Fear could linger after toasted trade deal

Summary

The market's verdict on the trade deal will take more than Beijing and Washington platitudes to shift.

Extended ‘over-reaction'

On the face of it, the 550-point collapse in Dow futures that immediately followed news that a senior Huawei executive was arrested looks like an over-reaction. If so, it has with legs. The second half of the European session sees indices barely off Thursday's worst, keeping the STOXX gauge close to a fresh two-year low, its second since late October. The Dow gushes another 400 points lower.

Close relation

The velocity of these declines looks past ostensible disconnects between Huawei and the trade dispute. True, the company is publicly owned, and the case involves alleged sanction violations. But Huawei's state links are hardly no secret. Decades-long affiliations have smoothed the regulatory permissions it required to become the world's second-largest smartphone maker in just over 30 years. The arrest of Huawei's chief financial officer, the daughter of founder, Ren Zhengfei, a former People's Liberation Army officer, won't pass as ‘unrelated.'

November gains almost wiped

Price action over the last 12 hours, which erases almost all late-November gains on Wall Street, Shanghai/Shenzhen and in Europe is the market's verdict. Furthermore, Huawei recently lost authorisations in the UK, New, Zealand, Australia and the States. Its participation in major new international transactions could also be definitively over. Anticipation of a messy extraction from contracts, partnerships, supply chains and more, keeps technology sector upset on par with tumbles in trade-sensitive car, and metal shares. Elsewhere, OPEC and Russia appear to hint at a smaller cut than the market would like, dragging energy sectors. That's all broad equity segments under a cloud. Already upended by Treasury yields' acceleration to three-month lows, volatility in major currency pairs remains unsettled too. Volatility goes up a notch as safety bids reappear in dollar, the yen and bunds.

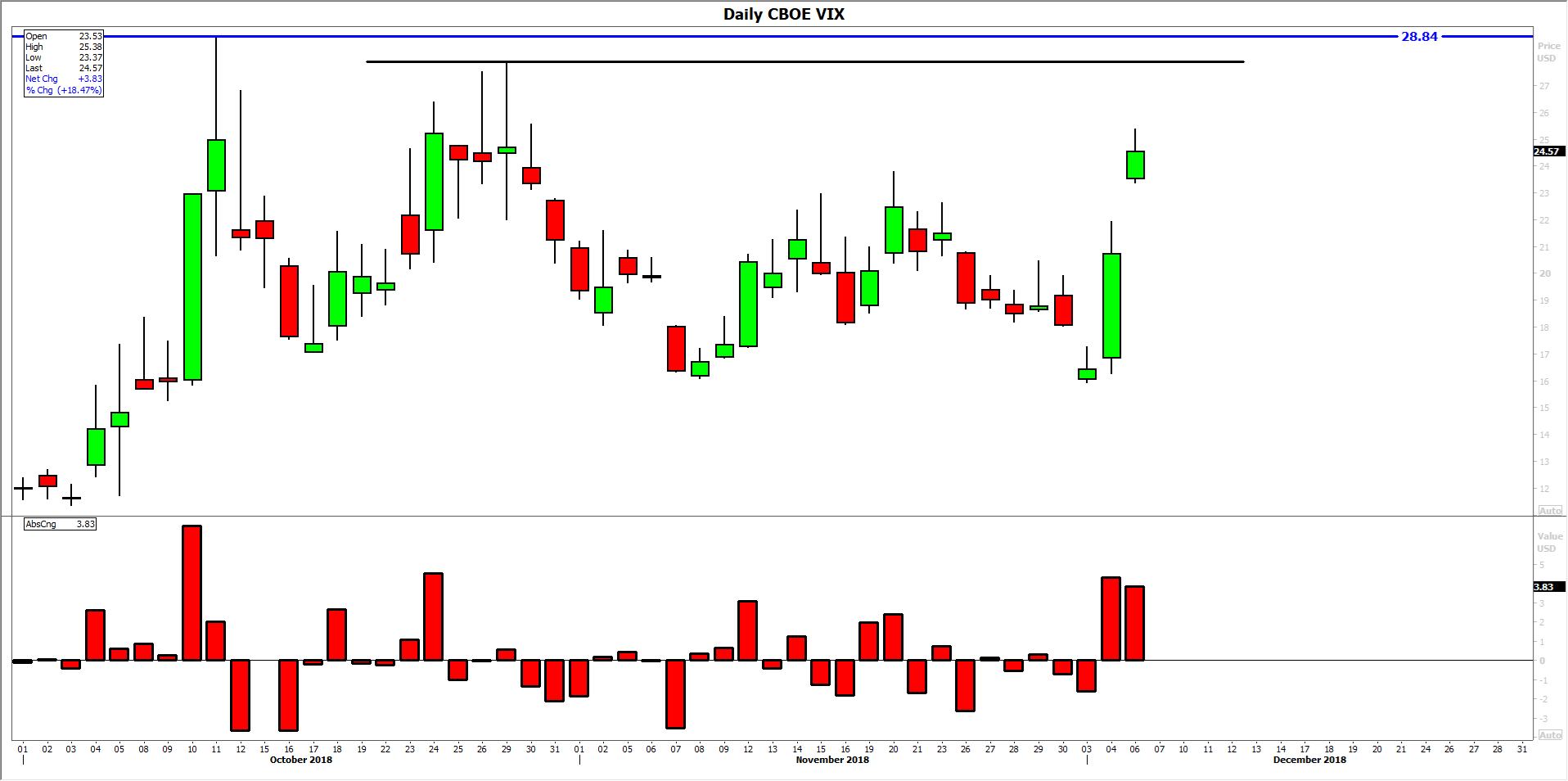

‘Fear gauge' still tethered

With Friday's payrolls in view, soft readings in the run up, including ADP's private assessment add to cross-market gloom. That will deepen if official data also disappoint. The extradition hearing of Huawei's arrested finance chief is also scheduled for Friday. So, one way or another, CBOE's VIX volatility index may have backing to extend a three-session run higher. Should it approach peaks around late 27-29 on the way to the round 30, feedback into aversive sentiment could intensify. In reality, that may be a fairly big ask. Since its second biggest one-day vault of the year in October, the ‘fear gauge' has been active, but relatively restrained. Still, open questions on everything from Brexit, oil, trade and more, offer ample conditions for vol. to go up a gear in the week ahead.

Author

Ken Odeluga

CityIndex

Ken Odeluga has over 15 years' experience of reporting and analysing global financial markets.