Market throws back in Fed's face a fairly good clue about next rate hike

Outlook:

The Fed offered the market a fairly good clue with the next rate hike "fairly soon," but the market threw it back in the Fed's face. We say this is bold, for the Fed, but traders wanted a stronger statement of intent. This is silly. The Fed never offers clear intent. It's always a guessing game.

El-Erian says the market is underpricing the odds of the March hike. We agree. The Fed prefers to sound cautious and swaddle its key comments in so many blankets you can't see the baby. Still, the odds of March fell to 34% from 36% a week ago. June is a dead cert at 76% but May is now coming up on the inside rail at 61.8% from 58.7%. Bottom line—May or June, but not March.

Disappearing into the pond with barely a ripple was a comment by TreasSec Mnuchin that the strong dollar is a "good thing." Analysts were quick to point out he was referring to the Big Picture and not any specific level right now.

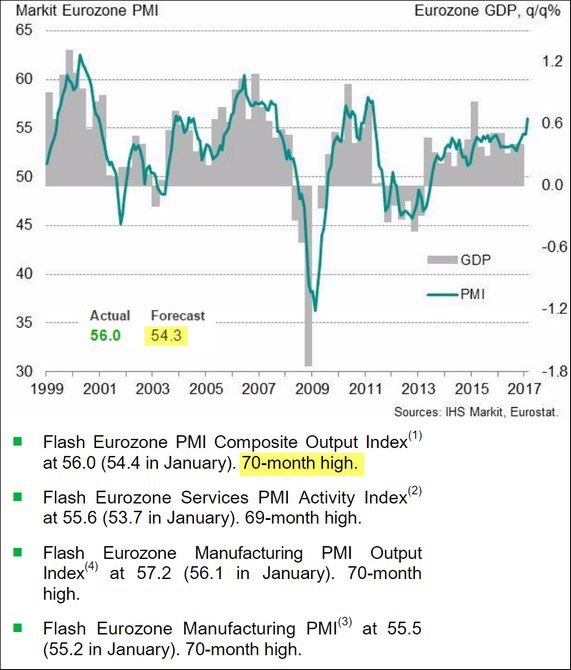

The data out of Europe is stupendously good. Germany just confirmed it has the fastest growth of all the developed countries, including the US and UK. And there is no more deflation in the eurozone—every member has a positive reading and the Jan y/y is 1.8%. Pressure on the ECB to end QE must be building.

The chart below is from The Daily Shot. We showed something similar a few weeks ago. The point: Europe is no longer sclerotic. Growth is more vibrant than in the US, and this counts—over long peri-ods of time, the country with the higher growth gets the higher currency.

What's holding the euro back, so far, is nerves frayed by political considerations. Reuters reports the 2-month implied volatility of the euro at "the highest in a month as contracts took in the first round of the election in April. But the 3-month equivalent was down slightly from post-Brexit vote highs hit on Wednesday, bolstering spot prices for the euro."

"A poll showing French far-right leader Marine Le Pen was only 10 points behind conservative François Fillon but 22 points behind Macron in the potential second-round run-offs was not enough to knock the single currency backwards." A Swedish analyst told Reuters "It will be interesting to see if the euro continues to be dominated by French politics. That has certainly been the case in the last few days."

The latest chapter has "veteran centrist" Francois Bayrou allying himself with Macron rather than stand himself, which would boost Macron at the expense of Fillon. Got that? This new alliance casts doubt on the latest polls taken beforehand that show LePen the favored candidate. She would win against both candidates in the first round, but lose the May 7 runoff to either guy. Now that both guys are in it together, she could lose the first round, too. Reuters reports a BVA poll showing "Macron beating Le Pen comfortably, by 61 percent to 39 percent, in the runoff vote."

We do not claim to understand French politics, but this latest development implies that pushing back the Far Right has become a serious job for the centrists, to the point where one of them took the ego-bruising path. This "should" be euro-positive to the extent that worries about Frexit were behind weak-ness, and sure enough, by 8:15 am this morning, the euro is surpassing yesterday's highs. Maybe it's not the French election and it's just all that lovely economic data. Either way, the euro is not a cooked goose.

And lurking in the background is the on-going problem of the relative real yields. It's all very fine for many in the market to project higher inflation from Trump policies, but the nominal yield has to rise to reflect it. So far, the nominal 5-year is 1.90%, about the same as inflation. Overall, the real yield is zero to negative. You don't get a currency push without more juice than that. We need another 1% or more in the nominal. SocGen's Juckes in the FT says "'A sustained or significant push higher by the dollar from here probably requires US real yields to move towards 1 per cent,' he says. Since 10-year real yields have averaged 1.8 per cent in the past 20 years, and in a climate of continuing gross domestic product growth and rate normalization, ‘real yields ought to be able to get to 1 per cent', he adds." The Fed needs to get busy.

Tidbit: Bloomberg has an op-ed from somebody named Joe. It's a somewhat bizarre take on the FX market and reveals the writer doesn't know FX history or conventional thinking—or maybe that he does. He proposes that the dollar is the sun and everything else is a planet or moon that revolves around it. This was pretty much the idea of Bretton Woods, but Bretton Woods has been dead for a long time. Still, "Joe" makes the point that Trump is already being dismissed as a factor because the role of the dollar is fixed.

"Since Donald Trump became President, there's been a lot of debate about why the apparent chaos in The White House hasn't provoked more (or any) negative response from financial markets. There are all kinds of possible reasons for this. Maybe markets just ignore politics and watch hard data. Maybe the people asking the question are just biased against Trump, and judging markets through a partisan lens -- which tends to be a very bad idea.

"But let's just grant the broader premise, for the moment, that there has been chaos in the White House and that strong U.S. governance has seen better days. So why no market concern? Perhaps the answer is similar to why U.S. interest rates didn't rise during the debt-ceiling debates of 2011 and 2013, even though those debates were precisely about whether the U.S. would pay its debts. The U.S. financial system is, in a sense, the global economy's one constant. You could argue that the dollar doesn't ever actually move... It's other assets that move around the dollar.

"The U.S. dollar is in a sense the financial equivalent of the "inch," an unchanging unit that everything else is measured in. So if you're asking why political dysfunction (today, in 2013, or 2011) hasn't had more market impact, you're essentially asking why the length of an inch isn't changing. In theory it could happen. Official weights and measures can fall out of fashion over the long sweep of history. But it definitely doesn't happen overnight."

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 113.15 | SHORT USD | 02/17/17 | WEAK | 112.86 | -0.26% |

| GBP/USD | 1.2453 | LONG GBP | 01/24/17 | WEAK | 1.2451 | 0.02% |

| EUR/USD | 1.0545 | SHORT EURO | 02/10/17 | WEAK | 1.0587 | 0.92% |

| EUR/JPY | 119.31 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 1.85% |

| EUR/GBP | 0.8467 | SHORT EURO | 02/16/17 | WEAK | 0.8490 | 0.27% |

| USD/CHF | 1.0099 | LONG USD | 02/10/17 | WEAK | 1.0024 | 0.75% |

| USD/CAD | 1.3157 | LONG USD | 02/22/17 | STRONG | 1.3174 | -0.13% |

| NZD/USD | 0.7196 | SHORT NZD | 02/10/17 | STRONG | 0.7185 | -0.15% |

| AUD/USD | 0.7690 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.73% |

| AUD/JPY | 87.02 | LONG AUD | 02/09/17 | WEAK | 85.92 | 1.28% |

| USD/MXN | 19.9495 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 4.14% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat