More NDX leadership

S&P 500 duly rallied on CPI data as per my premium predictions, confirming what I said the day before about bond market buyers. Tremendous series of intraday gains and directional calls with levels for swing traders continues...

Let‘s unlock the macro assessment driving the gains, these exact predictions (I‘m leaving today‘s PPI part out, and will publish it likewise after the fact).

(…) Core CPI is likely to come below expectations, and whether we get exactly 0.3% or even 0.2%, it‘ll make stocks and risk assets rally into FOMC, where the conference delivery of no hike and cosmetic dot plot changes to the marginally hawkish side with plenty of conditionals mentioning slowing job market and real economy (forget NFPs establishment headline, look under the hood and at JOLTS, uenmployment claims and wildly diverging household survey) would provide for reversal of selling into initial enthusiasm of no rate hike being 2024 imminent.

Look at what kind of clarity of message delivery Powell achieved. Was he trusted on one rate hike in 2024, or did markets still think two? Was he clear on PCE inflation targeting? Little wonder that stocks gyrated so wildly during the conference, before focus turned on good tech earnings, AVGO – and that‘s what contributed lion‘s share of our very latest gains.

If you looked at equities, bonds and the dollar yesterday, what was a greater driver? CPI or FOMC? Here are the inflation readings and what kind of moves they spawned across the three assets, and how these moves were then merely retraced during Powell.

Today‘s premium predictions continue with PPI – it‘ll seal the inflation path message and override the impact Powell had on rate cutting bets as these moved from 28% after CPI to 38.5% now (Russell 2000 of course bound to underperform and short end of the curve was bought at expense of longer dated maturities).

The PPI prediction yesterday finished the above quoted paragraph with „The inflation on the back burner theme would be reinforced by tomorrow‘s PPI interpretation, sending stocks and precious metals higher.“

CPI really came on the low end, and when for now corporate earnings don‘t disappoint, profit margins are good, but revenue is struggling, that means that input costs aren‘t rising too steeply. If you look though at latest hourly earnings, these are up, above expectations, so that results in more of a PPI opportunity to surprise on the downside today, which would be greeted with Nasdaq led upswing continuation applying to S&P 500 as well.

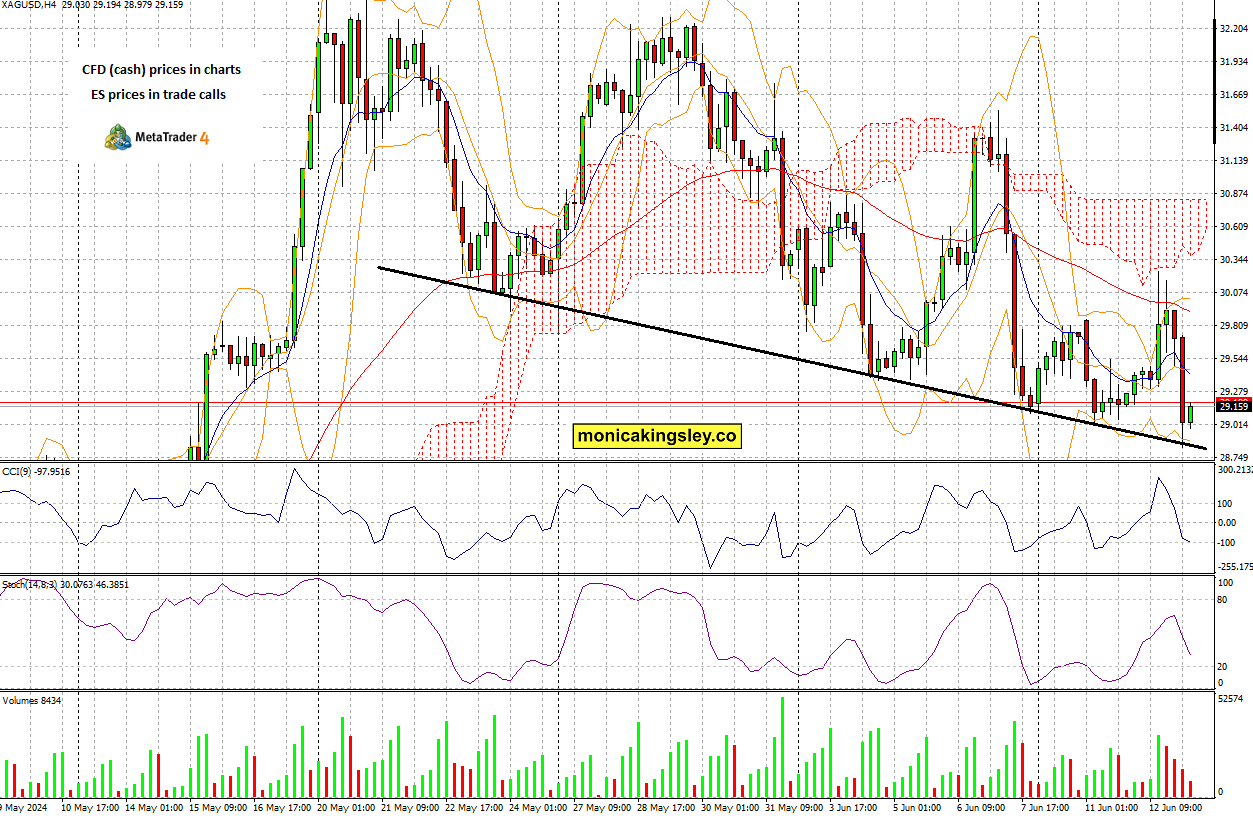

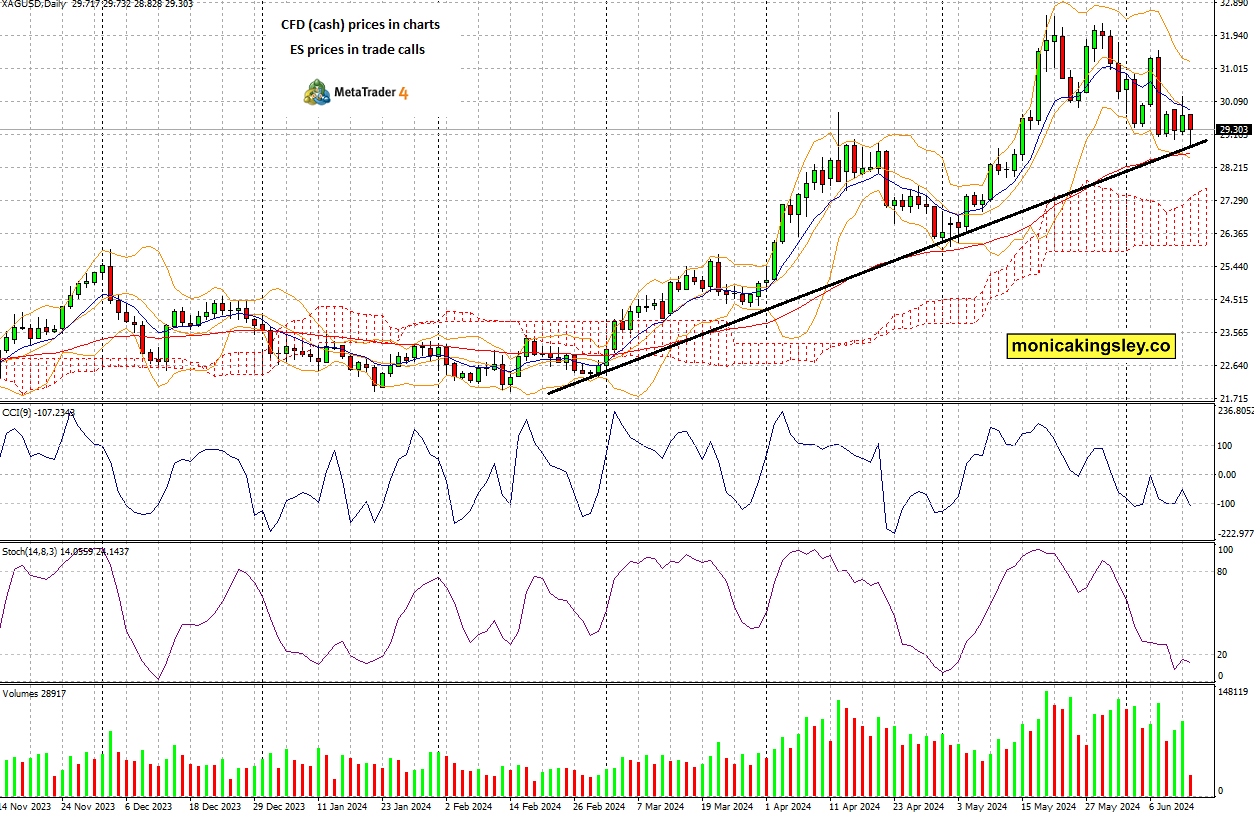

Today‘s free analysis features silver heavily as we had seen an important technical development in the Asian session.

Much Telegram and Twitter live commentary follows as always.

Gold, Silver and Miners

Instead of the usual precious metals chart, I‘ll feature two silver ones, and say that gold is displaying bullish divergence as it didn‘t fall below Friday‘s close, leaving the possibility of slamming below $2,270s in doubt, and keeping above $2300 as more probable. Given the gold silver ratio looking to go silver‘s way towards the end of the month, that would leave more appreciation potential with the white metal, as soon as these two support lines (on the 4hr and daily charts) are proven to have held (both posted earlier today in the premium Trading Signals channel).

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.