EURUSD: Fed to hike rates today, market will focus on CPI data

Macroeconomic overview:

-

Today the Fed is expected to announce another 25bp rate hike, which lifts the target range for the federal funds rate from 1.25% to 1.50%. With this third rate hike of the calendar year, the bank would have met its own forecast for the first time. The post-meeting statement and the updated Summary of Economic Projections will most likely contain only limited changes. Most importantly, we do not see any adjustments to the committee’s median interest rate outlook for the medium term, as recent inflation numbers should strengthen the committee’s confidence in its own, sanguine inflation outlook. With all the written releases being almost unchanged, the market will also focus on Janet Yellen’s press conference. We think that the tone of her comments should be a little more upbeat, mostly due to the fact that inflation has been moving in the right direction, thus vindicating the Fed’s ongoing policy normalization during the summer. In addition, it is Janet Yellen’s final press conference in her current role. After a turbulent time, and after having successfully set the course for the Fed’s policy normalization, she may actually be relieved that she will soon hand over the responsibility to her successor.

-

Democratic candidate Doug Jones won the Alabama Senate special election to fill the seat left vacant by Attorney General Jeff Sessions. After today's election, the GOP only has a 51-49 majority in the Senate. Most importantly at this point is that the passage of the tax bill remains on track. But as the GOP cannot afford to lose another vote beyond Bob Corker, who did not vote in favor of the Senate's version of the bill, we expect the compromise bill that House and Senate leaders are currently working on will be extremely close to the Senate's blueprint.

-

U.S. CPI data will be released today. The US consumer price index, likely rose 0.4% in November as gasoline prices showed an unusual increase for this month. As a result, the headline inflation rate will rise back to 2.2% yoy from 2.0%. The CPI excluding food and energy should have risen another 0.2%, leaving the core inflation rate at an unchanged 1.8% yoy.

-

FX market will likely shrug off the upcoming 25bp hike by the FOMC tonight as the decision is firmly expected. Most of the attention will be on the US core CPI release in the afternoon. Although last month’s figure came in line with expectations, six out of the last eight core CPI releases in the US surprised to the downside. Our expectation for a flat reading of 0.2% mom is in line with consensus and unlikely to provide much support to the dollar. Any weaker number, however, could lead investors to worry about inflation developments in the US and the potential implications for next year’s hiking path. Therefore, a negative surprise would likely lead to a sell-off in the dollar, despite the widely anticipated rate hike by the FOMC in the evening.

Technical analysis and trading signals:

-

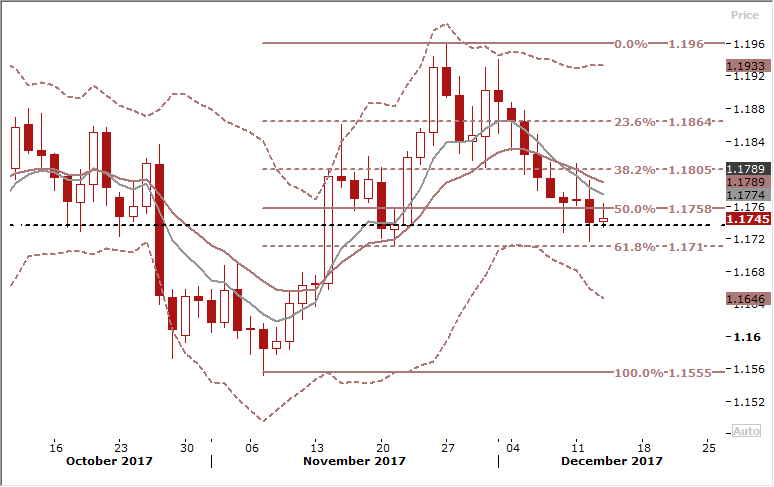

EUR/USD is supported within the daily cloud, 1699/1.1823. While above the base of the cloud there is scope for a rebound towards the top. Slow stochs are beginning to rise from OS levels favoring return to higher levels.

-

We keep our long in play with stop at 1.1685, below the cloud base.

GBP/USD: UK wage growth accelerates slightly

Macroeconomic overview:

-

Pay growth for British workers quickened slightly in the three months to October but there was another drop in employment, official figures showed, suggesting employers are turning more cautious as Brexit nears.

-

Britain's economy slowed sharply this year as the 2016 Brexit vote weighed on households and companies, but job creation has largely remained strong until recently.

-

The number of people in work fell by 56k during the three months to October, the most since mid-2015, the Office for National Statistics said on Wednesday. It was the second consecutive fall.

-

The data also showed the unemployment rate held unexpectedly at its four-decade low of 4.3%, against expectations for a further decrease to 4.2%.

-

The Office said workers' total earnings, excluding bonuses, rose by an annual 2.3% in the three months to October, compared with 2.2% in the three months to September. The market had expected to see no improvement. That was weaker than the latest 3.1% reading of British consumer price inflation in November and the Office said wages in real terms dropped by an annual 0.2%.

-

Including bonuses, wage growth picked up to 2.5% from 2.3%, as expected, although the annual comparison was flattered by weak bonus payments this time last year.

-

The Bank of England increased interest rates for the first time since 2007 last month as most of its policymakers thought the steep fall in unemployment will soon start to push up wages. The BoE's next rate decision announcement is due on Thursday. We expect a 9-0 vote to remain on hold. Overall, this should be a non-event.

Technical analysis and trading signals:

-

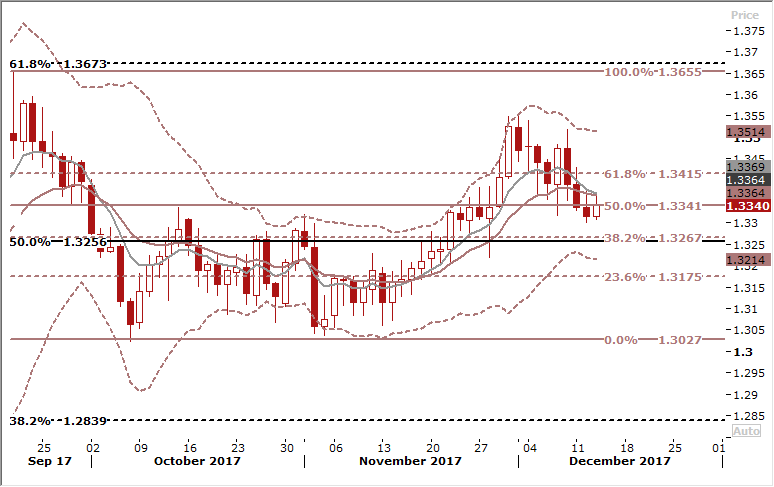

7-day exponential moving average touched 14-day ema and a negative cross could be a bearish signal. On the other hand, a break above 21-dma at 1.3345 is giving bulls a chance for continuation of a rise from November.

-

In our opinion the GBP/USD outlook is bullish, however the risk on this pair is high due to uncertainty over Brexit negotiations.

Author

Growth Aces Research Team

Growth Aces

GrowthAces.com is an independent macroeconomic consultancy. They offer you daily forex analysis with forex signals for traders.