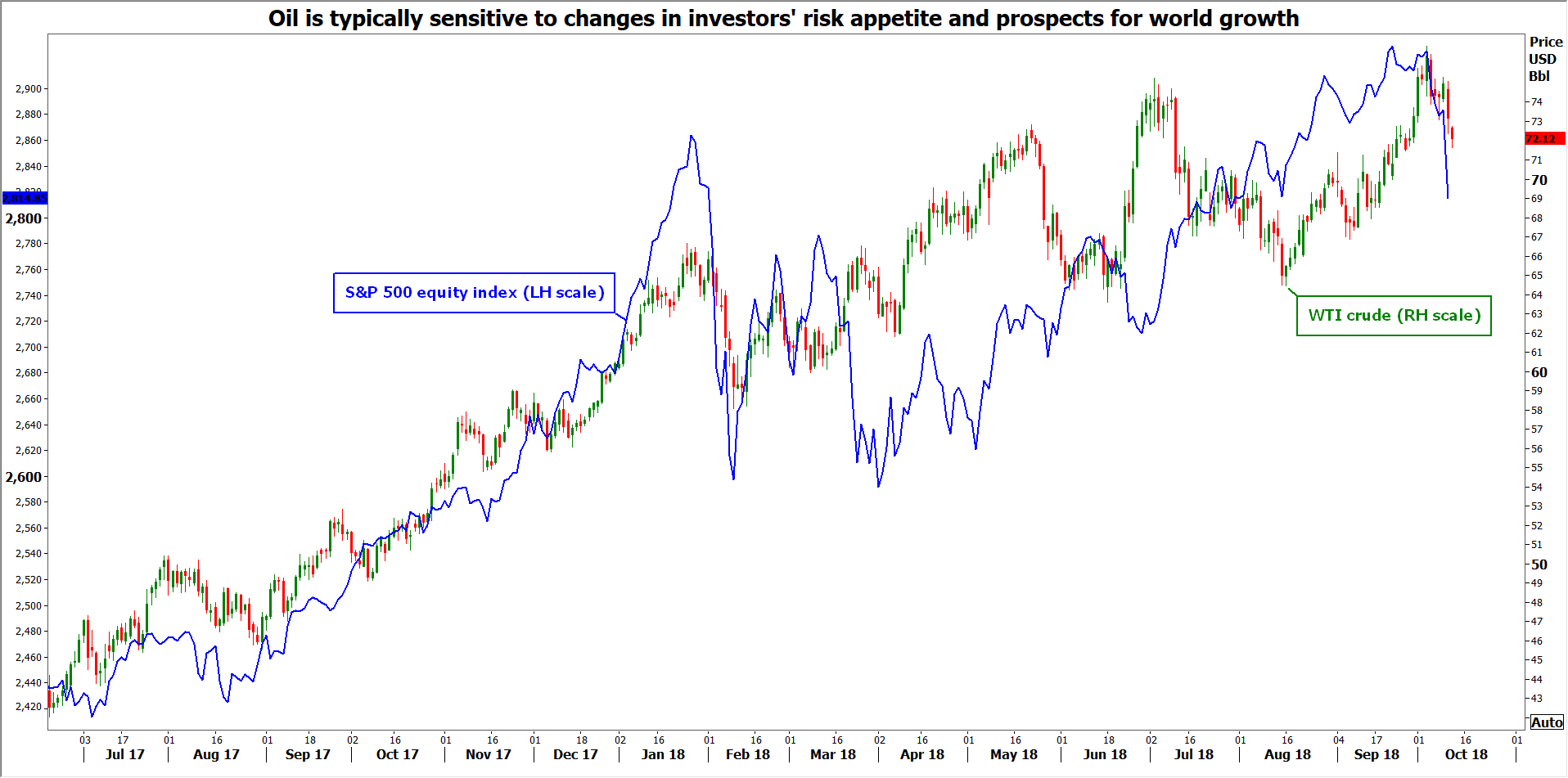

Turning to the demand side, risk aversion engulfed markets in recent sessions, curbing appetite for riskier assets and commodities, including oil. Perhaps more importantly, traders appear increasingly nervous around the prospects for Chinese growth, in the midst of an ever-escalating trade conflict. Such concerns are evidently felt among Chinese authorities as well, which eased monetary policy a few days ago and hinted at fiscal stimulus in the pipeline to support the economy, in a sign that they expect a prolonged and possibly damaging trade battle themselves. With China being the world’s largest importer of oil, any material economic slowdown would have sizable consequences for demand and thereby, for prices.

Overall, the above developments cast doubt on recent calls by several pundits for oil prices to rally towards the $100/barrel neighborhood soon. Major and unforeseen supply disruptions – beyond those from Iran that are already well-priced into the market – would probably have to materialize for crude to rally from current levels. Likewise, it may take a de-escalation in Sino-American trade tensions to brighten the outlook for demand and push prices higher, which seems quite unlikely at this stage considering the recent rhetoric from the US and reports of tensions on noneconomic fronts too. In the more immediate-term, oil’s fortunes may hinge mainly on the evolution in investors’ risk sentiment and the performance of equities, given the liquid’s risk-sensitive nature.

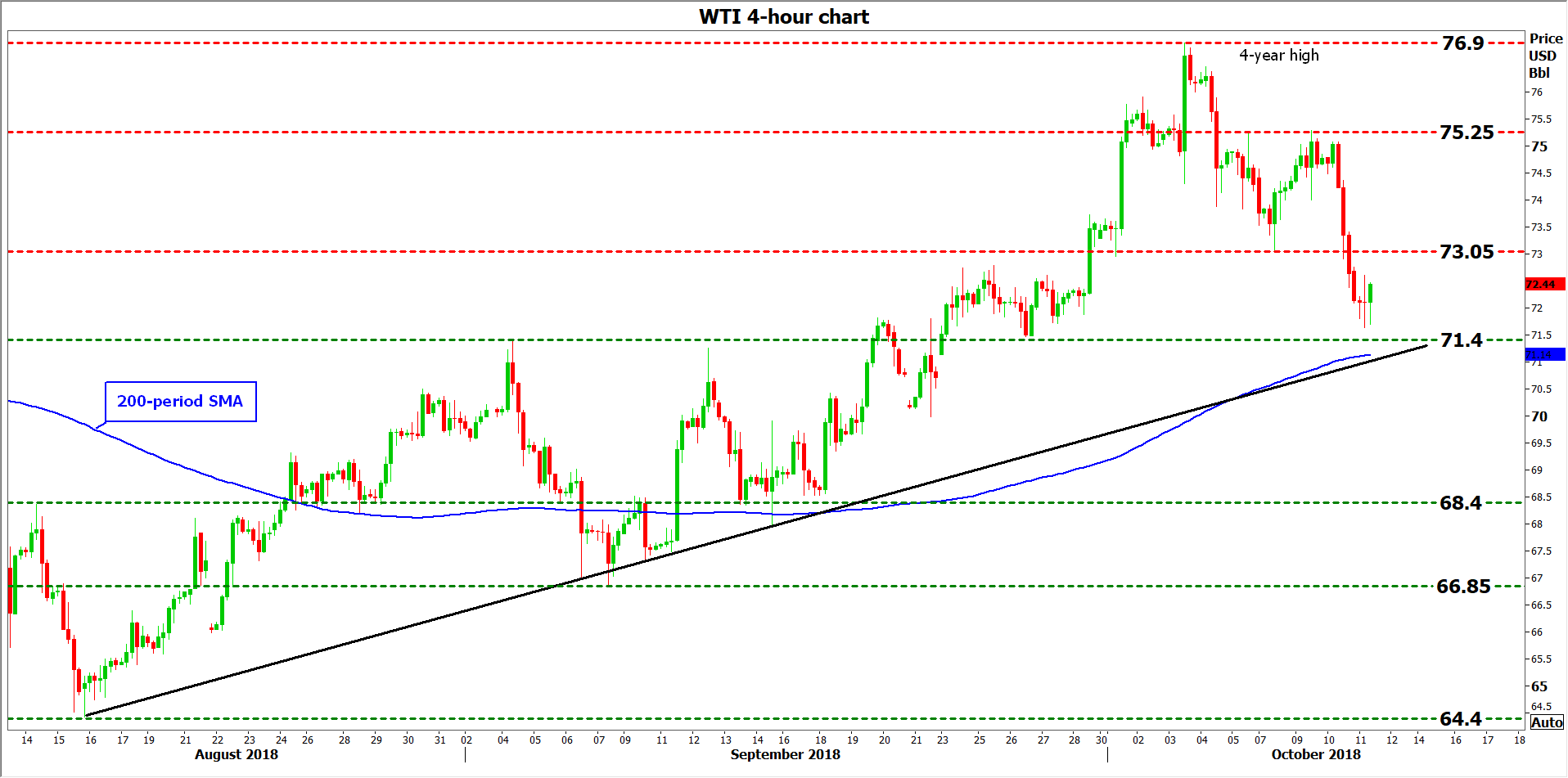

Technically, the picture is much brighter, as WTI continues to trade above both a long-term uptrend line drawn from the lows of June 2017, and a short-term upside support line taken from the troughs of August 16. Moreover, the fact that prices recorded a fresh 4-year high last week reaffirms the positive outlook. A potential rebound in WTI could encounter immediate resistance around $73.05, a zone marked by the inside swing low on October 8. An upside break could open the way for the October 9 peak of $75.25, before the 4-year high of 76.90 comes into view.

On the downside, a first line of support to declines may come near the crossroads of the $71.40 area and the uptrend line taken from the lows of August. If the bears manage to pierce it, that would turn the short-term outlook to neutral (from positive), paving the way for a test of the $68.40 hurdle that halted the decline on September 13. Even lower, the September 7 lows of $66.85 would increasingly attract attention.

Author

Marios graduated from the University of Reading in 2015 with a BSc in Economics and Econometrics. Prior to joining XM as an Investment Analyst in December 2017, he was providing financial analysis, reporting and consulting service