Do European NPLs Pose a Global Economic Risk?

Executive Summary

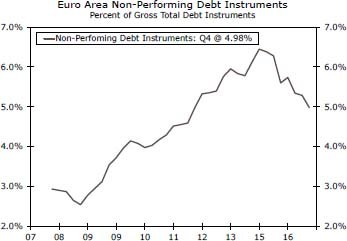

Non-performing loans (NPLs) in the Eurozone rose markedly between 2009 and 2015 due largely to weak economic growth that permeated euro area economies during those years. The NPL ratio has receded over the past two years, but it remains elevated at nearly 5 percent. Could a NPL crisis in the Eurozone derail the expansion that is underway in the global economy?

Greece and Cyprus have truly extraordinary NPL ratios at present, but the relatively small size of their banking systems means that those economies probably do not represent much of a systemic risk to the overall financial system in the Eurozone. In our view, Italy represents the most serious systemic risk to the European financial system given the high absolute amount of NPLs that infect the Italian banking system. But unless the Italian economy falls back into recession, which we do not anticipate, a NPL crisis in Italy does not appear to be imminent. If the Italian banking system needs to be recapitalized, should that eventuality occur, the Italian government could call upon the financial resources of the European Stability Mechanism to lend support.

NPLs in the Eurozone Are Receding Although They Remain Elevated

We recently wrote two reports in which we looked at debt issues in developing economies.1 We generally concluded that although the recent buildup in debt in the developing world probably would not cause a global financial crisis in the foreseeable future, debt developments in those economies bear watching going forward. But emerging markets are not the only economies that potentially could have debt servicing issues in coming years. Specifically, debt has risen in the euro area as well. Could European banks, where much of this debt is held, experience financial difficulties in the not-too-distant future?

In that regard, the NPL ratio among banks in the overall euro area rose sharply between 2009 and 2015 (Figure 1). Although the NPL ratio has receded over the past two years, it remains elevated at roughly 5 percent. NPL ratios in 18 of the 19 individual Eurozone economies are shown in Figure 2.2 Greece, where nominal GDP is nearly 30 percent below its 2008 peak, leads the pack with a NPL ratio in excess of 45 percent while Cyprus, where GDP has yet to regain its previous peak as well, is a close second at 38 percent. Rounding out the top five countries with the highest NPL ratios at present are Portugal (19 percent), Ireland (16 percent) and Italy (15 percent). Each of these economies suffered deep recessions in the immediate aftermath of the global financial crisis and in the depths of the European sovereign debt crisis in 2011-2013. Weak economic growth usually is associated with deterioration in loan quality.

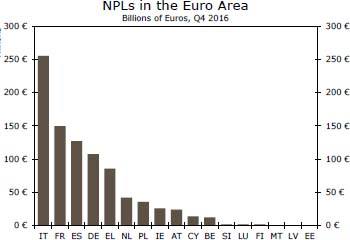

Clearly, the banking systems in Greece and Cyprus have some issues in terms of their elevated NPL ratios. But the Greek and Cypriot banking systems are fairly small and likely do not pose much of a systemic risk to the overall European banking system. The outstanding amount of NPLs in Greece total about €85 billion, which is a manageable amount from a European-wide perspective, while Cyprus has less than €15 billion worth of NPLs (Figure 3). The Eurozone economy with the highest absolute amount of NPLs is Italy (more than €250 billion), followed by France (€150 billion), Spain (more than €125 billion) and Germany (more than €100 billion). These are the individual banking systems that would pose the largest systemic risks to the overall European banking system.

Italy: The "Problem Child" in Terms of European NPLs

We are not overly concerned about the German banking system. The overall NPL ratio in Germany is low at only 2.7 percent, and the German economy is strong at present with the yearover- year rate of nominal GDP growth closing in on 4 percent. A full-blown NPL crisis in Germany does not appear likely anytime soon. With €150 billion worth of NPLs and a ratio of 3.7 percent, France represents more of a potential systemic risk to the overall European banking system than Germany. That said, the French economy has accelerated recently with nominal GDP growth rising to a 6-year high of 2.7 percent in Q2-2017. As long as economic growth in France remains solid, the French banking system likely will not face a NPL crisis, at least not in the near term.

Spain appears to be more problematic than either Germany or France with a NPL ratio of nearly 6 percent at present. Although the outstanding amount of NPLs in Spain has slowly receded over the past two years, it still exceeds €125 billion today (Figure 4). However, Spain is among the fastest growing economies in the Eurozone at present with nominal GDP growth in excess of 4 percent. As long as Spanish economic growth remains robust, both the level of NPLs and the ratio in Spain should recede further.

In our view, Italy clearly is the real "problem child" in terms of NPL issues. Not only does the Italian banking system have the highest absolute level of NPLs (more than €250 billion), but its NPL ratio is elevated at 15 percent. Furthermore, nominal GDP growth in Italy is lackluster at present at less than 1 percent. Although base effects may have depressed the year-over-year rate of growth in Q1-2017, nominal GDP in Italy has not grown in excess of 2 percent on a sustained basis since prior to the global financial crisis.

As shown in Figure 4, the outstanding amount of NPLs in Italy has receded since their peak in 2015, but progress has been slow. Nominal GDP in Italy should accelerate somewhat in coming years. The IMF looks for 2.0 percent growth in 2018 and 2.2 percent in 2019, and these growth rates should be buoyant enough to prevent a rise in the outstanding amount of NPLs in Italy. But a sharp reduction in the NPL ratio likely will not occur unless nominal GDP growth in Italy strengthens significantly, which does not seem to be very likely. In other words, the Italian banking system may remain vulnerable to a potential NPL crisis for the foreseeable future.

Lines of Defense Against a NPL Crisis

So what would happen if the Italian economy were to stall or go into reverse, thereby causing NPLs to rise anew? The reserves of the Italian banking system would form the first line of defense. At the end of 2016, Italian banks had laid away roughly €125 billion worth of loan loss reserves that they could use to write off NPLs. However, employing their total stock of loan loss reserves would leave Italian banks in a much weakened financial position. The Tier 1 capital ratio of the entire Italian banking system is only 11.4 percent, well below the 14.7 percent ratio for the banking system in the overall euro area. Consequently, some Italian banks may need to be recapitalized if they were to encounter more financial difficulties.

In 2016, the Italian government helped to set up a private equity fund known as Atlante to assist in the recapitalization of Italian banks. However, the Atlante fund has only €4 billion or so of equity capital, so it would be insufficient for a complete recapitalization of the Italian banking system. The larger backstop would be found in the European Stability Mechanism (ESM), the organization set up by the European Union at the height of the European sovereign debt crisis in 2012 to provide financial assistance to countries in the euro area. Not only can the ESM provide direct financial assistance to governments, as it has done for Greece, Cyprus, Portugal and Ireland, but it can also be called upon to help governments recapitalize banks, as it did in Spain. The ESM currently has a disbursement of €87 billion, giving it a forward lending capacity of €376 billion. If needed, Italy could tap the ESM to recapitalize its banking system.

Of course, a NPL crisis in Italy, should one occur, would likely lead to financial market volatility not only in Italy but probably across Europe. Growth rates in other large European economies, such as in France and Spain, could weaken, which could lead to a rise in NPLs in those countries. The lending capacity of the ESM could be tested in the event of another recession in the Eurozone.

Conclusion

The NPL ratio in the Eurozone rose markedly between 2009 and 2015 due largely to the economic weakness that pervaded the euro area during those years. It has receded over the past two years, but generally remains elevated near 5 percent. Countries such as Greece and Cyprus have extraordinarily high ratios, but the relatively small size of those banking systems mean that they probably pose little systemic risk to the overall European banking system. In our view, Italy represents the most serious systemic risk to the European financial system given the high absolute amount of NPLs (about €250 billion) that infects the Italian banking system.

That said, we do not think a NPL crisis in Italy is imminent. Italian NPLs have been slowly trending lower, and economic growth in Italy appears to be firming. Renewed recession in Italy, which we do not anticipate at this time, seems to be the most likely catalyst for a NPL crisis in Italy. Although the capital needs of the Italian banking system could be significant in the event that the economy slipped back into recession again, the Italian government could call upon the financial backstop of the ESM to help recapitalize its banking system. The Italian banking system may be weak at present, but it likely will not trigger another global recession, at least not in the foreseeable future.

Author

Wells Fargo Research Team

Wells Fargo