December Fed rate hike back on the table

Outlook:

A Fed rate hike is not expected on Wednesday but December is back on the table, with the CME reporting a 55.8% probability, according to the CME FedWatch tool, from 37.3% a month ago. Analysts are nearly certain the buying program cut-back announcement will be delivered this week. If it's true that rate hikes are back on the table, why are stock markets continuing to be so bubbly? Rising yields should compete with equities, dividend-paying or not. We "should" be seeing a shift into fixed income.

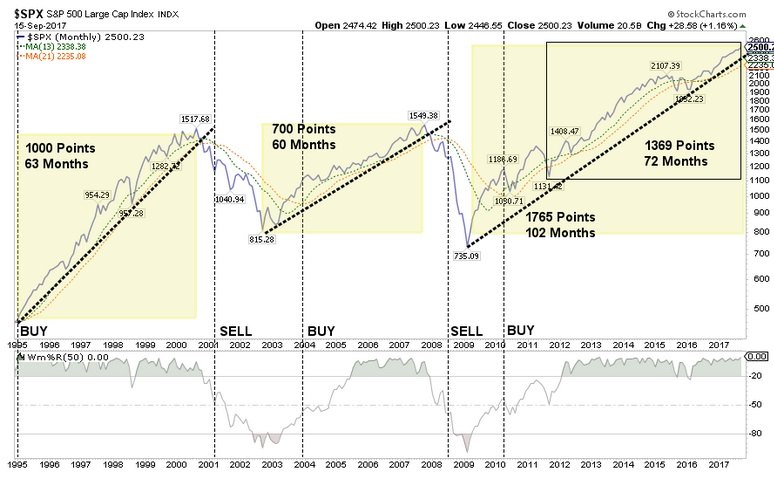

This is not to say a stock market crash is coming and the Fed will be to blame. It is to say that formerly normal relationships are out of whack. Here's a chart that can set your hair on fire, selected by MarketWatch from a series by Lance Roberts at Clarity Financial. We like charts. Of this one, he says "... this bull cycle is on pace to become the longest ever. ‘Regardless, it will end, and like all previously over-valued, over-extended, over-leveraged and overly-complacent bull cycles in history, it ends badly.'"

This doesn't pass the "so-what?" test as spilling over into FX unless we can name what companies will fail, especially in the financial sector. The key is, as usual, who is "over-leveraged." As we have seen in past bull cycle endings, there is always somebody who borrowed too much to speculate and gets called. Who lent to the big borrowers? Or are any of the big borrowers financial institutions themselves using depositors' money, or pensioners' money? Perhaps it will take another giant failure by an insurance company or pension fund manager to remind Congress that the regulations it wants to cut back were devised because man is naturally greedy and greed makes people do stupid/reckless things.

So far the state of the stock market has little to do with developments in the FX market. The outside factor that does have influence is the geopolitical one. The world seems to have brushed off the latest North Korean provocation, judging from the risk-on sentiment seen in most markets. This is almost certainly a mistake. N. Korea is far from over. In fact, we expect military action of some sort before year-end, if not nuclear. See below.

Trump will address the United Nations today. Gee, what can go wrong? Trump is anti-globalist in the first place and critical of the UN for anti-democratic and sometimes anti-US positions. He's not entirely wrong. (Besides, the UN delegates take all the parking spaces in the city.) The WSJ notes the US pays the most of the UN budget, 22% of the core budget ($5.4 billion) and 29% of the peace-keeping budget ($7.3 billion), which the US wants to cut by $600 million. Secy of State Tillerson is promoting a peaceful solution, which is so unrealistic as to be delusional.

You have to wonder if the eurozone will step up, as it did in the case of NATO. The German election is Sept 24 and Merkel is a shoo-in. Remember that she had said Europe should stand on its own two feet. Merkel is thought to be the winner mostly because she is a no-drama, steady-Eddie. We say the contrast with Trump is a factor--not lying and changing positions three times a day. Importantly, Schaeuble will likely remain as FinMin.

