Macro Events & News

FX News

European Outlook: Asian stock markets declined amid profit taking. Markets have come quite a way up from recent lows and it seems investors need another catalyst before taking things further. The Nikkei is down -0.25%, the Hang Seng lost -0.62% so far and U.K. and U.S. futures are also in the red ahead of today’s SNB and BoE announcements. Both central banks are widely expected to keep policy on hold, but the BoE’s statement in particular will be watched carefully after this week’s higher than expected inflation number. Gilt yields moved higher yesterday, while the FTSE 100 closed in the red, despite slight gains on other European stock markets. Bund yields also moved up slightly but closed below the 0.4% mark and so far at least it seems the ECB is successful in dampening the impact of its move towards a further reduction in monthly asset purchase volumes, even though yields should have bottomed out. Central bank meetings aside, the European calendar has plenty of ECB speak as well as final inflation data from Italy and France. Released overnight, the U.K. RICS house price balance came in higher than anticipated.

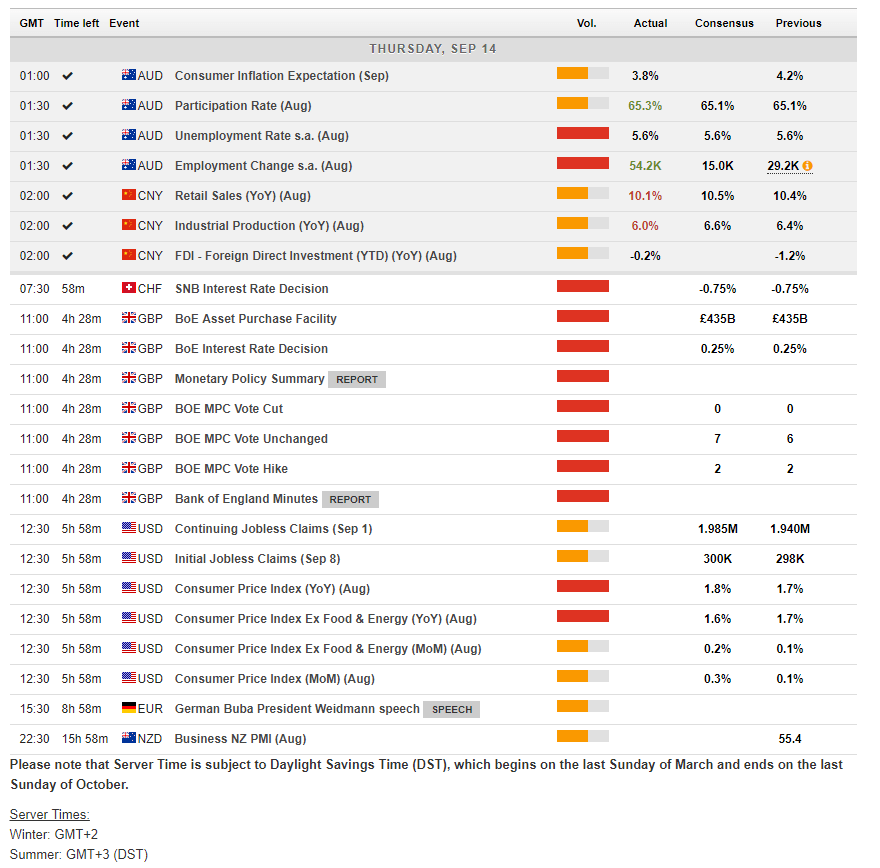

China: China’s retail sales today morning, industrial production and fixed investment were disappointing in August. Retail sales slowed to a 10.1% y/y pace in August from the 10.4% rate of expansion in July. But year to date retail sales growth was 10.4% in August, matching July. Industrial production growth was 6.0% y/y in August versus the 6.4% rate in July. But year to date production dipped to 6.7% from 6.8%. Fixed investment (excluding rural households) slowed to a 7.8% y/y growth pace in August from 8.3% in July. But foreign direct investment did improve to a 9.1% y/y pace in August from 2.3% in July, after contracting 3.7% in May and falling 4.3% in April. The CSI 300 is 0.1% firmer, the Shanghai comp is also 0.1% in the green while the Shenzhen comp is up 0.2%.

Australia: The employment surged 54.2k in August following a revised 29.3k gain in July (was +27.9k). The increase was more than double expectations. The details were strong – full time jobs grew 40.1k after a revised 19.9k drop (was -20.3k) while part time jobs improved 14.1k following a 49.1k rise (was +48.2k). The unemployment rate was 5.6% in August, matching the rate in July. The participation rate rose to 65.3% in August from 65.1%. AUDUSD jumped to 0.8015 from 0.7975 on the report, and has edged slightly lower to 0.8006.

US reports: a 0.2% August U.S. PPI headline with a 0.1% core price increase undershot estimates thanks to a lean 0.1% service price increase, with a flat trade service figure and a 0.3% gain for transportation and warehousing services. We saw the largely expected figure for goods prices, with a 3.3% energy price rise and a 1.3% food price drop that left a 0.5% rise for the goods component overall. It is tentatively expected a hurricane-led 0.5% PPI rise in September with a 0.2% core price increase thanks to a pop in gasoline prices and an assumed rise in service prices. The y/y PPI rise should climb to 2.6%, after rising to 2.4% in August from 1.9% in July, while the y/y core PPI rises to 2.1% from 2.0% in August and 1.8% in July. Oil prices have largely moved sideways in 2017, though we’ve also seen a drop in the dollar and a stronger global economy that has boosted commodity prices, after the opposite 2016 pattern of dollar and oil price gains, but global growth weakness. Upward 2017 price pressure has been limited by the absence of an inventory recovery despite a petro-rebound that is trimming excess capacity.

Main Macro Events Today

SNB announcement– The Swiss central bank will publish the latest quarterly policy review today and is widely expected to keep key policy settings unchanged. Officials have welcomed reduced pressure on the CHF, but still see volatility in forex markets and with the ECB inching only very gradually towards the end of QE and geopolitical risks on the rise again, the SNB is firmly on hold. as it watches developments in the Eurozone and Brexit negotiations.

BOE announcement – September BoE Monetary Policy Committee meeting is due today, in which no change outcome is expected, albeit with the two dissenters from the previous two meetings, Saunders and McCafferty, repeating their votes for a 25 bp hike in the repo rate to reverse the post-Brexit “emergency” cut and return the repo to 0.5%. Not much change is anticipated in the tone of the guidance from that delivered in August, when the central bank was able to expand its view in its quarterly inflation report, which brought downward revisions to growth and inflation forecasts. The market consensus is for the BoE to refrain from change policy settings until 2019.

US CPI & Unemployment Claims – .CPI will be a focal point today, forecast to rebound 0.3% in August from a 0.1% reading in July, while core should remain subdued at 0.1%; on a core y/y basis CPI should remain in the 1.7% area, well shy of the Fed’s 2.0% target. Initial jobless claims may retrace their steps -8k to 290k following the 62k surge to 298k after Harvey, before being distorted again by Irma’s impact, making a wreck of underlying employment trends for some time to come.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in