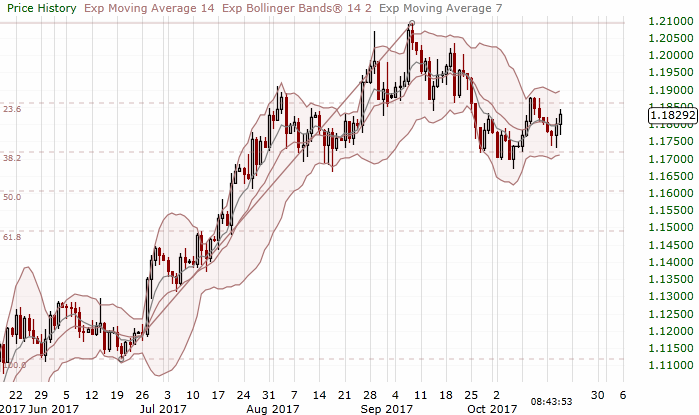

EURUSD: Investors shrugged off Catalonia crisis and focus on ECB

Macroeconomic overview:

-

The Federal Reserve said the pace of growth in the U.S. was “split between modest and moderate” in its latest snapshot of the economy known as the Beige Book. The report covers August 29 to October 6.

-

A stable economy and the tightest labor market in years, however, did little to move the needle on inflation. The Fed characterized the increase in wages and the cost of materials as “modest.”

-

Spain’s central government said on Thursday it would suspend Catalonia’s autonomy and impose direct rule after the region’s leader threatened to go ahead with a formal declaration of independence if Madrid refused to hold talks. The euro climbed to a one-week high on Thursday as investors shrugged off political uncertainty emerging from Spain before a central bank meeting next week where policymakers are expected to reveal plans to unwind their multi-year stimulus policies.

-

The European Central Bank is widely expected to announce the bulk of its tapering decision next week. Inflation remains stubbornly below target, but solid and broadening economic growth is increasing the central bank’s confidence that underlying price pressure will eventually embark on a clearer recovery. Over the last few days, several speeches have provided important hints about the Governing Council discussion at the upcoming policy meeting. We think that within the current QE parameters, the Governing Council could decide to spread the residual firepower over a longer period of time and at a slower monthly pace.

-

We expect net asset purchases to be carried out at a monthly pace of EUR 30bn from January to the end of 2018. This should be more in line with ECB chief economist Peter Praet’s statement that, under more-normal market conditions, the purchases can be executed over a more extended time interval (as opposed to being frontloaded) because investors have become “more patient”. Given that the last two purchase windows have been of six and nine months, the next step could well be of twelve months – if not, it should be at least nine months.

-

Risks to the above-mentioned scenario remain tilted towards lower purchases, mainly due to scarcity issues. Unsurprisingly, the latest ECB speeches continue to indicate that there is no appetite for changes to any of the key parameters of the program. This makes self-imposed limits a binding constraint over the course of 2018. Our estimate of EUR 360bn in net asset purchases next year assumes that the ECB would be able to meaningfully step up purchases of German state bonds, which, however, is a rather illiquid market. If the ECB does not feel confident that will be possible, it would have to settle for a smaller dose of additional QE.

Technical analysis and trading signals:

-

Long lower shadow on yesterday’s candlestick, the rebound above the neckline of head-and-shoulders pattern and today’s continuation of the upward move suggest that short-term momentum is getting bullish.

-

That’s good news for our long EUR/USD position. We do not change anything in our trading strategy. We stay bullish for 1.2400.

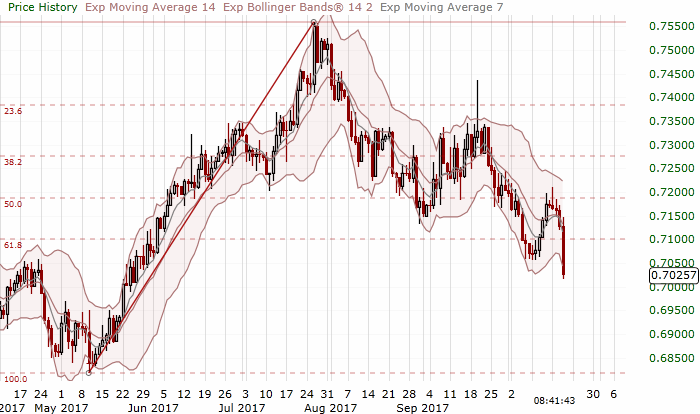

NZD/USD: Jacinda Ardern to be next Prime Minister of New Zealand

Macroeconomic overview:

-

Labour Party leader Jacinda Ardern will be the new Prime Minister of New Zealand. Winston Peters, the leader of the small New Zealand First party which emerged as the kingmaker from the September 23 vote, ended weeks of political guessing games. He agreed to form a new government with Labour Party, ending the National Party’s decade in power.

-

The announcement of the new government drove the New Zealand dollar down to its lowest levels in four and half months, as markets worried about more protectionist policies to come. Labour said it would stick to its campaign promise to change the central bank’s mandate, seek to renegotiate the Trans-Pacific Partnership trade deal and prioritize an effort to ban foreign ownership of certain types of housing.

-

Record net migration of more than 70k annually has fuelled demand for housing in New Zealand, far outstripping supply and pushing house prices prohibitively higher, pricing ordinary New Zealanders out of the housing market.

-

It has said it wants to add employment to the central bank’s mandate, which would mark a big change for the Reserve Bank of New Zealand which was the pioneer of the inflation-targeting regime adopted across the world.

-

New Zealand First leader Winston Peters, who has been offered the role of deputy prime minister, said new policy announcements would be up to Ardern, but gave a foretaste of what may come by saying he expected fewer immigrants to be allowed into New Zealand.

-

Markets are concerned about uncertainty. They worry that curbs to migration and trade could hurt two key sources of New Zealand’s robust growth in recent years. More restrictive trade and foreign ownership could also hurt New Zealand’s reputation as an open economy and antagonize the likes of China, a key trading partner. As a result, the NZD/USD dropped to a near 4-1/2 month low.

Technical analysis and trading signal:

-

The NZD/USD broke below 61.8% fibo of May-July rise and October lows, which opens the way to full retracement of summer move. However, today’s move is the result of political events and it is hard to say whether it will be continued in the coming sessions.

-

Despite higher political uncertainty we think that long-term outlook for the NZD/USD remains bullish on improving demand from China and rising commodities prices.

-

We stay sideways now, but will be looking to use current dips to open a long position soon.

Author

Growth Aces Research Team

Growth Aces

GrowthAces.com is an independent macroeconomic consultancy. They offer you daily forex analysis with forex signals for traders.