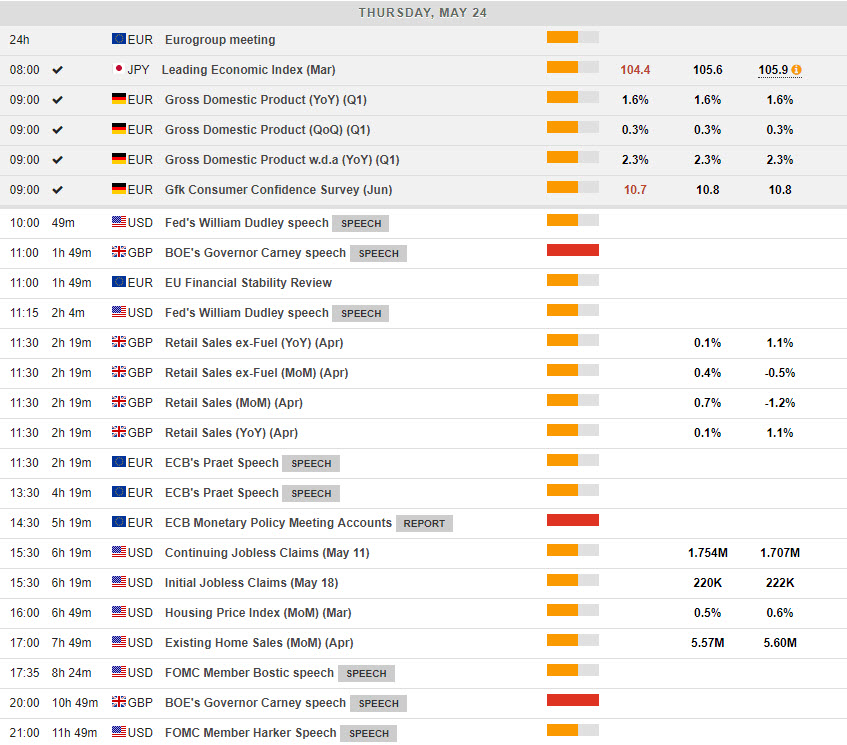

Macro Events & News

FX News Today

European Outlook: 10-year Bund yields quickly recovered opening losses and are now up 0.7 bp at 0.510%, as peripheral bond markets rally led by Italy. The 10-year BTP yield is down -7.9 bp at a still high 2.310%. Spanish and Portuguese 10-year yields are also sharply lower. Reports that Five Star is considering an alternative finance minister to Savona, who promotes Italy’s exit from the euro may be helping. Stock futures meanwhile are mostly heading south in Europe, in tandem with U.S. futures and after a largely negative session in Asia. Released at the start of the session German Q1 GDP was confirmed at 0.3% q/q, and GfK consumer confidence fell back. Still to come the U.K. has retail sales data, ECB’s Praet and BoE’s Carney are scheduled to speak and the ECB publishes the latest Financial Stability Report.

FX Action: Yen out performance has once again been seen, driving USDJPY to a 10-day low of 109.33 and pushing EURJPY further into 10-month low territory. Belligerent rhetoric from North Korea and reports that the Trump administration is mulling a 25% levy on imported cars have provided some added fuel to risk aversion in global markets, which has maintained a safe haven bid for the Japanese currency. The dollar has also remained broadly buoyant, though has steadied off highs seen yesterday versus most currencies. EURUSD posted a fresh five-month low at 1.1675 during the New York PM session yesterday before recouping above 1.1700 following the release of the FOMC minutes to the early May meeting showed the Fed is in no hurry to tighten. Fed funds futures gained a little on the minutes, and were still fully pricing in a 25 bp rate hike in June while showing about odds of about 75% for a further quarter-point hike move in September. Italy will remain in the spotlight and the risk remains that we see further paroxysms in Italian markets as investors digest the formulating policies proposals of the anti-establishment and Eurosceptic coalition government.

German GDP & Consumer Confidence: German Q1 GDP was confirmed at 0.3% q/q as expected, leaving the working day adjusted annual rate at 2.3% y/y. The focus was on the breakdown, which was released for the first time and showed a clearer picture on why growth slowed so dramatically compared to the 0.7% q/q rate in Q4 last year. What the data showed were negative contributions from net exports, stock changes as well as government consumption, with the latter contracting -0.5% q/q in Q1, likely due partly to the political vacuum and the long period without a fully functioning government following the inconclusive election last year. Investment contributed 0.2% points to the quarterly growth rate, private consumption -0.2% points, net exports detracted -0.1% as export growth corrected -1.1% q/q, after rising a very strong 2.6% q/q in Q4 last year. The strong EUR may partly be to blame.

German GfK consumer confidence fell to 10.7 with the advanced reading for June, down from 10.8 in the previous month and the second consecutive dip. The index peaked at 11 in February, but remains at very high levels. Still, the full breakdown for May showed a marked decline in the willingness to buy despite an improvement in income expectations. The willingness to save meanwhile declined. Q1 GDP data today still showed a positive contribution from consumption to overall growth, but the GfK numbers at least signal some slowdown ahead.

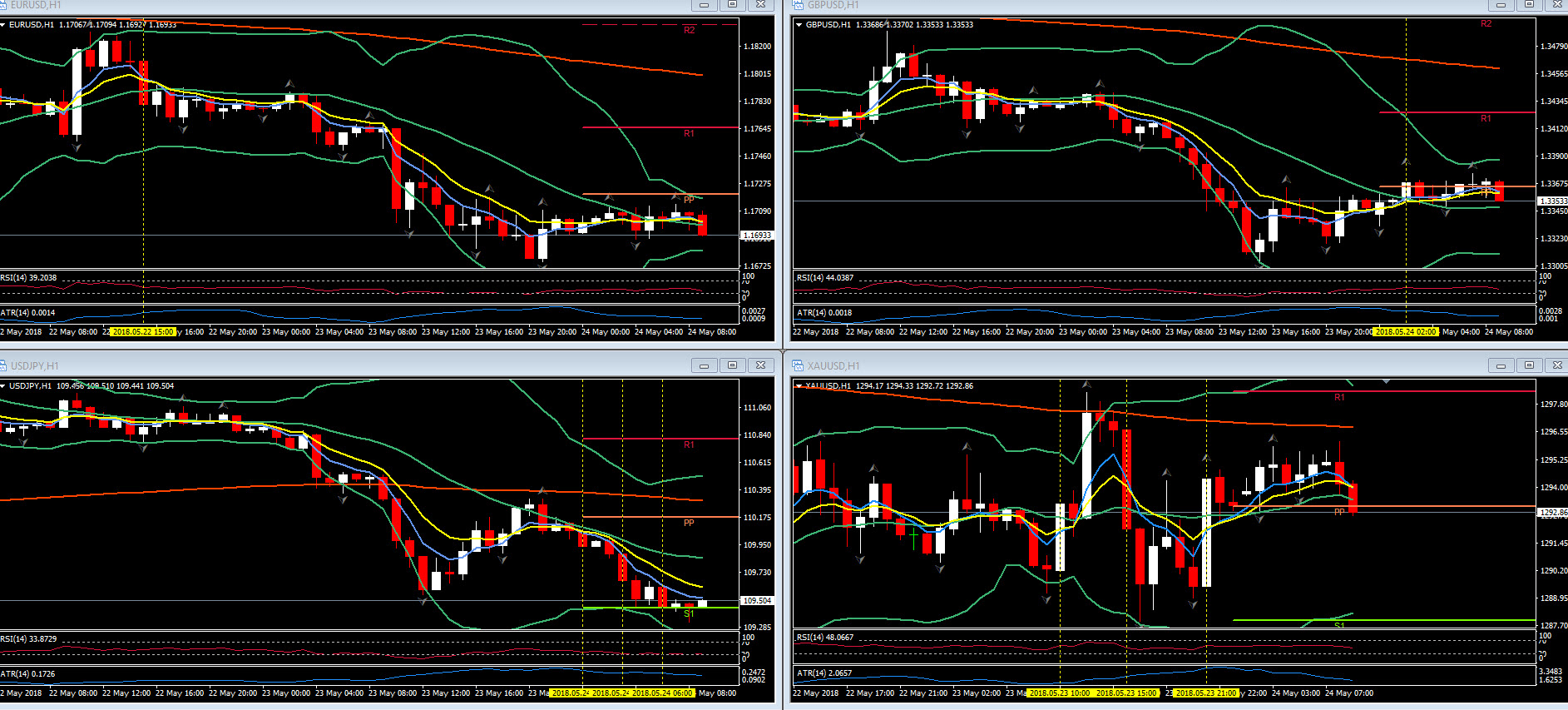

Charts of the Day

Main Macro Events Today

UK Retail Sales – Expectations – Likely to show a pick up (from 0.7% from a dire -1.2% in March) but questions remain this be sustainable through to the summer and remainder of Q2.

US Initial Claims – Expectations – A 2k decline to 220k is expected for new claims with continuing claims rising to 1.754 million.

Plethora of Speeches – Dudley, Carney, Praet, Bostic, & Harker – possibly of some surprises and volatility for USD, EUR and GBP simply from the number of speeches on tap today

Support & Resistance Levels

There's more! Access all our latest analyses and other great content by subscribing to the HotForex Youtube channel. You can also talk to our experts live by registering for one of our free webinars!

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c