Equity players continue to expect tax reform

Outlook:

The big news today will be the release of the last Fed minutes, although experience should teach us the minutes will not deliver a single clue on the timing of the next hike. The market still does not buy the idea of March, although the probability is higher at 43%, according to Bloomberg.

It's a little hard to swallow that the suggestion LePen has a real chance in France pushed the French- German yield spread from 30 to 80 bp and reports of a Greek budget deal—without the IMF—took the 2-year yield down a whopping 154 bp. But seemingly realistic talk of a March hike in the US still gets the raspberry from the bond gang. One wag pointed out that between March and June, we do have a May FOMC.

To get a feel for sentiment in the US, just look at equities. Equity players continue to expect tax reform, deregulation, fiscal stimulus and even health care reform, town hall protests notwithstanding and a complete offset of likely rising raters on any date. Attention is increasingly focused on the Trump speech to a joint session of Congress on Feb 28—next Tuesday.

This is a huge agenda and it would be silly to expect a comprehensive plan covering everything that can then get passed in Congress. Health care reform is the thorniest issue. Congress entertained some 50 bills over the years to repeal the Affordable Care Act, but failed to get it done and more tellingly, failed to offer a replacement. We have some replacement bills floating around but support has not coalesced around any single one. The sad and funny truth is that voters love Affordable Care and hate Obamacare, not appreciating they are the same thing. They want reform, not repeal, according to protesters at town halls. One poor Senator told his town hall audience that he has to oppose Affordable Care or he would get "primaried," meaning the Republican party would put up someone else and he would lose his seat.

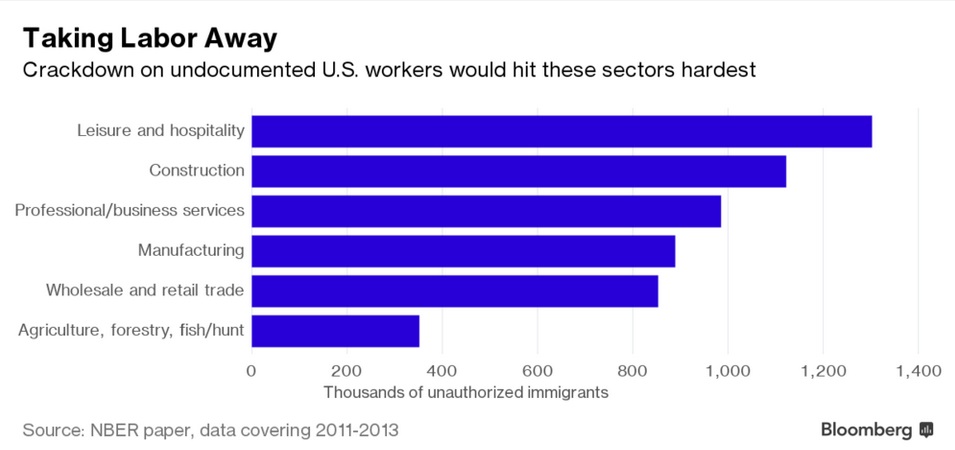

Then there's the cost. We already know the Trump administration plans to fiddle the numbers but it's not clear how it will hide the cost of the new crackdown on illegal immigrants (and how it will pay to build the wall). The new crackdown will entail hiring another 15,000 border and immigration agents at a cost of $21 billion, by Trump's own accounting. One report (Bloomberg) has it that departing immigrants will strain an already tight labor market and cost the economy as much as $5 trillion over 10 years. See the table. We say so much of the labor is in the gray market that the NBER data can't be accurate. In other words, it could be worse, economically speaking.

We must expect a flood of heart-breaking stories, but there are three sorry truths in this new development. Trump promised the crackdown in the campaign and is keeping his promise. But whether it will be well-managed is something else. Local border and immigration officials have wide discretion. The Obama version was targeted to proven criminals. The Trump version already looks indiscriminate. If you are undocumented, off you go, no mitigation allowed. The immigration system was already badly managed and horribly cruel and unfair. It's not going to get any better under Trump. (The only other big management issue pertaining to humane treatment is the Veterans Administration. We have yet to hear how Trump is going to fix that.)

