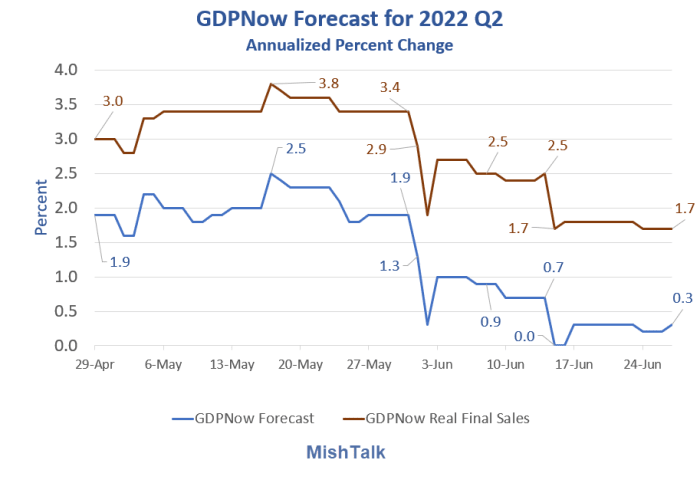

GDPNow forecast inches up to 0.3 percent, but what's on the way?

The GDPNow was mostly flat, but bigger economic reports are one the way. Let's look ahead at upcoming data.

GDPNow data from Atlanta Fed, chart by Mish

The Atlanta Fed GDPNow Model was on updated June 27. The previous release was June 16. The intermediate points and movements in the chart above were just updated today.

Key points

- Real Final Sales (RFS) is the true bottom line forecast of the economy.

- The difference between GDP and RFS is inventory adjustment that nets to zero over time.

- RFS is 1.7 percent, unchanged since June 26.

- Base GDP is up to 0.3 percent from June 26, a meaningless rise in size but more importantly because RFS is the number to watch.

Housing

- Since June 16 the most important data releases were existing and new home sales.

- June 24: New Home Sales Jump 10.7 Percent in Big Upward Surprise

- June 21: Existing Home Sales Skid Another 3.4 Percent in May, Down Fourth Month

The net impact of housing was essentially nothing.

Important notes about the model

This might sound odd, but it's very important to note that the data itself does not necessarily matter.

What does matter is what the data does vs what the model predicted.

Thus, seemingly good surprises to the upside might cause the forecast to decline and seemingly bad surprises might cause the forecast to rise.

All that matters is how good or bad the data is relative to the forecast. Every data point changes the model's expectation of what's coming.

Looking ahead

The next GDPNow forecast is Thursday, June 30. Looking ahead the data points are

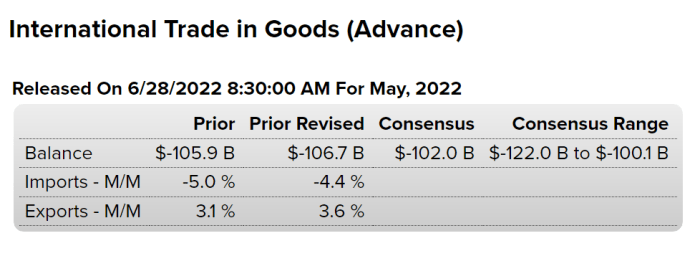

- International Trade in Goods: June 28

-

Q1 GDP Final: June 29

-

Jobless Claims: June 30

-

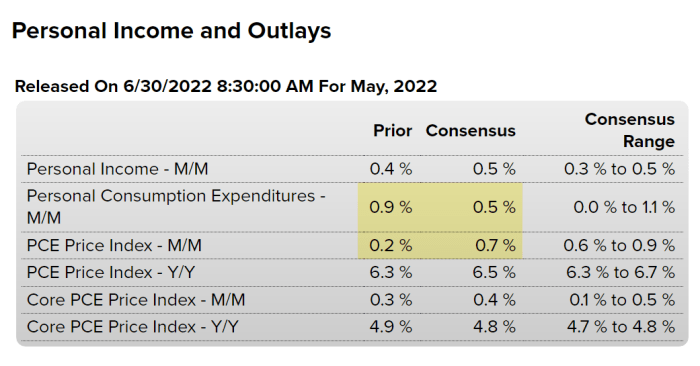

Personal Incomes and Outlays: June 30

-

ISM Manufacturing: July 1

-

Construction Spending: July 1

In terms of swings to the GDPNow forecast, the most meaningful reports are the three in italics above. But ISM is outside the date range of the next forecast.

International trade in goods for May 2022

Bloomberg Econoday Consensus Estimate

Imports down and exports up seems like a good result, but on June 7 International Trade knocked down the GDPNow forecast because the model predicted more.

I suspect the model will have this correct unless there are some big revisions.

Personal income and outlays estimate for May 2022

Bloomberg Econoday Consensus Estimate

There is plenty of scope for big surprises in personal incomes and outlays, both to the economists and to the GDPNow model.

May retail sales numbers and April revisions took the GDPNow estimate down from

On June 15, I noted Retail Sales Flounder in May With Negative Revisions in April.

- The March 2022 to April 2022 percent change was revised from up 0.9 percent to up 0.7 percent.

- In nominal terms retail sales fell 0.3 percent.

- In real terms sales fell from 233,724 to 230,852 from April to May.

- That's a month-over-month decline of 1.2 percent, using the CPI as a deflator. It's real, not nominal spending that's an input to GDP.

What's the model thinking?

I asked Pat Higgins, the Atlanta Fed creator of GDPNow that question on June 3 regarding ISM.

I asked because the model took a big hit on June 1 when the forecast of RFS declined from 3.4 percent to 2.9 percent on what seemed to be an ISM surprise to the upside.

Hi Mike,

There is not really an easy way to translate what the model was expecting for the ISM Manufacturing data with the actual release [in addition to the composite index, the model also includes the employment, inventories, new orders, production, and supplier deliveries subindexes]. But I have attached the estimates of the factor on May 27th (pre ISM) and on June 1st (post ISM). On May 27th, the May and June 2022 values are forecasted based on the factor estimates through April. On June 1st, the model uses the ISM Manufacturing data [and all of the lagged data] to estimate the factor for May and then uses the factor estimates through May to forecast the June factor value. Here's an email on Real Final Sales

Best regards,

Pat

Guessing game

- So not only are we guessing the data, we are guessing what the model is predicting in relation to the data.

- Based on May retail sales, I suspect the model envisions a downward revision to April.

- There easily could be another adjustment lower to April and a miss for May.

- There could easily be something else.

My guess is the data will be weaker than what economists project. But that might not matter if it's not what the model thinks.

To go out on a limb, I think May will be worse than the model projects and June much worse than the model predicts at this time.

If incoming data changes to the downside, then the model will reflect that data in later updates.

US manufacturing output contracts for first time since 2020, service growth dramatically slows

The next GDPNow release on Friday will not incorporate ISM. And the model does not look at manufacturing PMI at all.

The PMI took a big smack on June 23 as noted by my post US Manufacturing Output Contracts For First time Since 2020, Service Growth Dramatically Slows

Since that is not reflected in the model, there's a good chance of a sizable model miss on ISM. However, ISM tends to be way higher than the PMI.

Place your bets.

I suspect the model estimates too much from consumer spending and way too much out of the ISM.

If so, the GDPNow Real Final Sales forecast will plunge.

Yet, that still is not conclusive. The GDPNow model itself may be inaccurate. The final forecast of GDPNow has been quiet good for many quarters, but that does not imply the next one will be as good.

The model can miss to the upside or downside.

Models cannot think

Models cannot think. We can. The data looks bad and feels bad. More importantly, the direction is bad.

Strong April retail sales took a dive in May, housing is pretty much going to hell, the Fed is tightening at a record pace on a percentage basis, QT just started, and the wealth impact from the stock market and crypto collapse is huge.

Add it all up and you get a recession that started in May.

I've seen enough, the US is in recession now, Q&A on why

For more discussion of the above data points, with many charts, please see I've Seen Enough, the US is in Recession Now, Q&A on Why.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc