Eastern Europe leading the lift-off for rates

-

Strong recovery in the making on back easing restrictions and strong global demand.

-

Inflation pressures prompting a change in central bank narrative.

-

CEE FX to benefit from CB hawkishness.

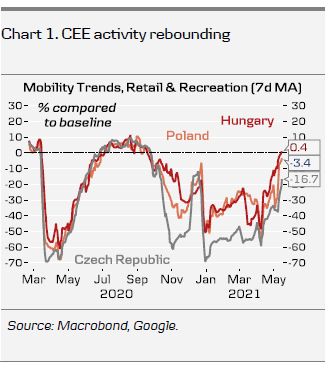

The CEE countries are gearing up for a fast recovery after coming to terms with the third COVID wave. In both Czech Republic, Poland and Hungary, the daily cases are back to Autumn lows as restrictions have worked together with warmer weather and vaccine rollout. On the latter, Hungary is standing out, as the early decision to use the Russian Sputnik vaccine has advanced vaccine coverage to the same levels as in the US and UK, with Poland and Czech Republic closer to the EU average. This has allowed for a relatively early easing of restrictions in Hungary, prompting strong rebound inactivity, but a similar picture is emerging in Poland and Czech Republic too (Chart 1).

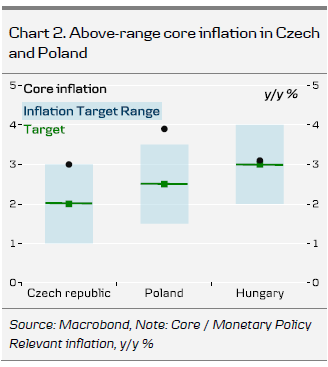

Furthermore, the countries are witnessing persistently high inflation. There are clear signs of the manufacturing sector overheating in Poland, where supply constraints and labor shortages are limiting output. Both core and headline inflation is now above the central bank’s target band at 3.9% y/y (Chart 2). Furthermore, the recent rise in commodity prices globally has an accentuated effect on CEE countries’ inflation, as they have notably higher weight for goods in consumer price indices, compared to the Euro Area or the US.

While expansionary monetary policy and negative real rates have supported the recovery, the heightened inflation pressures have turned the local central banks more hawkish. The National Bank of Hungary used to be the more dovish of the bunch, but the deputy governor Virag surprised the markets this week by calling for preparation for a rate hike, and the Czech central bank is targeting a rate hike in June already. The Polish central bank remains divided on the issue, but the more hawkish members are calling for a hike already this summer. The dividend policy committee makes us a bit more hesitant on the upside for PLN compared with the two others but overall we see stronger CEE currencies.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.