How high can (and should) the Fed policy rate surge if inflation refuses to buckle?

FED funds rate is obviously the central bank’s main tool to fight inflation, which acts on the price formation mechanism through many direct and indirect stages. First of all, it discourages spending using credit and incites saving instincts of rational individuals. Banks are having a tougher time lending out profitable credits simply because there is less liquidity to toss around and the quality of loan applicants worsen during dramatic rate hike cycles. Reports have come out this week about rising certificate of deposit (CD) rates even among the top-tier US banks since outflows from real person accounts have exceeded quarter of a trillion dollar in 2022, according to Federal Deposit Insurance Corp. data since investors are fleeing to Treasury yields which are much higher than the average CD rate of 1.5%.

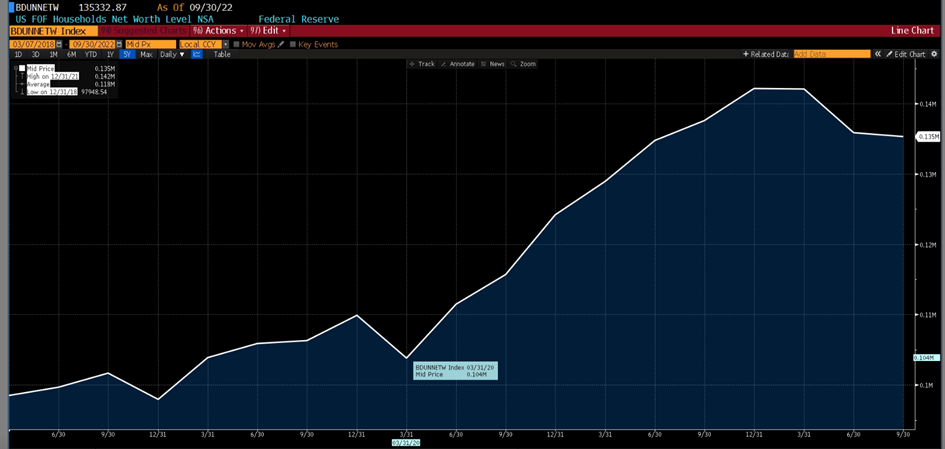

However, besides throwing a monkey wrench into the borrowing-spending cycle, perhaps the most effective and durable blow to inflation using the interest rate weapon is the utter destruction of wealth, at least on paper. The official figures have put the creation of household wealth since the pandemic bottom (end of 1Q2020) to 3Q2022 (the latest official announcement) at almost 30 trillion USD. This inertia of this data is very huge and noise is very small so we can safely predict that fortunes must have climbed up within the past 5 months.

This week for two days and a total of almost 5.5 combined hours, FED Chair (Honorable) J. Powell has sat in front of Congress members and replied question after question. Although the economy is seriously reeling from inflationary pains, the Congressmen & women surprisingly grilled the FOMC’s leader more about the burden of high interest rates. He was specifically called-on about his intent to rest his case for accelerating rate hikes (the euphemism for making a 50-bips hike instead of the usual 25-bips) on whether more than expected people found jobs and whether those already employed had wage gains exceeding inflation. Both sides of the aisle (Republicans and Democrats) were critical about dismantling inflationary forces by handicapping the purchasing power of US consumers.

The testimony sessions clearly revealed that the pressure on FED about fighting inflation is coming in unison with the constraint about keeping the economic growth on an even keel, hence there is certainly no green light about growth and monthly payroll numbers going into the red territory. The JOLTS figures were also a huge blow to FED’s envisaged (albeit bizarre) path to a goldilocks market outcome where prices become steadier while keeping workers at handsomely paying jobs; namely, a tight monetary stance and rising interest rates would dissuade businesses from looking for workers and the job market would find a balance where unemployed masses would have to accept bargain salaries in order to get hired. Despite the headline job opening figures displayed a decrease from the prior month, it was almost 300K more than the expected drop. Since job openings are plenty and job seekers are scarce, coupled with quit rates remaining high, the only way to get inflation declines seems like crippling paycheck numbers as well as the average amount of each check.

The market-based interest burden has already become onerous, since bond yields are pushed up by near, medium- and long-term inflation expectations. Treasury markets are pricing 1-year and 2-year inflation rates (the level of the 12-month backward looking CPI from 1 or 2 years from now) already surpassed the highs of last July when inflation when FED was concatenating 75-basis point hikes. The first one has exceeded 3.40% and the second one is around 3.15%. Both figures were at or below 2.0% threshold at the New Year’s Eve. Hence we observe that the cost of credit has skyrocketed on all maturities, and the prospect of recession is not enough yet to limit long-term rates which otherwise could spare the housing market from this macroeconomic wildfire.

Unlike 2010s, this decade seems doomed to an elevated structural (and hence sustainable) rate of inflation since many factors outside of the FED’s (and other central banks’) intervention such as transition to clean energy, tighter labor markets which results from the firms labor-hoarding as well people quitting from the workforce at earlier ages, rising geopolitical tensions due to the higher number of military superpowers with conflicting interests, and disrupted supply chains inherited from the pandemic era all lead to a higher (and inevitable) rate of inflation.

The last few weeks’ trading has shown that markets reach to real rates as much as the nominal figures. In the real 2-year rates chart (thanks to Bloomberg) shown below, even small intersession drops supported the risk markets to find bids in March even though nominal 10-year yields hovered around the dreaded 4%threshold. Whatever hike the FED opts for this month, it should not let this chart to blow past the 2.00% mark significantly, which is already the highest figure since the Great Recession. Even one-and-a-half decades ago, the real rates were up so much only because inflation expectations turned seriously negative (even more than negative 5% for a few weeks), hence there is virtually no historical comparison since the Volcker’s FED era.

There is virtually no limit to how high the policy rate can go if the FED stubbornly refuses that a higher long-run inflation regime is the name of the game. All the Ponzi-like monetary schemes set during the Great Recession and the COVID19 pandemic to save the world economy has come home to roost, hence we need to make payments for those past deferred debts (since a lot of global public and private debts for practically “forgiven” by central banks in those epochs). A higher long-run inflation will be the price that has to paid. Successfully pulling off the dual mandate of keeping inflation rate at slightly above 2% and maximum (non-inflationary) employment has already become a joke in the near and medium term.

Nevertheless, we believe that the FED will opt for a moderately high policy and instead persist on that rate for a longer period. There have been 3 huge policy errors during this rate hiking cycle (starting too late, and then too slow, and then decelerating too early), the FED has no room for a 4th mishap. The world economy and the risk markets cannot endure another easing and then reversing course to another tightening cycle. Thereby, barring any huge surprise numbers in wage growth and core inflation figures in the next few months, the FED policy rate should peak at 5.50%. That rate may either come in the form of three 25-bips hikes or a 50-bips hike this month and a 25-bips in May. Going above this rate maybe the straw that breaks the camel’s back and create a huge market stir, since going to 5.75% at some point would entail the market to fully price in 6.00%. We expect volatility and downward pressures to abate after the new terminal rate is negotiated between the markets and the FED, hopefully after the FOMC meeting at 22nd of March.

This article is sponsored content

Author

Emre Ozturk

Numberone Capital Markets Limited

Emre Ozturk is a dedicated, analytical and methodical finance professional who graduated in Business Administration from the Bogazici University.