Gold to perform admirably in 2019

Being long gold has been a tough investment since 2012, and so often, when we see the yellow metal gaining traction the USD regains its mojo, and we see the inevitable reversal. However, as we look into our crystal ball and gaze into 2019, emerging warning signs can be seen that suggests 2019 could be the year where the gold bulls finally get their day in the sun.

The case for gold

Forget inflation as our guide, gold rallies in 2019 as the ‘anti-USD and best of the rest’ trade. That being, it will be the best house in a bad neighbourhood, and progressively seen as an alternative to G10 currencies. Falling ‘real’ (inflation-adjusted) and nominal long-end bonds yields, amid elevated and sustained implied equity and bond volatility will only promote gold to the investment community.

A capital preservation trade should grip the world, and we see a hunt for duration in US and German bond markets, while the JPY and precious metals all trend higher. The prospect that the equity and credit market search out the strike price for the ‘Fed put’, where driven by risk aversion and a sharp tightening of financial conditions, the Federal Reserve (Fed) alter its communication to indicate the US rate hike cycle is over.

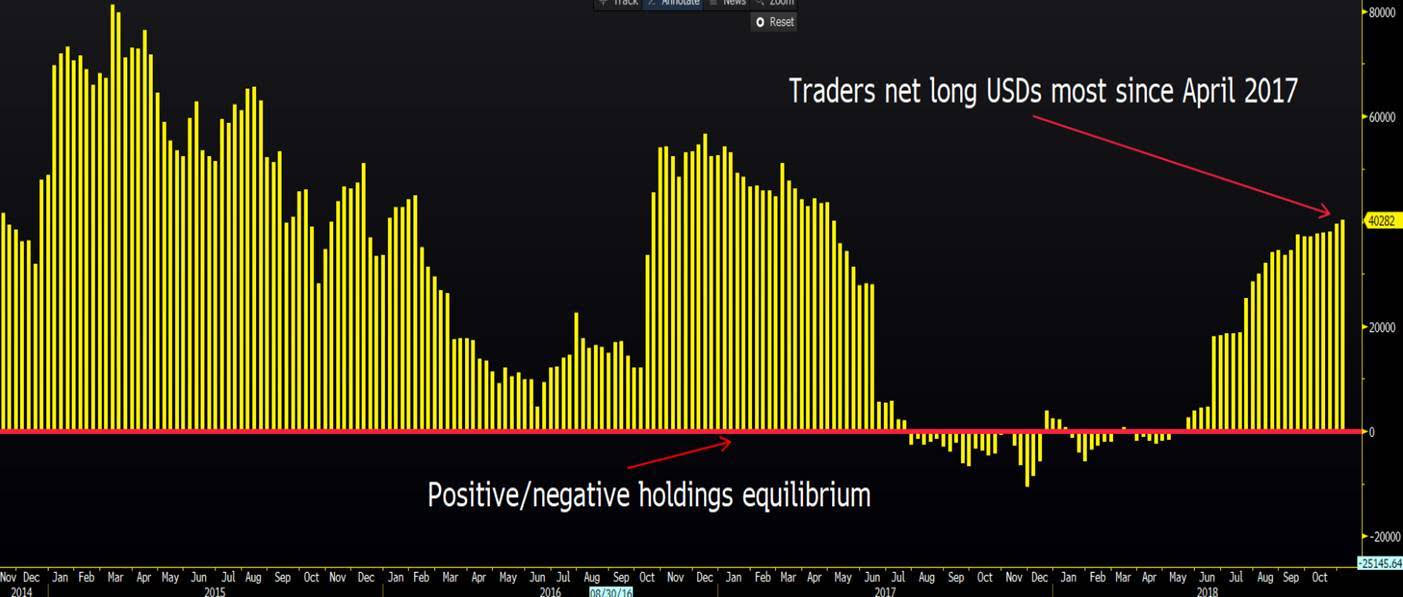

Currency wars, a theme that gripped financial markets at various time since 2010 could become a significant theme again, and this, in turn, should promote gold as the best alternative. That time is currently not upon us, as the USD index is trending and at the highest level since June 2017, with speculative positioning ever increasing (see Bloomberg chart below). However, it’s what happens when the USD losses its appeal that interests most and it's this consideration that I want to explore.

(Histogram of the weekly CFTC data showing non-commercial gold futures holdings)

(Source: Bloomberg)

A taste of things to come

The market has shown us through October, perhaps on a small scale, how 2019 may evolve, although the foundations for the volatility were really put in place from mid-August. Theoretically, we shouldn’t see the US 10-year ‘real’ Treasury trade to the highest level since 2011, libor rates to the highest level since 2008, while US crude and Chinese and HK equity markets fall into a bear market, yet the S&P 500 makes a new all-time high. That dynamic makes very little sense, as the cost of money is rising, at a time when liquidity, the oxygen of markets, is falling.

(Inverse relationship - White line - US 10 year ‘real’ Treasury, Orange line – gold)

The tipping point came in October when we saw S&P 500 implied volatility (VIX) pushing to 28% and risk assets globally savaged. At the heart of this was a clear central catalyst; The Federal Reserve had altered its communication on hiking interest rates and the idea that they were prepared to take the fed funds rate past the short-term neutral rate, which many felt was closer to 3%, meant markets had to readjust radically.

US economic dynamics

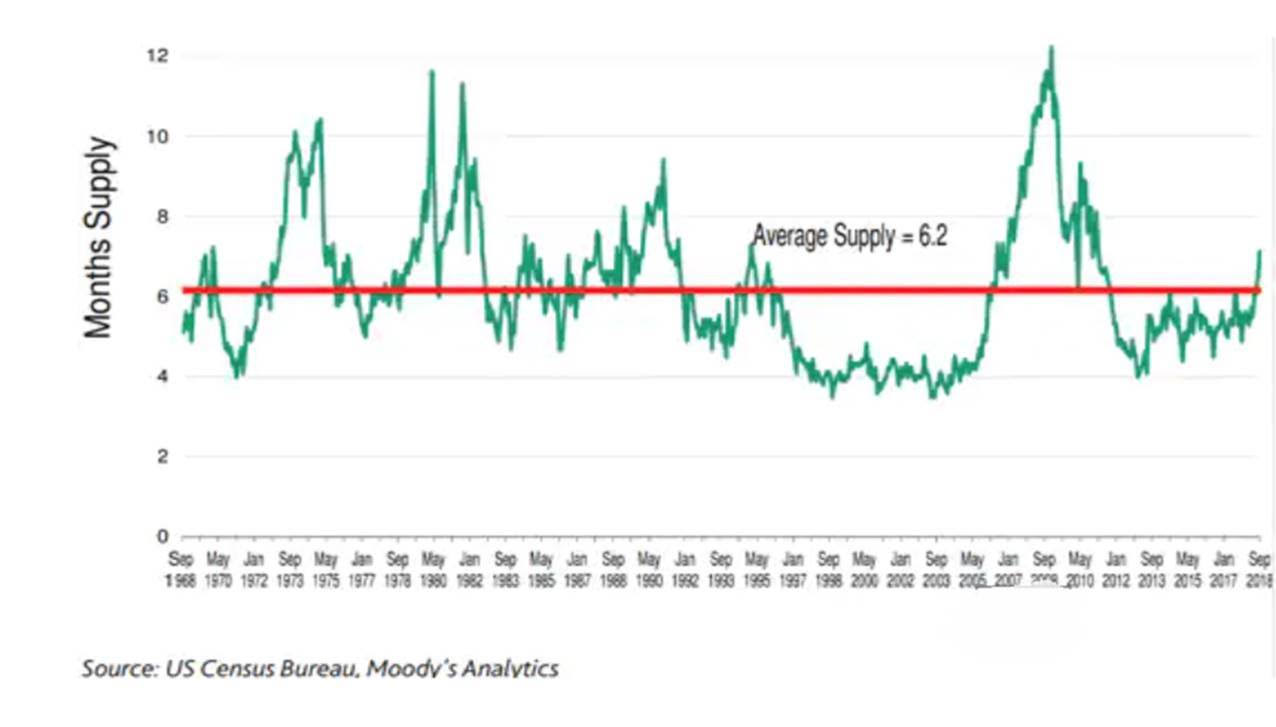

The bears will immediately point to the interest-sensitive parts of the US economy, with softness seen in auto sales, residential investment and housing starts, while the inventory of new unsold homes has pushed sharply above the long-term average (see chart below). We can focus on the fact 30-year mortgage rates have risen to the highest levels since 2011 and pushed fears of housing affordability.

We can look at capital goods orders (ex-defence) and see this falling from 10% yoy growth in July to a 1.1% yoy pace at the last read. There is no doubt weakness in these data points contributed to the drawdown in risk assets, but the failure from the Fed to acknowledge this weakness is the bigger issue.

Cooling the US labour market

Of course, the Fed is fully aware of the deterioration in certain aspects of the economy, but they would be far more focused on the fact the employment rate is sitting at 3.7%, and some 80 basis points (bp) below what is considered ‘full employment’ and on the Fed’s economic projections we should see the unemployment rate even tick down to 3.5% in 2019.

For those familiar with economic theory would know an unemployment rate this far through full-employment and NAIRU (the non-accelerating inflation rate of unemployment) would worry any central bank. Especially the Fed who sense these dynamics will hold huge implications for the availability of labour and a steeper Philips Curve, which subsequently results in wage pressure and inflation. This comes at a time when they are already meeting its inflation target (core Personal Consumption Expenditures or PCE is running at 2%), while wage growth is running at 3.1% - the hottest pace since 2009.

Now look at look at the fact while the US economy has come off the Q2 high of 4.2% GDP growth, it is growing 70bp above-trend growth of 2.8%, while the services ISM print is not far off the highest levels in 21 years. The Fed would argue that they are facing a rising output gap and that even now the US economy is overheating. So, to derail the Fed from its chosen path of higher rates and a reduced balance sheet seems a tall order, and, as stipulated even through this recent volatility the Fed were unnerved and committed to the cause.

A policy mistake

There has been much made of the Fed economic projections, but the fact they have 4.5% as its longer-term forecast for unemployment is incredibly important. Perversely, this forecast suggests unemployment will not only rise, potentially as a result of a decline in investment, but the Fed could actually engineer this, as it would be a critical factor in closing the output gap and cooling the linkage with inflation.

So where do you go?

At a time when other parts of the economy are already sagging, and China and Europe have shown economic vulnerabilities all through 2018, then a rise in the US unemployment rate will be the straw that breaks the camel’s back. Naturally the Fed will communicate this to the market, but if there is an unexpected tick higher (in the unemployment rate) say in early Q2, traders will sense a policy mistake, and risk aversion will take hold, with a rampant flattening of the US yield curve and a USD flight will be in play.

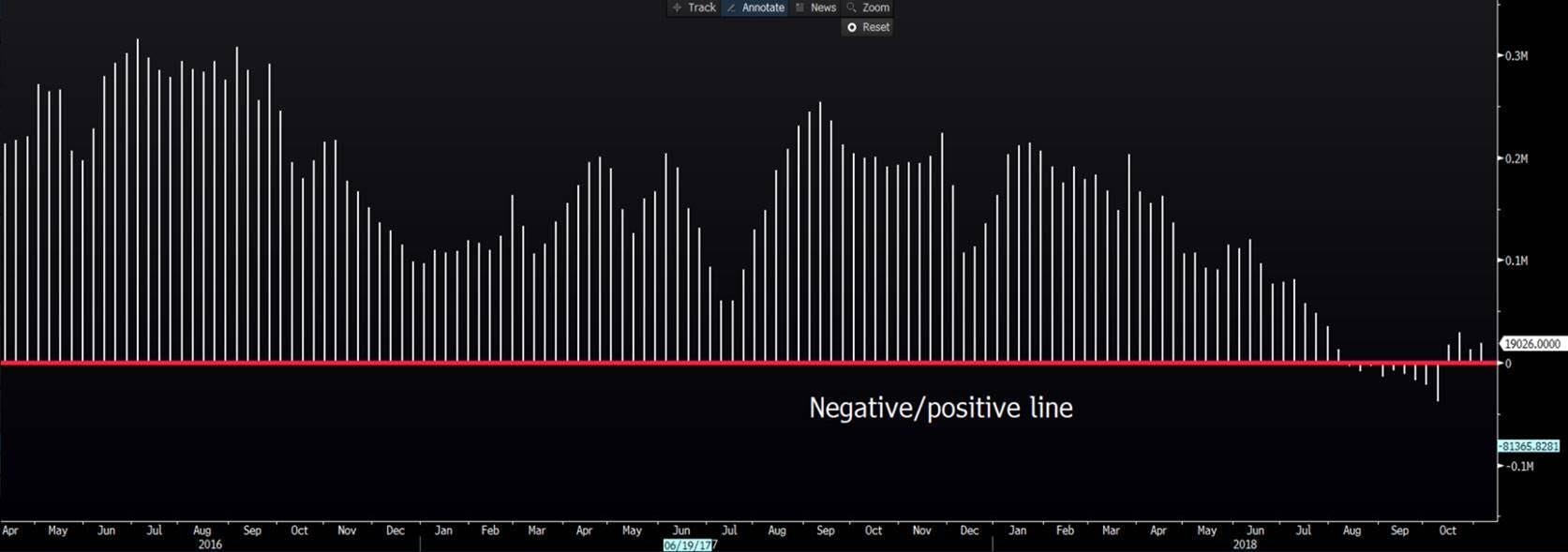

This is when gold works, especially when the position in gold futures (see below chart) has been significantly reduced.

(Weekly CFTC data showing the net long or short position on gold futures)

The US bond market already has to contend with the dynamic of sourcing capital to fund an ever-growing fiscal deficit, with estimates of 4.8% of GDP in 2019. The role of the primary dealer, those US financial institutions mandated to buy bonds at auctions, will be even more important and will offer great insight into external demand for US debt. In an environment of heightened volatility, countries with high external funding needs will struggle and the US is the posterchild of deficits in developed markets.

As mentioned, Europe has been slowing for much of 2018, and this will only get worse in 2019. The ECB will completely stop asset purchases in December, but from here the discussion turns from one of whether it is realistic that they will hike in late 2019. Instead we are already asking whether they will offer another round of ultra-cheap loans to European banks (LTRO), and this looks likely, especially with some €500b in maturing TLTROs (Targeted Longer-Term Refinancing Operations) by 2020. Italy is not out of the woods, and many feel its fiscal budget for 2019 will come out closer to 2.9%, rather than 2.4%. Italy has to raise €50b in funding from the markets in 2019, and they will no longer have the luxury of the ECB buying its bonds in the secondary market and keeping its funding costs in check. The domestic banks will be asked to buy Italian debt, and that is a huge worry.

Germany, the powerhouse of Europe, has had a well-documented slowdown in manufacturing, with foreign orders collapsing, resulting in a rampant build in inventories. A technical recession seems touch and go, just as it will be in Italy. So, if long-end US Treasuries are headed lower, then 10-year German bunds will move closer to 10bp, perhaps even zero. There seems little reason to believe the ECB will hike anytime soon, if at all, so without the EUR offering a real investment case then we look further elsewhere and again we turn to gold.

It’s hard to see huge upside in AUD or CAD unless we start talking renewed QE. The GBP could be a good alternative, but its line ball, whether the UK economy will be pummeled by a so-called ‘hard Brexit’, and this outcome is progressively looking more likely. Anyhow, even if we do see a positive outcome, it may be so long time before we fully understand the full extent of the impact that institutions won’t touch the GBP with any great conviction and 1% GDP is the new normal in the UK, even if there are elevated wage pressures.

Could the world pile into the CNY? Again, this seems unlikely. So that leads us to the JPY and CHF. The Swiss National Bank (SNB) don’t have much it can do with rates, especially given the SNB are already at -75bp and bear in mind it has accumulated a sizeable position in US tech stocks through its asset purchase program, and this is a headwind for the CHF. CHFJPY shorts look like an excellent trade for 2019, as the JPY should perform well if financial market volatility.

The trigger level to buy

Clearly, we are not at the point of accumulating gold assets with any conviction. In fact, we may not get there, but my view is that a Fed hiking to close the output gap at a time when we see vulnerabilities both internally and externally. And at a time when liquidity is falling, and USD fundin is high, suggests once the USD falls out of favour and there are no clear alternatives then gold will rally hard. The US unemployment rate is our trigger.

The weekly chart gives great perspective and there is little reason to buy now. That said, I am a buyer through $1238, but the real kicker comes if and when the unemployment rate starts to react to tighter monetary conditions, and that may be some months off yet. But it the battle lines are set.

(Source: Bloomberg)

Author

Chris Weston

Pepperstone

Chris Weston recently joined Pepperstone as Head of Research.