FOMC looms

The Fed concludes its 2-day meeting today and releases its policy statement and new Summary of Economic Projections (SEP) at 18:00 GMT. The market will focus closely on the statement and ensuing press conference for further insights on the inflation targeting framework and discussion of other possible policy actions.

Chair Powell will hold his press conference from 18:30 GMT. He largely preempted this meeting in terms of policy with his Jackson Hole announcement of the FOMC’s new strategies where it will pursue an average inflation target and monitor any shortfall in employment. The Fed had already indicated, and reiterated it’s interest rate posture would be on hold for years into the future, but it’s now codified.

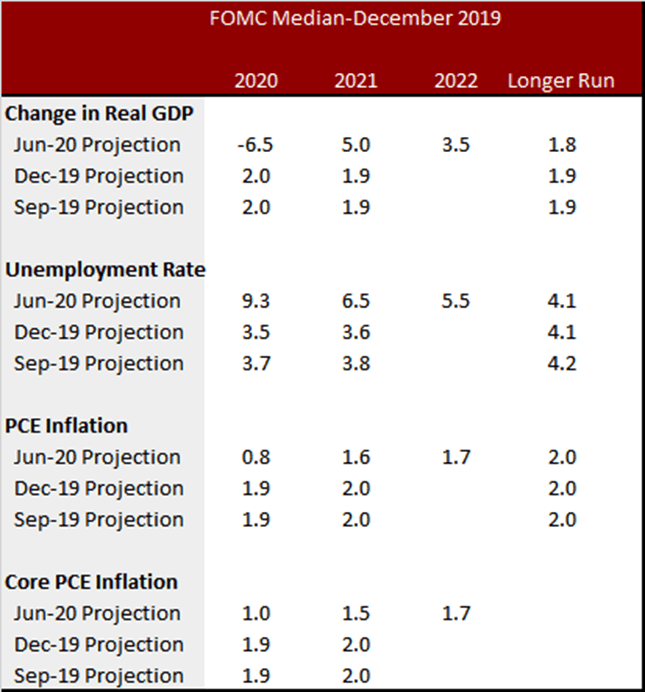

Hence, attention will be on the Fed’s revised forecasts, which will likely show out-sized boosts in the official 2020 GDP forecasts, followed by a smaller 2021-23 bounce. The statement is expected to show upward revisions to GDP and inflation outlooks, and a downward bump to unemployment. The GDP is seen at a central tendency boost to the -3.6% to -3.2% area, from the prior central tendency of -7.6% to -5.5%.

The dot plot should show no rate hikes through 2023. No changes are anticipated to forward guidance currently, or to QE, as the Fed takes a more wait and see approach for now. Indeed, a number of Fedspeakers have suggested action on forward guidance would be “premature.”

In the following, we summarize economic developments that have occurred since the last FOMC meeting in July regarding the labor market, inflation and consumption.

Consumption: Real PCE has been hit hard by the shutdowns, leaving a Q2 contraction rate of -34.1% after a -6.9% pace in Q1. GDP fell at a -31.7% rate in Q2, after a -5.0% Q1 pace. Monthly consumption fell -12.9% in April before rebounding 8.6% in May and 1.9% in July.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in