Markets reeling from turbulent week last week; global economic growth data the focus this week

Friday’s trade caps off turbulent week: Friday’s trade ended a turbulent week for financial markets, and on balance, amounted to another bearish day for stocks and other risk assets. Global equity indices racked-up losses, while growth sensitive currencies, commodities and credit-assets traded mixed. The news the punditry is pointing-to in order to explain the lacklustre market sentiment was, first: the announcement by US President Trump’s administration to delay extending licenses to US businesses permitting trade with controversial Chinese mega-company Huawei; and second, released later-on in the day’s trace, news that the US President was open to cancelling upcoming trade-talks between the US and China in September.

Fears linger about trade war and global economy: Those headlines ostensibly compounded concerns about the state of US-Sino relations, and enhanced the probabilities that the trade-war would act as a tightening straight-jacket on global economic growth. Such fears certainly appear rational. UK GDP data was released on Friday night for one, and – although clearly just as much a product of ongoing domestic political-turmoil, as it is any global-phenomenon – showed a surprise contraction in quarterly growth. Investors are almost certainly operating in an environment whereby the flame-of global economic activity is dimming. Hope remains of a central bank engineered turn-around, or at least soft-landing, but judging by Friday’s price action, the odds of that are slimming.

Sentiment isn’t as bearish as what it seems: That doesn’t preclude a turnaround in market fortunes in very short-term, however. And although global equities did put-in quite an uninspiring performance on Friday, things probably looked a little worse than what they were. A few mitigating factors need to be considered right now when assessing market-behaviour. Activity in markets is a little thinner than usual, owing to the August-holiday season in the Northern Hemisphere. As much could be witnessed on Friday, with volumes below average across global stock markets. The VIX did lift, showing sentiment was slightly pricklier, relatively speaking. But the resulting moves to the downside are probably being exaggerated by less bums-on-seats in global trading-floors.

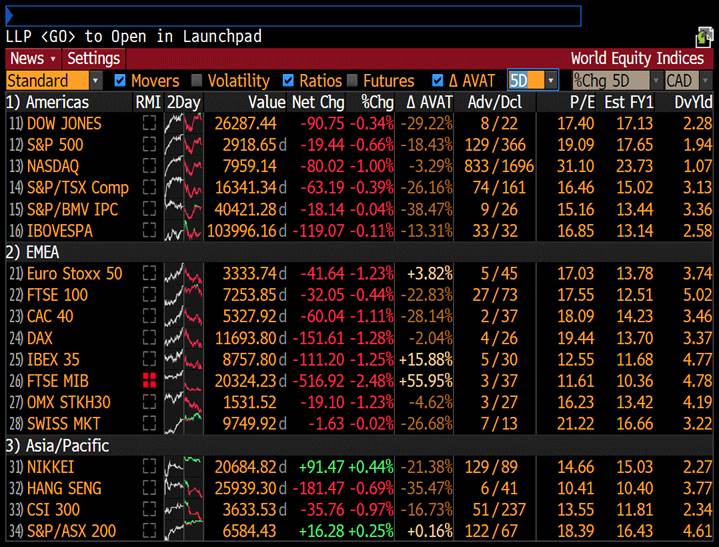

Not quite risk-on, not quite risk-off: This doesn’t dismiss the tumult of earlier on in the week, last week. That was genuinely high-octane selling, driven by a generous dollop of panic. The point is Friday’s action ought not be seen as an extension of that for stock-markets. Again: fundamentals are still eroding, and the outlook is looking bleaker. However, jumping the gun and suggesting the 0.5 per cent to 1.00-plus percent losses sustained by the S&P500, DAX and FTSE was another day of terror-on-the-trade-floors would be very misleading. Case-in-point: global bond yields were generally unchanged in global markets to end the week, suggesting there was no additional drive to safe-haven assets.

Commodities and currencies ended week mixed: Gold was also marginally lower, oil prices climbed as the Saudi’s promised to stabilize the market, copper dipped, while the Japanese Yen and Swiss Franc is powering forward as the trade-war-risk hedges of choice, as China proxy currencies, like the Australian Dollar, look liable to further downside. Because of this mixed behaviour, many are calling Friday’s trade in stocks a day of taking profit from the mid-week rally. That’s a convenient, but perhaps true-enough assessment of the state-of-affairs. Futures markets are pointing to another day today of much the same too, although those prices are failing to discount a weekend’s worth of information.

ASX to start week on the back foot: The ASX200 ought to open 22 points lower, for one, backing up a day in which our benchmark stock index was one of the few strong performers in global markets on Friday. We caught the tail-winds of a solid lead from Wall Street the night prior, that disproportionately benefited bank stocks, and managed to obscure what was an otherwise neutral day for Australian equities. The highlight of our session was the RBA’s Quarterly Monetary Policy statement, which revealed a downgraded set of domestic growth numbers, and hinted that interest rates will remain low in Australia for what appears to be a number of years yet.

Growth data presents as key theme this week: The week ahead becomes about global economic fundamentals. The UK’s growth-data established the tone quite adequately: market participants are going to be perusing the detail of a series of high-impact data, to reprice for what is beginning to look like are more imminent global economic slow-down. A series of European GDP numbers are released, with the German set of numbers expected by many to show a growth contraction. US Retail Sales numbers are printed, and will be used to gauge how long left this US economic cycle has to run. While at home, punters will be keeping close watch on jobs data Thursday, and wage-growth data on Wednesday.

Author

IGMarkets Team

IG Markets, Inc.