Emerging Markets Briefer: Global recession fears and monetary easing to drive emerging markets

Q3 19 turned out to be a roller coaster for global risk sentiment and emerging markets . After fortified hopes of an earlier trade deal between China and the US in June, US President Donald Trump shattered risk sentiment in August by announcing new tariffs on Chinese goods. China retaliated. Negative sentiment has been fuelled further by geopolitical turmoil in the Middle East after some European nations, Saudi Arabia and the US accused Iran of the heavy drone attacks on Saudi oil production facilities. While we saw some support from the looming oil price shock for commodity producers such as Russia, net oil importers - India and Turkey - came under significant pressure.

Disappointing manufacturing data from the EU and the US, combined with 'not dovish enough' stance by the ECB and Fed, have weighed on emerging markets through fears of looming global recession, fuelled by unresolved trade war issues. German recession concerns are putting pressure on economic growth in the Central and Eastern European economies, which enjoyed solid expansion in H1 19. The recent unleashing of a trade conflict between the EU and US will hurt economic sentiment in Czechia and Hungary, but impact Poland less.

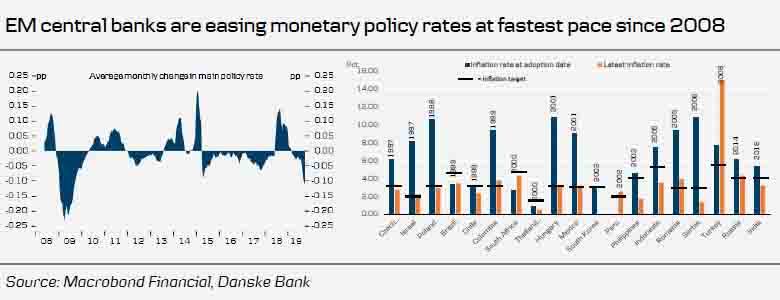

However, the central banks in emerging markets have not just been observers this time. They started to front-run the markets and monetary policy makers in advanced economies by delivering notable cuts across the continents: 14 out of 21 major emerging markets have now cut their policy rates. In addition, China has both cut its reserve requirement for banks and enacted a small policy rate cut in its new monetary policy framework. The only exceptions to this vigilant easing are either EMs under pressure such as Argentina or the Eastern Europeans such as Poland and Hungary, which have prolonged their dovish rhetoric.

We spend a lot of time looking at monetary easing in the advanced economies . However, now, the majority of the global economy belongs to the emerging market world. The Fed's easing in particular will support the emerging markets in 2020. We expect the easing will support domestic demand and help soften the external manufacturing shock in emerging markets but also benefit the global economy more broadly.

Economic growth in emerging markets is set to accelerate in 2020-21 as monetary stimulus gains traction. Given stabilisation in currencies across many emerging markets, accelerated inflation is set to calm down further in 2020, we believe. However, some global yellow lights could still turn red, affecting emerging market growth.

Author

Danske Research Emerging Markets Team

Danske Bank A/S