Don’t Rush Your Swing: Inventory Outlook & GDP

Executive Summary

Golf legend Bobby Jones once said, "You swing your best when you have the fewest things to think about." Inventories play an important but choppy role in short-run variations in growth. As we gauge the swing-factor role of inventories in the second half of 2019 and beyond, we have a lot to think about, including Boeing's delivery halt, how businesses will adjust their stockpiling plans in the context of an escalating trade war and worries about late-cycle business spending dynamics and the risk of recession. Our base case is that inventories will help pull the sled for GDP growth in the second half of 2019, but we see potential for a drawdown in 2020 which could weigh on growth, perhaps substantially so.

Don't Rush Your Swing

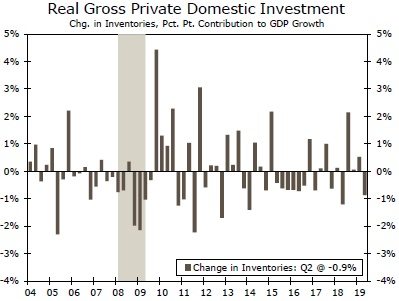

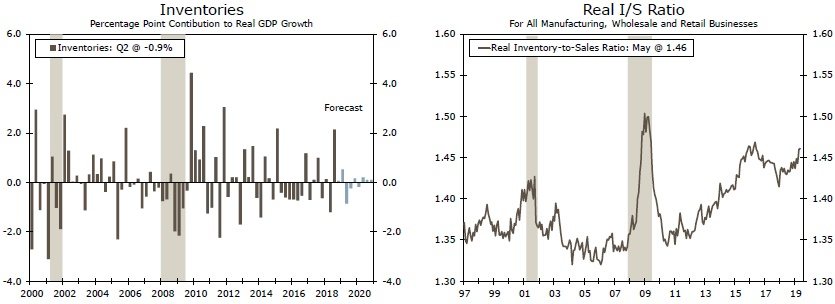

Inventory swings can make or break a GDP report, although they are notoriously difficult to forecast. In the past four quarters, inventories have lived up to their reputation. The contribution to topline GDP growth has ranged from a boost of over two percentage points to the nearly one point drag in Q2 we warned about in our last published note on inventories (Figure 1). 1

If inventories increase unexpectedly, future production is likely to be curtailed to prevent an oversupply of goods. Conversely, a suddenly lean level of inventories would signal the need for greater output to meet demand. Fine-tuning the balance between production and sales is not easy, however, and therefore inventory growth can bounce around wildly from one quarter to the next.

Inventories' influence on GDP growth is based on how quickly stockpiles are growing (or contracting) compared with the prior quarter. When inventory growth picks up, it reflects an increase in production that was not captured in sales, i.e., produced but not consumed that quarter. Therefore a faster rate of change in inventories generates a positive contribution to GDP growth that quarter. If businesses are not adding to inventories as quickly as the prior quarter, it signals a slowdown in production not captured in final sales. Therefore even if inventory growth is positive, it can still detract from GDP growth if less positive than the prior quarter.

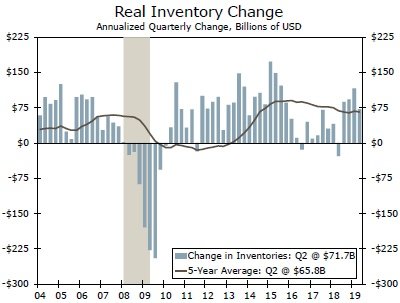

At a $72B annualized pace in Q2, inventory growth was closely in line with its five-year average (Figure 2). Ordinarily, that would suggest inventories are poised to fade into the background as a major influence on GDP growth over the next few quarters. After all, the recent pace of inventory growth no longer looks particularly extreme, so any deviations from last quarter's growth are likely to be small. But these are hardly ordinary times.

For one, the high value of new 737 MAX aircrafts means Boeing's issues are large enough to singlehandedly move the inventory outlook. Shipments of the company's best-selling model are likely to be suspended through at least the end of the year even as production has proceeded. While Boeing has scaled back the rate of production, any completed 737 MAX models are still ending up in inventories until they can be shipped to buyers, which means an added boost to overall inventory growth as a result. Assuming Boeing has been producing about 36 MAX planes per month, we estimate that would equate to an additional $39B annualized of inventory per quarter on its own.

Beating the Tariff Clock

Less clear is how the most recent escalation in the trade war with China may impact inventories. For a business trying to manage the uncertainty, one approach to limit tariff costs would be to get product through customs before the import taxes take effect. A second-half rush to beat the tariffs therefore could lead to stronger inventory building. Although bringing more inventory ashore sounds straightforward, a number of logistics would need to be considered, such as suppliers' production capacity, shipping capacity and where the extra goods would be stored. Cash flow and financing could be additional hurdles.

To evaluate the potential for a tariff-related inventory build before year end, it is useful to look at recent tariff episodes. Anecdotally, clients have told us that they brought in extra inventory to avoid upcoming tariffs. Recent Beige Book reports from the Federal Reserve have similarly been sprinkled with comments about some businesses trying to get ahead of tariffs. But has this been enough to move the inventory needle?

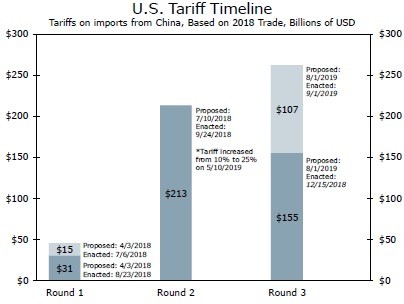

Referring back to Figure 2, one can see inventory growth ramped up over the second half of 2018 and remained exceptionally strong in the first quarter of this year. The timing coincided with the Trump administration beginning to take specific aim at China. In April 2018, tariffs on an initial $50B of imports were announced and went into effect over the summer (Round 1), while in July the situation escalated with the administration announcing 10% tariffs on about $200B of imports to go into effect in late September (Round 2). The administration also threatened that the 10% tariffs on Round 2 goods would rise to 25% at some point in the future (which occurred on May 10, 2019).