It's a busy calendar this week. The Bank of Japan meets on Thursday and Abe is muttering about a snap election. We say we should be thinking about whether he will revive the idea of a constitutional amendment to get rid of the no-war Article 9 ("... the Japanese people forever renounce war as a sovereign right of the nation and the threat or use of force as a means of settling international disputes..."). Nobody is talking about it but it seems like a logical deduction. In the UK, PM May delivers a key speech on Brexit in Italy on Friday.

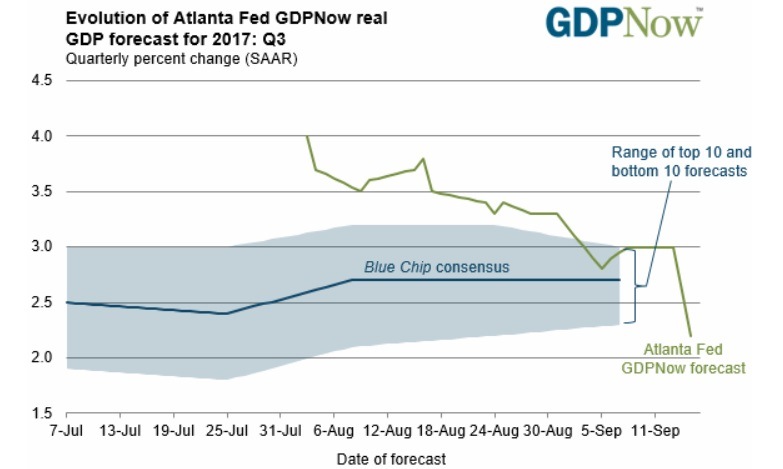

Later today we get the Treasury report on capital flows. This week we also get the housing index, and new and existing home sales, another chance for observations about demographic change in the US (so far it's baby boomers moving and buying while the youngsters are not moving and prefer to rent). We also get a revision of the terrible, awful, really bad GDP forecast from the Atlanta Fed.

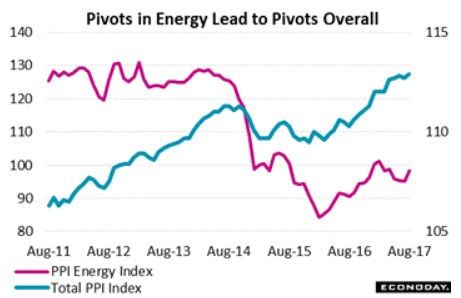

At the end of the week we get the Atlanta Fed business inflation expectations. This is more important than usual because of the hurricanes, which will raise actual and expected inflation by a serious amount in the last quarter. It's a pity the Fed prefers to look at inflation data excluding fuels and food, since those are two things whose price will definitely be going up. It's not just gouging at the gas station. It's Georgia peaches and nuts and Florida citrus fruits, plus all the processing. It's also things like sterno stoves designed for camping, batteries and plain old water. The profiteers will be out in force.

Econoday had a long, serious article on inflation on Friday, saying "hurricane swings will even out over the coming months, not providing the permanent punch that prices need." We are not so sure. See the energy chart. If energy prices continue to strengthen, we all know the knock-on effect.

The dollar is buffeted by opposing forces. On the positive side, we have a sane and reasonable central bank that is going to inspire some confidence (if not as much as the Fed would like) on Wednesday with the announcement of fewer asset purchases, driving home the normalization message. We may also get a cautious word or two about the likelihood of that third hike this year. In addition, the US has some inflation to justify hikes, if barely, but with more to come and an unknown spread nation-wide. Re-building from natural disasters is not the same as an infrastructure plan but can serve as a partial substitute.

Offsetting any idea of a dollar rally is Trump, Trump and more Trump. He keeps changing his stance on just about everything, including immigration, and nobody knows whether the generals can keep him in line on North Korea. At least the stupid twittering has abated. In the background is the on-going developments in the Russia investigation, which makes for gripping cable TV but has yet to bear any actual fruit. In contrast, Europe looks far more politically and economically stable. Look how far we have come! The euro was 1.0340 on Jan 3. Since then Trump has lost and the French won (by dismissing LePen). It's too early to summarize the year, but what was put in place in the first six months shows no sign of reversing. The trend is your friend.

