End of week wrap : Tension between rates and equites roils sentiment

MARKETS

Assuming no last-minute sell-off, US stocks are unchanged Friday and on pace for a modest gain for the week as investors continue to navigate a bumpy path amid the ongoing bank uncertainties in the US and Europe, a 'dovish hike' from the Fed, and a US stock market that still trades at a P/E close to 18X -- not cheap by historical standards.

This week's story was one of continued tension between rates and equities while uncertainties around the stability of some banks linger.

On the rates side, the Fed hiked. Still, it also set a relatively subdued tone for the economic outlook, with its 4Q23 GDP growth forecast at a scant +0.4%. And the FOMC now forecasts a peak rate of 5-5.25%, a feat we now refer to as Entering The Mission-Impossible Zone.

While higher credit conditions could substitute for rate hikes, the asset market impression of these two arcs is very dissimilar. Hence, we remain cautious about buying risk when front-end rates are sinking faster than the Titanic, a straightforward get-out-of-dodge signal these days.

Looking further down the drain, however, it's hard not to be concerned about the medium-term availability of bank lending in the real economy. And this has opened up a whole new can of worms - which, broadly defined in a practical sense- is likely to worsen.

An essential fact, however, is that the latest Lending standards were already tight heading into the current bank stress, suggesting they may not get as incrementally tighter as some expect. Several bank economists continue to remind investors that the labour market is very tight, suggesting that people who get laid off in the current economy will have an easier time finding a new job than in past slowdowns. And they do not expect the unemployment rate, for example, to rise by much even as growth slows throughout 2023

Bank borrowing through the discount window and Bank Term Funding Program (BTFP) stabilized at last week's level. Still, the composition moved toward the BTFP (this was released in H.4.1 yesterday). Today (4 15 pm EDT), we will get the H.8 release, which shows banking lending. The release will only be as of 15th March, so it may be too early to look for any signal. Still, this release will become especially important as the Fed SEP forecasts implied weak sequential growth beyond Q1.

Financial stocks are so far flat on the week. On the stock's side, the market remained largely resilient this week (at the Index level), with the S&P 500 still up over 2% for the year. And pockets of Tech remain the favourite 'defensives' in the current environment as lower rates support an improved outlook on future earnings.

For now, markets are pricing in a large but craggy hit to growth focused on small businesses. And the S&P 500 has been resilient because most of its market cap is concentrated in businesses away from these stress points -- like Tech and large corporations.

Saddle up as we close out March next week, which means the 1Q 23 earnings season is right around the corner. And that means markets have an opportunity to refocus their attention on corporate fundamentals rather than macro impulses. The latest bank stress may yet translate into corporate fundamentals should we see a sharp pullback in lending that spreads beyond regional banks and their SMB customers. But in the meantime, inflation issues (pricing power, cost control, labour availability) will likely dominate corporations ate 1Q conversation.

FOREX

A healthy dose of policy skepticism, particularly towards those pulling the strings behind the red, white and blue curtains at the Fed and Treasury, continues to weigh on the dollar and US equity sentiment. And amid the shifting mix of tightening with the possibly willing to let tight credit rather than Fed hikes do the heavy lifting, the dollar looks prone.

Fed officials believe tighter credit conditions could substitute for rate hikes to slow the economy, but each policy produces a different arc for the US dollar.

Unlike a higher risk-free rate of return via 10-year bond yields, which typically support the US dollar when the Fed hikes, tighter credit conditions lower the expected real rate of return on domestic assets, deter portfolio flows and weaken the currency.

GOLD

And gold is trading on fear in the banking sector even if a run of big banks is improbable. But fear is contagious, and contagion always finds a friend in gold.,hence fear is the essential medium to short-term driver for gold.

Fear is contagious, and contagion always finds a friend in gold. But the catalyst for the current rise in 'fear' was not only banking and funding stress, to levels last seen in March 2020, but also a sharp rise in the market-implied probability of a US recession in the next year.

Gold has rallied by over $150/toz over the past two weeks on the back of banking stress and lit up by US 2-year yields recording the largest decline since 1987, which triggered a significant risk appetite reversal.

OIL

Paper oil, to a degree, is also bouncing around on fear in the banking sector, even as financial contagion risk did not morph into physical demand risk. After all, the markets witnessed the most prominent bank collapse since 2008 and the quickest and most significant repricing of a Fed curve ever. Understandably oil traders drew a straight line from the oil market meltdown during the 2008 GFC.

We suspect professional oil traders are just as worried about another VAR shock as about recession odds. They fear the rise of another liquidity event when any signs of any Bank risk hit. In London, for example, oil fell when concerns about the health of Deutsche Bank hit. We think this is a lingering by-product of last Friday's "Negative Gamma Event as bullish oil traders get jumpy even on small interday selling moves, knowing the significant open interest on Brent put strikes at $70 and $65. could create another downside volatility event like we saw last Friday.

Fundamentally not too much has changed on the supply-demand front, and we believe as the dust settles, and the smoke clears, oil traders will shift more aggressively into an OPEC patience trade.

While some investors may short oil as a recession hedge based on the collapse in oil prices during the last recession, however, Asia consumption has increased markedly since 2008, suggesting even in a minor OECD recession, the low elasticity of demand, along with oil prices mobility-driven nature, suggests selling oil does not offer the best hedge for how the next hypothetical recession is likely to play out in oil markets.

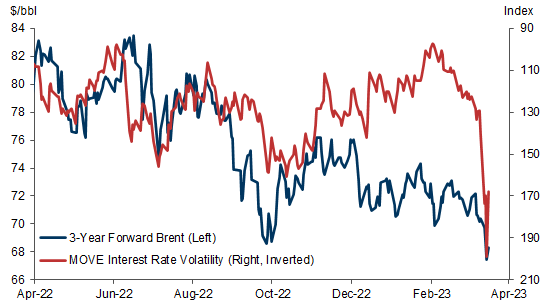

As markets stand right now, and assuming broader rates volatility drops as oil prices remain tied to the hip of the MOVE index, our bullish play is for OPEC to stay the course and with the weaker dollar allowing better China fundamentals to shine through. And bullishly, we think oil markets could enter a small global deficit as soon as June due to OECD skirting a 2023 bank-driven crisis recession, thirsty Asia buyers and a fall in Russian production.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.