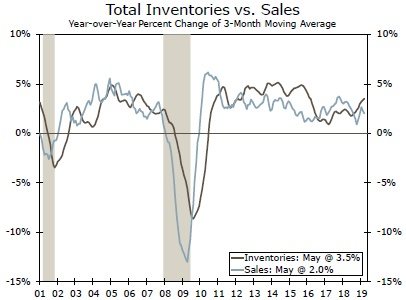

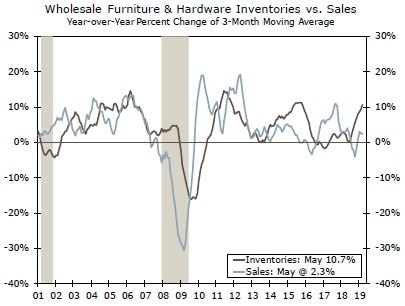

Yet the build-up in inventories over this period also coincided with a noticeable slowdown in sales (Figure 3). Arguably, wholesalers would be more directly and immediately impacted than manufacturers and retailers, particularly in sub-industries like furniture and hardware, which were exposed to tariffs under Round 2. While inventories have taken off within these sectors, the build has also come amid a slowdown in sales. (Figure 4).

The weakening sales environment suggests that the rise in inventories around the time the China tariffs kicked off was largely unintended. Indeed, while recent Beige Book reports from the Fed have included a few comments about inventories being pulled forward, they have also included plenty of comments about inventories rising due to slower sales. While some individual businesses may have hustled to get product on shore ahead of tariffs taking effect, the macro impact on inventory building is not terribly consequential, at least not yet.

Formula to Keep in Mind: Round 3 > Round 2

Might the most recent round of announced tariffs have a more meaningful impact on inventory building? This seems within the realm of possibility. First, the Trump administration has a more clearly defined track record on tariffs than it did last April when it first floated tariffs aimed specifically at China. Last summer, businesses may have had more doubts about whether the administration would follow through on implementing tariffs on such a large swath of goods, and decided bringing inventory in earlier was not worth the effort and cost. It would be reasonable for businesses to take President Trump's tariff threats more seriously now, especially with negotiations reportedly deteriorating over the past several months.

Second, the latest round of tariffs is simply bigger than past rounds. According to the Office of the U.S. Trade Representative, nearly $300B of goods are included in Round 3 versus about $200B in Round 2. By our calculations, the value of Round 3 covers closer to $260B of goods, but is nonetheless larger than prior rounds. Moreover, many of the Round 3 items will have more time to come ashore. About 60% of the Round 3 tariffs will not take effect until December 15. This gives importers 136 days to bring goods stateside, compared to 76 days for the prior round (Figure 5).

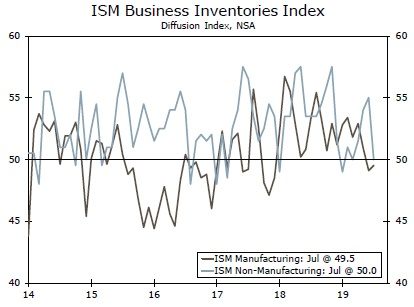

Any impact of firms racing to get ahead of upcoming tariffs, however, is likely to be at least partially offset by firms whose tariff clock has already struck midnight. Businesses whose products are already subject to 25% tariffs may try to keep inventories extra lean in the coming months in hope that a deal lifting tariffs is reached soon. More broadly, businesses may hold back on inventory building with the escalating trade tensions and recent market volatility clouding the sales outlook. The ISM surveys show manufacturers' inventories declined the past two months while inventory levels at non-manufacturers were unchanged in July (Figure 6).

Paved Roads and Good Intentions

Currently we expect inventories to have a relatively muted impact on growth in the second half of the year (Figure 7). We expect inventory growth to ease up from the $94B annualized pace averaged in H1, which brought the real inventory-to-sales ratio to a three-year high (Figure 8). However, we see the risks to this call as skewed toward the upside. We could see more inventory building and a larger contribution to GDP growth in part from a greater intended build in inventories, as companies subject to 10% tariffs beginning December 15 take efforts to stock up before the deadline. The more generalized threat of 25% tariffs on those items at some yet-to-be-determined point may give companies further incentive to load up.

A smaller, but still present risk: an unintended build in the second half if constant headlines about both tariffs on consumer products and a potential recession dent consumer confidence and subsequently sales.

Is There a Reckoning Coming in 2020?

Intended or unintended, inventories will eventually need to be right-sized with sales. That opens up the potential for a drawdown in the first half of 2020, or at the very least a slower rate of additions. Already we expect to see inventories weigh on GDP growth in the first quarter of next year as we assume Boeing resumes shipments of its 737 MAX planes, but the total drag from inventories could end up being larger if stocks pile up more before the end of the year.

The upshot is that inventories look to stay true to their role as a major swing factor in GDP growth. Rather than inventory growth settling down, we see the potential for a pickup in the second half of the year that would give a temporary boost to GDP growth. Inventories will eventually need to be unwound, however. That reckoning will likely mean a pullback in production or imports, and means inventories could be a major drag on GDP growth in 2020.

Author

Wells Fargo Research Team

Wells Fargo