Nationality at the ECB, does it matter?

How do ECB speakers from northern countries compare to their southern counterparts? Bert Colijn and Timme Spakman team up with the ILO's Ekkehard Ernst and Rossana Merola to find out, as Christine Lagarde takes the reins from Mario Draghi as head of the central bank.

As Christine Lagarde starts her term as president of the European Central Bank, there is growing curiosity about how her tenure will differ from that of her predecessor, Mario Draghi. Simple stereotypes around nationality suggest that monetary policy in the eurozone may indeed take a different turn. The theory goes that central bankers from the north of Europe are more focused on the inflation target and less worried about supporting growth while the opposite is said to be true for central bankers from southern Europe.

But is there any truth to these assumptions? To find out, we studied the speeches given by ECB Governing Council members, which consist of the governors of the national central banks of the 19 eurozone countries and the Executive Board members, including the president. We have categorised themes that these central bankers discussed and have found that:

Northern governors prioritise monetary policy issues compared to southern central bankers. Differences between northern and southern central bankers increased in the aftermath of the crisis when southern governors intensified discussions on growth and labour market issues.

French governors are closer to their northern colleagues than their southern ones in terms of topics discussed.

However, the differences between the northern and southern central bankers are much less clear once people are on the ECB Executive Board as opposed to being the governing council member for their respective countries.

How to define differences between central bankers

There are many ways in which you can define differences between central bankers. A straight-forward way is to collate their opinions on monetary policy on the respective central bank boards. In the UK, the position of the Monetary Policy Committee members on monetary policy decisions is known in most instances, which has allowed for detailed analysis. This is not the case for eurozone central bankers, which makes the discussion about the intrinsic nature of central bankers more qualitative.

A possible resource available is the large list of speeches that central bankers give. In recent times, central bankers have taken on a more public role, which includes more frequent outreach in terms of speeches. Communication has proven to be an effective tool to complement monetary policy.

In this brief, we follow the methodology of Ernst and Merola (2018) to determine topic intensity of central bank speeches. Defining topics of interest in speeches provides insight into which drivers determine monetary decision-making. As Ernst and Merola find, overall communication of speakers on inflation and economic activity is in line with policy measures undertaken. That means that topic intensity of speeches gives interesting insight into policy preferences regarding monetary policy. With that, we can aggregate speakers from northern and southern eurozone countries to see whether there are indeed differences in terms of policy priorities between countries.

How to determine the relative intensity of speeches among central bankers

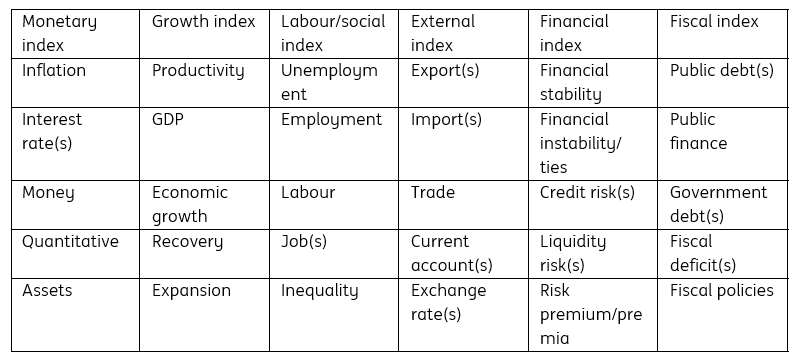

We use the following themes to compare northern and southern eurozone central bankers: monetary, fiscal, financial, labour, external and growth.

The monetary theme captures the intensity of discussion of inflation and other issues surrounding price stability and monetary policy actions to achieve this. This theme is closest to the ECB mandate of inflation targeting.

The fiscal theme centres on public debt concerns and fiscal stimulus.

The financial theme focuses on possible risks to financial stability in the economy.

The labour theme is similar in as much as it relates to cost pressures stemming from labour market conditions. While the unemployment rate is a specific target for the Federal Reserve, it is not for the ECB.

The external category focuses on exchange rate stability and external competitiveness of the eurozone economy.

Finally, the growth theme focuses on economic conditions, which can be taken as an important driver of the inflation target but is not, in itself, the main target of ECB policy.

While the monetary theme is the most obvious one for ECB speakers to address, the others are important issues that are relevant to the monetary environment and should influence central bankers' policy decisions. Differences in the weight given to these themes suggest which issues are top of mind, which can reveal differences between northern and southern central bankers. To assess this, we have looked at the relative intensity indices of Ernst and Merola with slightly adapted keywords used to determine the values for the indices. The indices capture how much themes have been discussed in a speech relative to each other. If a theme captures 100%, it was the only theme discussed in the speech. If two themes are at 50%, they were discussed an equal amount, while the other themes were not discussed at all.

Table 1 Convergence in unemployment has hardly returned after the end of the crisis

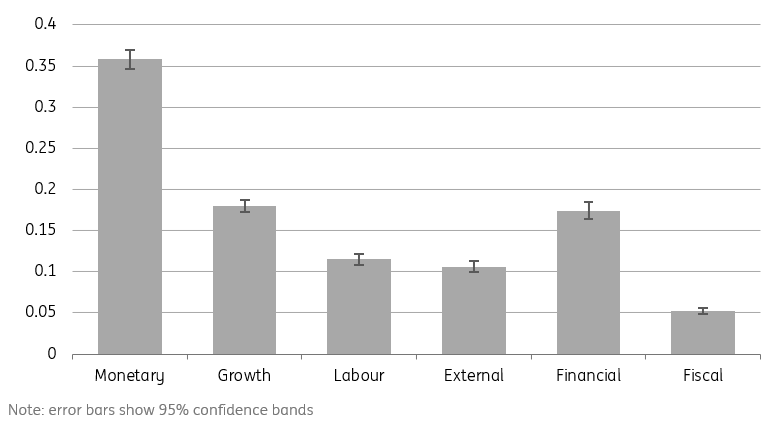

In general, we find that monetary tools and targets are the most discussed themes among ECB governing council members. This fits with expectations of what central bankers should be focused on. We find that the next highest intensity of topics discussed relates to growth and financial stability.

Fig 1 Monetary tools and targets are the most discussed theme among governors

What is northern and what is southern?

The public debate suggests that it is easy to discern bankers from the north or south of the eurozone. In practice, however, the lines between them are not easily distinguishable. To be sure, most people often just focus on the bigger countries, and when we look at speeches from the eurozone as a whole, we find that those countries usually have the most vocal central bankers. There is little doubt about Germany, the Netherlands, Austria and Finland as typically northern when it comes to central banking, with public opinion assuming they take a hawkish stance on monetary policy issues. Spain, Portugal, Greece and Italy are intuitively southern or dovish, focusing less on inflationary concerns or the state of public finances and more on the real economy. France seems to be less easy to classify when it comes to this somewhat arbitrary division, which is interesting given the new ECB president's nationality.

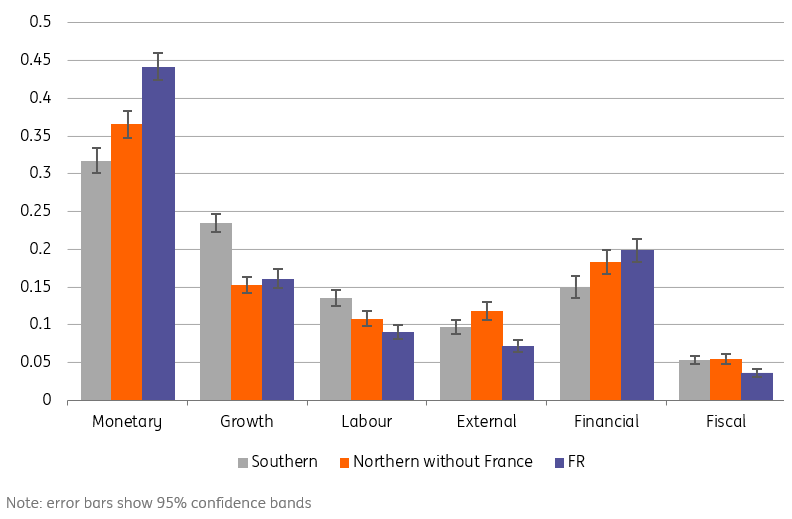

Fig 2 French governors resemble their northern colleagues most in speech topics

Even though French central bankers are generally considered to be less hawkish than their more ‘northern' colleagues, the difference in topic discussion in speeches is not all that different. As Figure 2 shows, French governors have an even higher relative intensity of discussing monetary topics than "northern" governors, while it is very comparable in terms of growth issues. French governors also discuss financial issues more than the average northern governor and discuss labour and social issues less than northern governors. In that sense, the perceived difference between France and northern eurozone countries in terms of central bank policy preferences does not relate to the issues that are top of mind for governing council members. From a speech perspective, we therefore categorise France with the northern countries.

Table 2 The country division used in the below analysis

Do we find differences between northern and southern ECB governors?

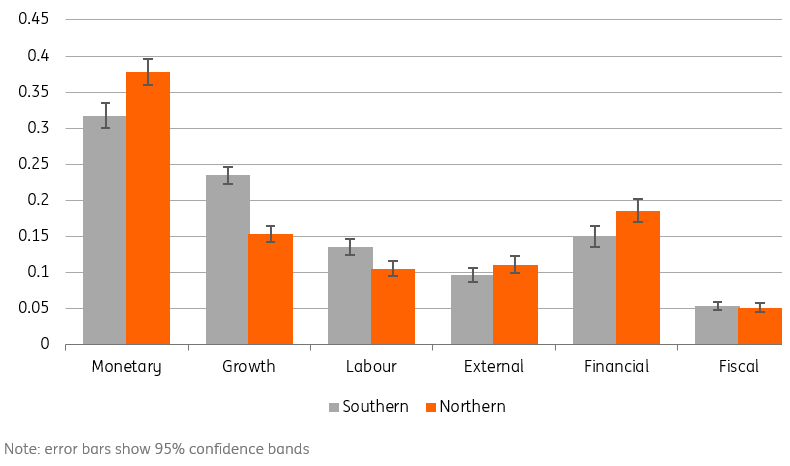

We split our analysis between the national governors on the Governing Council and the Executive Board members. When looking at the relative intensity of different themes between governors, we find that northern governors do speak more about the monetary topic than their southern colleagues. While it is the most discussed theme for both northern and southern governors, it dominates among northern speakers. For southern speakers, the growth theme follows quite closely, with relative intensities of 32% and 23%. In the north, the differences are much larger with 38% for monetary, 19% for financial and just 15% for growth.

Fig 3 Northern governors focus more on monetary themes, while growth is more discussed by southern governors

The financial topic ranks third for both northern and southern eurozone governors, indicating that financial stability is a very relevant concern for all governing council members. Labour and external issues rank below that for both the south and north, but labour is more important to southern governors. Given the deep unemployment crisis that most southern countries have experienced, this seems logical. The more export-oriented northern economies see a bit more interest in the external topic, although it does rank rather low. The least discussed theme is fiscal, which ranks last for both sets of governors with no significant differences between both groups of speakers.

Has the focus of ECB governing council members changed over time?

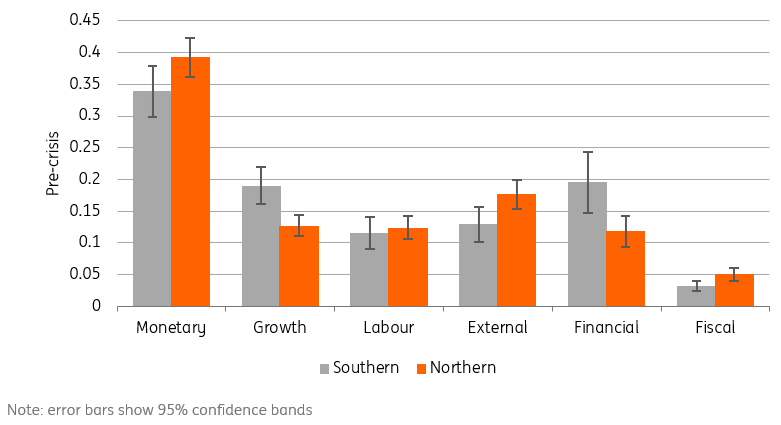

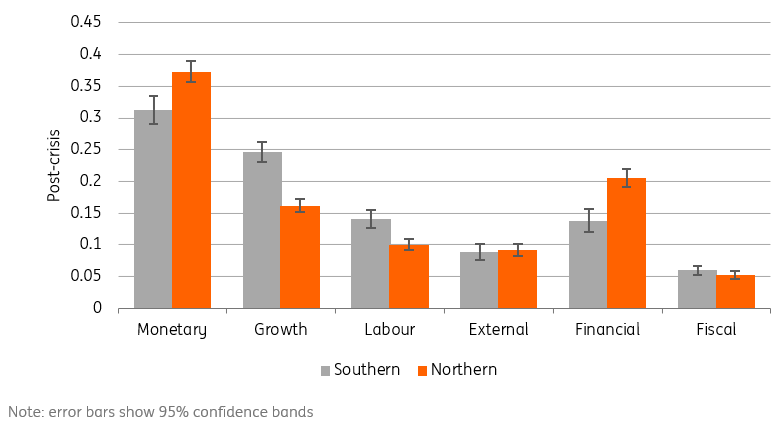

Splitting up the sample between the pre-crisis and post-crisis period (1Q 1997-4Q 2007 and 1Q 2008 until 2Q 2019, using the start of the 2008 recession as the cut-off point) generates some interesting results. Quite significant changes have happened in terms of emphasis in speeches since the crisis period. The larger relative intensity of monetary issues discussed by northern governors compared to their southern counterparts has become significant in the post-crisis period. The difference between north and south on growth issues has also become larger with even more discussion of the theme for the south. Labour issues were discussed evenly between the south and north, but the south has seen a significantly higher percentage of speeches discuss this issue since 2008. The differences between monetary and growth issues discussed between northern and southern governors have therefore intensified since 2008.

The importance of exchange rate stability has declined for both northern and southern governors. In the period leading up to the crisis, this was a big theme among speakers in both the south and north, but it was a particularly large issue among northern (in general more open and trade-oriented economies) eurozone governors, as it ranked second after the monetary topic. Looking at the current period, we find that the relative intensity of discussions of the external theme has fallen significantly and that, outside of the fiscal theme, it is now the least discussed topic for both northern and southern speakers.

Fig 4 The differences between south and north were less significant pre-crisis

Another big difference is around the financial theme. In the post-crisis period, it ranks very high among northern speakers at 20%, making it the second most important topic addressed in speeches. That reveals a more conservative focus with regards to monetary policy as concerns about the stability of the financial system have taken a more prominent place in central bank communication for northern eurozone speakers. This is not the case for the southern speakers though, where the relative intensity of the topic has in fact declined from 20 to 14% while focus on economic growth and labour market issues increased.

Fig 5 Differences post-crisis have increased, with labour and growth more discussed by southern governors and financial and monetary more discussed in the north

For the southern governors, the big shift between periods has occurred in discussions of growth relative to financial stability issues. In the most recent decade, the growth theme has gained prominence at the expense of financial stability discussions as the deep crisis has left large scars on the southern eurozone economy. The theme also saw an increase in the north, but not as much as the financial issue gained prominence, for example. All in all, the differences in performance of home economies seem to have had an important impact on the prominence of themes discussed in speeches.

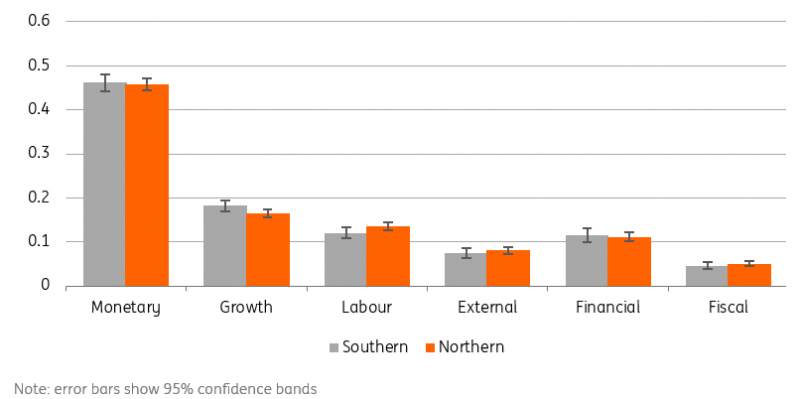

Among board members, the picture is less clear

When looking at the ECB board members, the differences between the north and south become negligible as Figure 6 shows. In fact, there is no significant difference between the southern and northern board members in terms of topics discussed at a 5% confidence level. Of course, board members are somewhat limited by the specific topic they are designated. Think of ex-board member Sabine Lautenschläger for example, who is also responsible for the single supervisory mechanism (SSM) and therefore is likely to focus more on financial stability than other topics in her speeches. Still, the fact that the differences between southern and northern speakers disappear when one considers Executive Board members instead of Governing Council members, indicates that the focus of board members is less country-determined than one might think. Whether the converging themes discussed lead to converging policy preferences is a different story though...

Fig 6 Differences between southern and northern ECB board members are mostly insignificant

For the incoming ECB president, this means that country preferences are not likely to play an overly large role in decision making over the coming years. Typically, French governing council members already focus on monetary topics quite a lot in their communication, so that would not be a large shift from the kind of speeches we have seen from previous ECB presidents. Then again, Lagarde has never been a governing council member and is therefore somewhat of an unknown force. At her hearing at the European Parliament, Lagarde focused mostly on the monetary mandate with some mention of inflation, but also included a lot of references to labour and social issues and even climate change. More recently, she urged countries with "room to manoeuvre' to act, referring to fiscal stimulus. In light of the boundaries of monetary policy that are likely to be tested in Lagarde's term, the fiscal theme may become more prominent in central bank speeches. Perhaps this could be an atypical president after all...

Read the original analysis: Nationality at the ECB, does it matter?

Author

Bert Colijn

ING Economic and Financial Analysis

Bert Colijn is a Senior Eurozone Economist at ING. He joined the firm in July 2015 and covers the global economy with a specific focus on the Eurozone.