FX News

European Outlook: Asian equity markets pared some of their recent gains after Chinese export and import data fell short of expectations, and investors ponder the global growth and central bank outlook while taking profits. Mixed earnings reports meanwhile weighed on the TSE and a stronger Yen is adding to pressure. Oil prices are holding above USD 49 per barrel but seem to be trending lower again after briefly rising above USD 50 per barrel at the start of the month. U.S. and U.K. stock futures are also heading south, pointing to a correction in the FTSE 100, which outperformed yesterday, as the DAX underperformed and closed in the red, while other European markets nudged higher. Eurozone spreads also narrowed. Released overnight, U.K. BRC retail sales rose 0.9% y/y on a same store basis, down from 1.2% y/y in May, while Swiss sa unemployment remained steady at 3.2%.

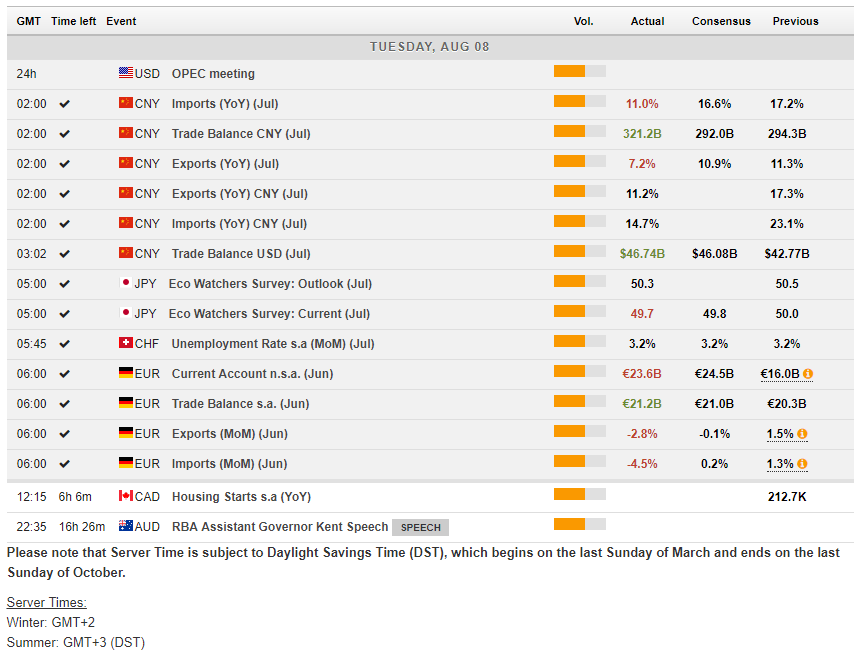

German exports slump in June, but trade surplus improves. In line with the Chinese trade report, German export and import growth disappointed, with exports falling -2.8% m/m and imports -4.5% m/m. The sa trade surplus though improved to EUR 21.2 bln from EUR 20.3 bln, leaving the total for the second quarter at EUR 61.3 bln, up from EUR 59.9 bln in the second quarter of the year. Like yesterday’s production numbers then the data point to a robust Q2 GDP growth rate, with net exports underpinning the German recovery, which orders suggest remains on track in the third quarter, even if automaker’s woes and the strong EUR are seeing investors turning cautious on German stocks.

Fedspeak: Yesterday there was a relatively dovish view from the nonvoting president, Fed’s Bullard, who continues to twist between a hawkish and dovish outlook, largely on the winds of inflation. Fed’s Bullard believes current rates are about appropriate for the near term. But, he’s a bit worried about the still low inflation rate, as recent data have “surprised to the downside and call into question the idea that U.S. inflation is reliably returning toward target.”. Of importance, though is his disagreement with the Phillips Curve orthodoxy that suggests low unemployment contributes to higher inflation, saying there is little relationship. He expects the economy to grow at about a 2% rate, but noted the pick-up in global growth. Those factors, including improved European activity and the potential for a more hawkish ECB, have weighed on the dollar. He supports getting going on QT, meanwhile he concurs with the general FOMC sentiment that the balance sheet unwind will be very slow and there shouldn’t be any big market impact. Fed’s Kashkari gave a speech as well yesterday in South Dakota, where he said he hasn’t seen wages growing very quickly in a Q&A session. The economy is doing pretty well, he added while noting the largest U.S. banks are still too-big-to-fail.

U.S. reported: consumer credit at $12.4 bln in June following the $18.3 bln May increase (revised from $28.4 bln). Non-revolving credit increased $8.3 bln, continuing to lead the strength in consumer borrowing, after the $11.4 bln jump in May (revised from $11.0 bln). Revolving credit was up $4.1 bln versus the prior $6.9 bln gain (revised from $7.4 bln). Credit slowed a bit in Q2, rising $42.9 bln (4.5%), after the $447.1 bln (5.0%) Q1 increase.

Main Macro Events Today

U.S. JOLTS & NFIB – JOLTS and the NFIB small business optimism survey today, will be mulled. The JOLTS expected to stay nearly unchanged with just a small drop to 5.660 M from 5.666M in May. The NFIB Business Optimism Index expected to be unchanged as well at 103.6.

CAD Housing starts – July housing starts are expected to fall to 200.0k from the 213.2k annual pace in June.

RBA Assistant Gov. Kent – RBA Assistant Governor Kent is due to speak today at the Bloomberg Address in Sydney.

Disclaimer: Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of purchase or sale of any financial instrument.

Recommended Content

Editors’ Picks

EUR/USD edges lower toward 1.0700 post-US PCE

EUR/USD stays under modest bearish pressure but manages to hold above 1.0700 in the American session on Friday. The US Dollar (USD) gathers strength against its rivals after the stronger-than-forecast PCE inflation data, not allowing the pair to gain traction.

GBP/USD retreats to 1.2500 on renewed USD strength

GBP/USD lost its traction and turned negative on the day near 1.2500. Following the stronger-than-expected PCE inflation readings from the US, the USD stays resilient and makes it difficult for the pair to gather recovery momentum.

Gold struggles to hold above $2,350 following US inflation

Gold turned south and declined toward $2,340, erasing a large portion of its daily gains, as the USD benefited from PCE inflation data. The benchmark 10-year US yield, however, stays in negative territory and helps XAU/USD limit its losses.

Bitcoin Weekly Forecast: BTC’s next breakout could propel it to $80,000 Premium

Bitcoin’s recent price consolidation could be nearing its end as technical indicators and on-chain metrics suggest a potential upward breakout. However, this move would not be straightforward and could punish impatient investors.

Week ahead – Hawkish risk as Fed and NFP on tap, Eurozone data eyed too

Fed meets on Wednesday as US inflation stays elevated. Will Friday’s jobs report bring relief or more angst for the markets? Eurozone flash GDP and CPI numbers in focus for the Euro.