And finally, while a vocal minority object to indiscriminate deportations, the majority don't care all that much—or else they support it. This means illegals will go underground. It also means regular local police and other law enforcement agencies need to become an arm of the Feds lest "haven" cities lose federal funding for all kinds of things—schools, hospitals, roads, etc. If cities like San Francisco push back, how will they replace federal money? In a word, taxes. And of course sales and property taxes are regressive, hitting the poor harder than the rich.

To return to FX itself, the dollar correlation with oil or gold or anything else is getting re-jiggered by the political factor. Let's say ABN Amro is right and oil prices fall back to $30 on OPEC failing to extend the output cuts past June or on US production rising even further. Analysts will claim the dollar is up because oil is down, just as they are now claiming gold is down because the dollar is up. But gold is up chiefly as a safe haven from political uncertainty, which you might think should affect the dollar equally—but does not. The disappearance of the negative Trump effect is really pretty amazing.

And we are also seeing some curious emerging market effects of the rising and resilient dollar. The Mexican peso, trashed by Trump, is coming back in a curious way. The FT reports the Mexican central bank "surprised markets by unveiling a $20bn currency hedging programme that would allow policymakers to combat volatility in the peso without dipping into their foreign exchange reserves." The peso is already at a 3-month high, the best since the Trump election, but Banxico is not taking any chances. It will auction US dollar hedges, starting with $1 billion on March 6.

An ING analyst told the FT he questions whether the program will suffice to "offer protection for the $230bn of portfolio capital or $500bn of FDI in Mexico." The SocGen analyst notes the similar Brazilian program was much bigger, peaking at $116 billion in early 2015. The dollar/peso initially rose on the story but is retreating already this morning.

We still don't know whether NAFTA will get dumped altogether or a softer version will come from Trump's "deal-making." But it's certainly interesting that EM's are not asleep at the switch and seeking ways to manage currency effects without changing interest rates, intervention or capital controls. Who else will step up, and how?

Back on the ranch, the euro is under attack, despite decent economic data, on political uncertainty. This can only grow until all those elections are finished in April and the advice, sell euro rallies, is becoming universal. Similarly, there is no benefit to be had from following the Japanese data or the Bank of Japan's QE tweaking—the dollar/yen is a one-way street headed for 115, 120, maybe 125.

Trump's Tweets: "When I use a word," Humpty Dumpty said, in rather a scornful tone, "it means just what I choose it to mean—neither more nor less."

"The question is," said Alice, "whether you can make words mean so many different things."

"The question is," said Humpty Dumpty, "which is to be master—that's all."

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 113.06 | SHORT USD | 01/05/17 | WEAK | 115.93 | -0.18% |

| GBP/USD | 1.2455 | LONG GBP | 01/24/17 | WEAK | 1.2451 | 0.03% |

| EUR/USD | 1.0503 | LONG EURO | 01/10/17 | WEAK | 1.0587 | 1.32% |

| EUR/JPY | 118.74 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 2.32% |

| EUR/GBP | 0.8432 | LONG EURO | 02/06/17 | WEAK | 0.8605 | 0.68% |

| USD/CHF | 1.0128 | SHORT USD | 01/05/17 | WEAK | 1.0113 | 1.04% |

| USD/CAD | 1.3174 | LONG USD | 02/22/17 | NEW*STRONG | 1.3253 | 0.00% |

| NZD/USD | 0.7166 | LONG NZD | 01/10/17 | STRONG | 0.7014 | 0.26% |

| AUD/USD | 0.7684 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.64% |

| AUD/JPY | 86.88 | LONG AUD | 10/06/16 | STRONG | 78.48 | 1.12% |

| USD/MXN | 20.0854 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 3.49% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat