Market update: Q2 GDP numbers for the Eurozone and Germany

Improved demand for risk boosted Wall Street overnight and weighed on Treasuries amid myriad crosscurrents. The markets are busy repositioning in the last week of July now that the Fed is safely out of the way with little likelihood for a tapering announcement until at least November. The miss on Q2 GDP was overlooked as inventories were the major culprit, while the surge in the price indicators to near 4-decade highs added to the pressure on bonds.

The focus turned back to earnings, data, the Delta variant, and the infrastructure deal out of Washington.

Good earnings news in general supported stocks with the USA30 and USA500 leading the way with gains of 0.4%, while the USA100 rose 0.1% as concerns over guidance from heavyweights, including Facebook and Paypal (beat earnings estimates, but guided lower), limited enthusiasm. Amazon’s online sales growth is slowing as lockdowns ease. Amazon’s core online store business disappointed, since it grew 15%, the slowest rate since 2019, despite it bringing forward its flagship Prime Day sales event to June. In Europe, GER30 and UK100 futures are also down -0.7% and -0.6% respectively.

In FX markets: EUR and GBP corrected against a stronger USD, leaving EURUSD at 1.1877 and Cable at 1.3980. USDJPY lifted to 109.60, although the Yen was steady to higher versus most other currencies. USOIL is at $73.38 per barrel. Gold was little changed at $1,831.

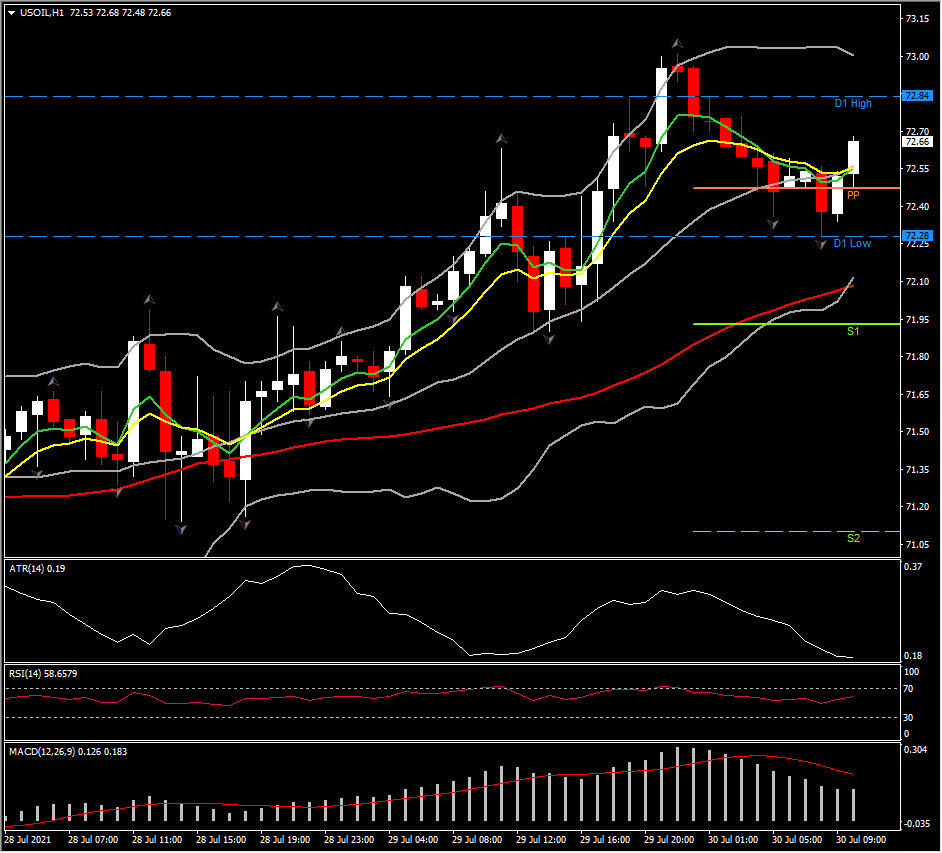

US OIL’s rally to 2-week highs over $73.20 on tight US supplies helped the CAD today as well. The market ignored the small uptick in Canada May average weekly earnings. USOIL stabilized at 72.60 today while PP is set at 72.45 and Resistance is at 73.00 and 73.30.

Today: The calendar is busy and focuses on Q2 GDP numbers for the Eurozone and Germany, which is expected to show a strong rebound from the contraction in the first quarter, while preliminary HICP readings could come in higher than anticipated, after strong German numbers yesterday. US CPI is also on tap, and it should decline -0.8% in June following the -2.0% May drop. Spending is forecast rising 0.9% after the unchanged reading in May. Weakness should result in a -5.5% decline in “current transfer receipts” after an -11.7% May plunge, as this measure tracks the pull-back in stimulus spending. This will more than offset the 0.5% rise in compensation. The savings rate should fall to 10.8% from 12.4% in May and a 27.6% peak in March.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in