GBP/USD sends bearish vibes below 20-SMA [Video]

![GBP/USD sends bearish vibes below 20-SMA [Video]](https://editorial.fxstreet.com/images/Markets/Currencies/Majors/GBPUSD/british-banknotes-14144912_XtraLarge.jpg)

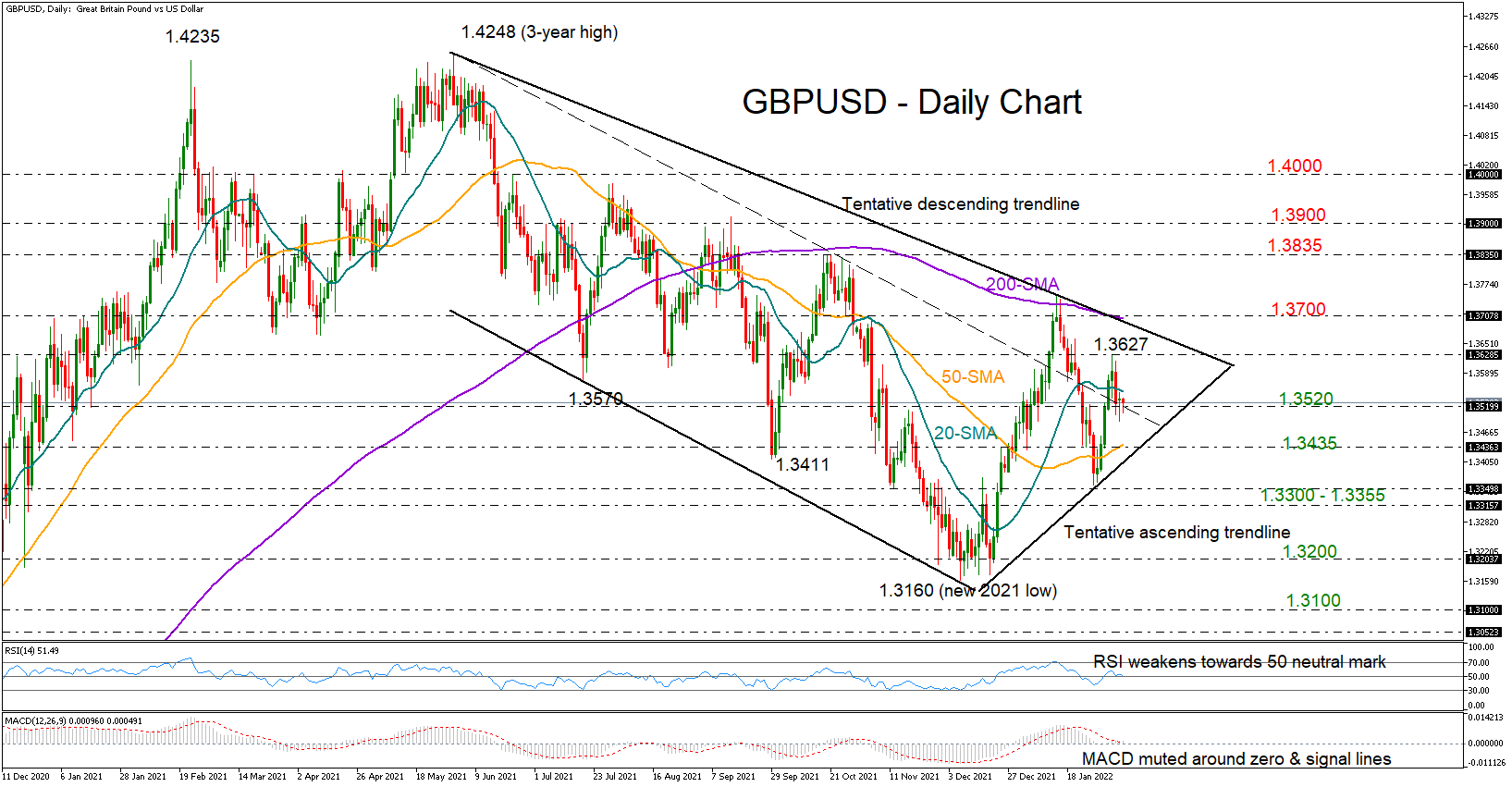

GBPUSD saw its bullish efforts evaporate near its 20-day simple moving average (SMA) on Monday, with the pair finishing the day muted and beneath last week’s peak of 1.3627 once again.

GBPUSD saw its bullish efforts evaporate near its 20-day simple moving average (SMA) on Monday, with the pair finishing the day muted and beneath last week’s peak of 1.3627 once again.

The above suggests the bears are still in charge and a downside correction below the nearby support of 1.3520 and towards the tentative ascending trendline and the 50-day SMA both at 1.3436 is still very likely. The negative slope in the RSI and the MACD, which are currently near their neutral levels, is also reflecting a weakening bias.

Should the upward-sloping trendline give way, the support region of 1.3300 – 1.3355 could immediately attempt to defend the short-term upleg off 1.3160. Failure to bounce here could trigger a sharper decline towards the 1.3200 number, while a close below the 2021 trough of 1.3160 may log a new lower low around the 1.3100 psychological mark.

In the event the bulls retake control above the 20-day SMA currently at 1.3549, driving the price above the latest peak of 1.3627 as well, a tougher battle could commence around the tentative resistance trendline and the 200-day SMA at 1.3700. A successful violation at this point would ruin the bearish trajectory in the medium-term picture, bolstering buying orders likely straight up to the 1.3835 and 1.3900 constraints.

In brief, GBPUSD is looking to be at a disadvantageous position in the short-term picture despite last week’s rebound, remaining exposed to additional declines towards 1.3435.

Author

Christina joined the XM investment research department in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.