Hawkish hike: We now expect additional Jun and Dec hikes

As widely expected, Norges Bank (NB) this morning raised the policy rate by 25bp from 0.75% to 1.00%. The rate path was adjusted upwards, as domestic factors, including the oil price and NOK, more than countered the negative effects of global growth and rates.

As Norges Bank clearly supports our view on the relative performance of the economy, we now expect NB to hike rates again in June, and deliver yet another rate hike in December (previous call was one 2019 hike in September).

The Executive Board stated that: ‘Our current assessment of the outlook and balance of risks suggests that the policy rate will most likely be increased further in the course of the next half-year.'

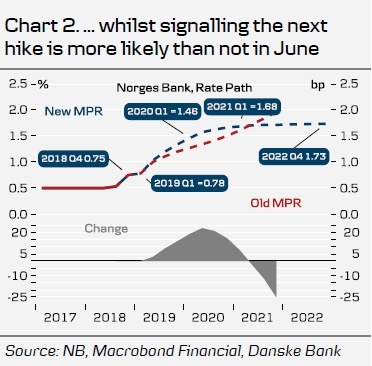

The rate path published in the Monetary Policy Report (MPR) was adjusted upwards until early 2021, and then downwards (Chart 2). Specifically, the rate path indicates that the next hike could come as early as June, and that a third rate hike in 2019 has a more than a 50% probability. Further out the rate path signals slightly more than one hike in 2021 and flattens around 1.75%.

The factors affecting the rate path were broadly in line with our expectations. Global risks and global forward rates pushed the rate path downwards. Surprisingly, a weaker currency, a moderately higher oil price and stronger domestic growth more than counteracted these effects.

However, the main takeaway from this meeting is that the robustness of the economy speaks for a gradual normalisation of rates despite the global weakness.

We now expect NB to hike rates again in June, and deliver another rate hike in December, taking the policy rates to 1.50 % at the end of 2019.

FI/Rates. We have earlier argued for a flattening of the Norwegian yield curve. Norges Bank flattened the interest rate projection more than we expected by adjusting the very short end of the 3m fwd Nibor curve by as much as 22bp mid-2020. There is a real probability of a third hike during 2019. The end-point of the projections was adjusted significantly downwards. We reiterate our strategies for a steeper Norwegian curve relative to international peers – as discussed in the recent Reading the Markets Norway. In particular the case for the Norwegian curve moving in the direction of the US curve seems to have become strengthened by the recent meetings in the FED and Norges Bank.

FX. At the time of writing EUR/NOK has fallen around 9 figures testing the 9.60 support level. We expect an eventual breach of 9.60 but in the near-term the 1.0850 level in NOK/SEK remains key. Fundamentally, we have over the past few months argued that relative growth, relative rates, tighter structural liquidity and a China-led stabilisation in the global environment alongside a higher oil price would support a stronger NOK. We think the carry-momentum argument has been significantly strengthened today, with June becoming a live meeting. Also Norges Bank itself now expects a much sharper appreciation tempo of the NOK than previously, meaning a stronger NOK in the magnitude of 3-4% this year will have little impact on the rate path. We remain short EUR/NOK via a 2M risk reversal (live PnL:+0.6%) and long NOK/SEK spot (+3.0%).

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.