Geopolitical Outlook: The elephant in the room is North Korea. Nobody knows how to get it out. The New Yorker just had one of its lengthy articles on N. Korea by a writer who was visiting N. Korea last summer during the initial provocations, including Trump's "fire and fury" response. A few points to keep in mind: the situation is a continuation of the Cold War. We tend to think the Cold War ended when the Soviet Union broke up, but no. North Korea views the US as an enemy which not only intends to destroy it, but is spying on it to be able to achieve that goal, and it's a military goal. The US will invade North Korea at any time. Only nuclear capability will deter. Mutually assured destruction will be avoided because the two leaders are not suicidal, even if both are unqualified, inexperienced and impulsive.

North Koreans are taught that the US started the Korean War in 1950 when it was the North Koreans who invaded the South over the 38th parallel which had been established at the end of WW II. Ah, but that's too simple. The North Koreans have an entirely plausible story, backed up with documents from military and political figures, that the US treated S. Korea only as a launching pad for an invasion. MacArthur himself misunderstood (or disagreed with) the US mission and famously got fired for it.

The deterrence function of N. Korea's nukes is irretractable. N. Korea will never, ever agree to give them up. Gaddafi gave his up and was killed as part of a NATO-US attack on his country eight years later that allowed the locals to kill him. Current promises by US government officials (like the op-ed by Tillerson and Mattis in the WSJ) that we have no intention of invading N. Korea are simply not credi-ble.

As for an actual war, the N. Korean attitude is that yes, a lot of people will die. But not all of them. And it won't only be N. Koreans who die. National pride requires this stance and justifies the seige mentali-ty (and paranoia) of the leaders and the people alike. Besides, the Americans are weak. Remember the capture of the Pueblo in 1968. The US got its sailors back but only 11 months later and after a US apol-ogy. The president at the time was Johnson, who was distracted by Viet Nam. Pres Clinton was the on-ly US leader who ever came close to getting talks, but then also got distracted.

It's a sign of the dismal state of affairs that the only American with Kim Jong Un's ear is Dennis Rod-man. There is no hope that access to South Korean and Western media will show N. Korean citizens what they are missing, or educate them on history or the principles of democracy—N. Korea bans eve-rything and is amazingly successful at it.

Throughout the New Yorker piece, the author drops breadcrumbs of cultural information, such as the N. Korean belief that Koreans are racially superior. There is a burgeoning black market. Kim Jun Un got to inherit the leadership because his siblings were either female or wusses. He wears his hair in that ridiculous style because it makes him resemble his grandfather. The Korean mentality is both overly dramatic and sentimental.

Bottom line, all the US military initiatives are bad. The best hope is being able to improve our ability to shoot down the N. Korean missiles. We can do it, but the anti-missile capability is short-range and seri-ously unreliable. And trying to shoot one down and failing would embolden N. Korea and give it a PR victory. How is it that we put a man on the moon 48 years ago but can't shoot down a missile?

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.26 | LONG USD | 09/13/17 | WEAK | 110.05 | 1.10% |

| GBP/USD | 1.3549 | LONG GBP | 09/07/17 | STRONG | 1.3075 | 3.63% |

| EUR/USD | 1.1941 | LONG EURO | 06/28/17 | WEAK | 1.1218 | 6.44% |

| EUR/JPY | 132.89 | LONG EURO | 09/13/17 | STRONG | 131.76 | 0.86% |

| EUR/GBP | 0.8816 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 2.40% |

| USD/CHF | 0.9600 | SHORT USD | 08/10/17 | STRONG | 0.9655 | 0.57% |

| USD/CAD | 1.2193 | SHORT USD | 08/24/17 | STRONG | 1.2533 | 2.71% |

| NZD/USD | 0.7300 | LONG NZD | 09/13/17 | WEAK | 0.7282 | 0.25% |

| AUD/USD | 0.8005 | LONG AUD | 08/17/17 | WEAK | 0.7931 | 0.93% |

| AUD/JPY | 89.51 | LONG AUD | 09/05/17 | WEAK | 87.30 | 2.53% |

| USD/MXN | 17.6941 | SHORT USD | 09/15/17 | WEAK | 17.6890 | -0.03% |

| USD/BRL | 3.1089 | SHORT USD | 09/05/17 | WEAK | 3.1409 | 1.02% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat