Bond boys continue to reject Fed's narrative of next rate hike this fall

Outlook:

There's not much point in trying to read the FX tea-leaves today How you interpret the data depends entirely on perspective. So far the bond boys are continuing to reject the Fed narrative of the next hike this fall being a normalization move independent of the inflation forecast.

Besides, demand is high and weighing on yield, whatever the macoeconomists are saying. The 30-year TIPS auction yesterday drew the highest demand since 2011, according to the WSJ. Moreover, foreign demand for TIPS in the form of indirect bidding was 76.1%, the highest since June last year and another bit of evidence that yield-seekers are not entirely abandoning quality (which the Argentina 100-year issue might suggest).

We are still worried about yields. It almost doesn't matter why yields are floppy. The FX market responds to actual differentials. But it can be hard to draw deductions when the things you are comparing influence one another and do not stand alone. Yesterday the 10-year yield flirted with the low of the year, 2.138% on June 14. The WSJ reports "Traders said lower government bond yields in Germany dragged down U.S. yields. Treasury debt continues to offer more attractive yields than government bonds in many developed countries, which has played a big role in holding U.S. long-term government bond yields at very low levels from a historical standpoint over the past few years."

Again, never mind that US yields "should" be higher for a whole list of reasons, not least Fed resolve. The FedWatch tool has the probability of a hike by mid-December at 40.9%. It "should" be over 50%. To be fair, Fed funds futures are a lousy indicator of actual developments, and breakevens are less than reliable (5 or 10-year nominals vs. TIPS) because the market for inflation-adjusted paper is much, much smaller. Forecasts from sentiment surveys are subject to the same faults as any other survey and we have just seen how those can miss by a mile. Besides, we are not supposed to be watching inflation forecasts these days, according to chief Yellen. We are supposed to have faith in the Phillips curve.

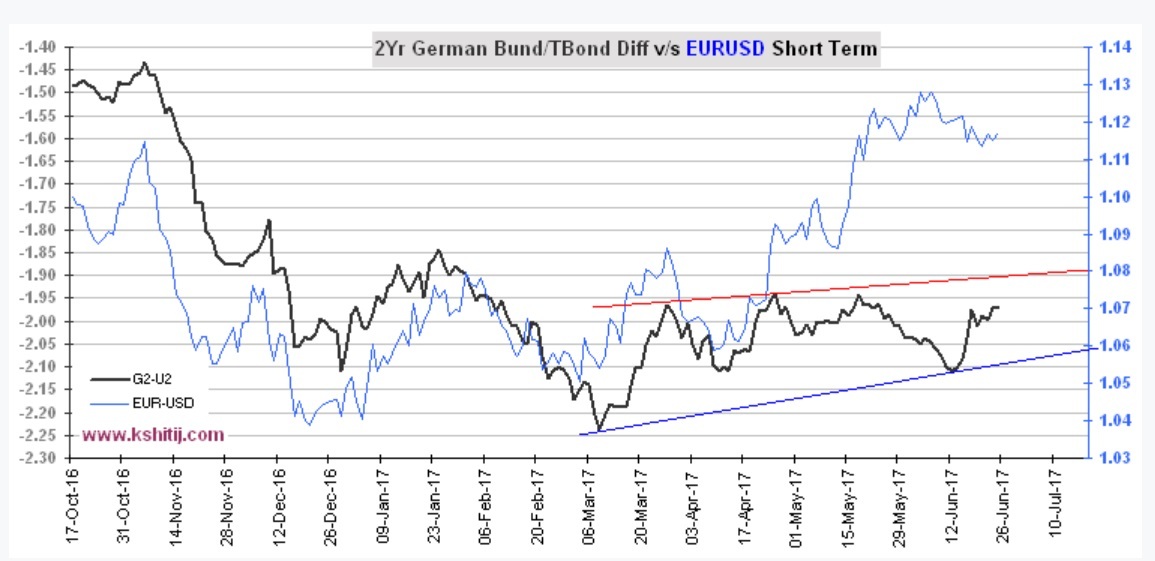

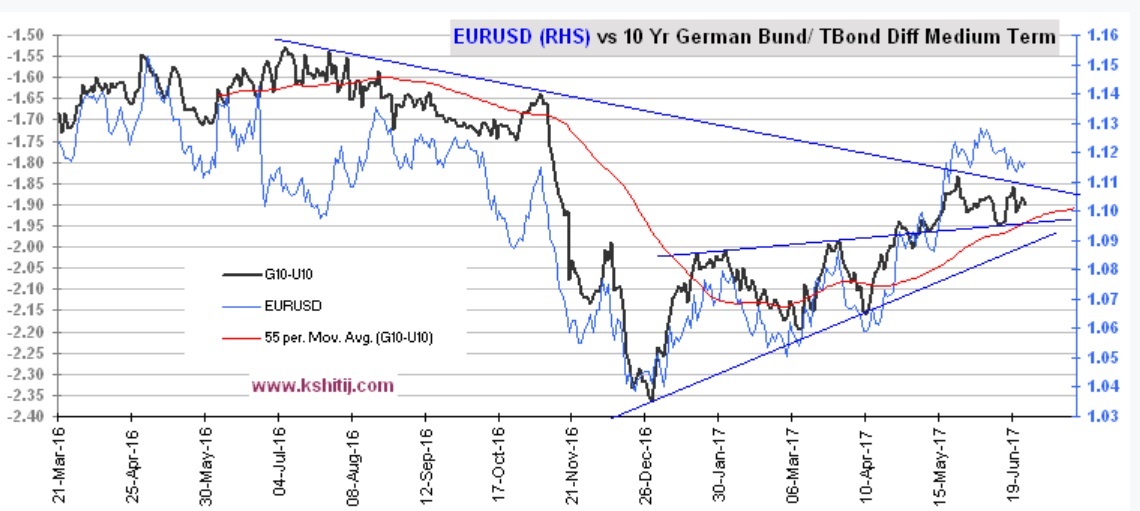

It's messy. The actual differential between the US and the Bund shows the euro is overvalued. This is true in the 2-year comparison and still true on the 10-year, if by less. See the charts.

Alas, that doesn't mean the dollar is going to recover. Divergences can persist for longer than you have the liquidity to resist, to misquote Keynes. ("The market can remain irrational longer than you can re-main solvent.")

News today in the US consists mostly of new home sales, expected to be robust at about 5.4%, and the Barker-Hughes rig count. We will also get wall-to-wall coverage today and all weekend about the new healthcare plan, even though we won't know the true costs and benefits until the CBO speaks on Mon-day.

A potentially big factor is all 34 of the big banks having passed the Fed's stress test, opening the door for higher dividends (among other goodies), to be approved next week. It's the third year in a row the banks qualified, basically convincing the Fed that in the event of another crisis like 2008-09, they would survive and also be able to continue lending. Republicans want to use the success to justify roll-ing back some of the regulations that brought about this outcome. It's a little like saying the barn didn't burn down, let's not renew the insurance policy. To the extent the financial markets expect regulatory cuts, the passing grade could be a factor promoting a stronger dollar. It shouldn't, but it might. Mean-while, the focus on a seemingly healthy banking sector contrasts with a still-troubled banking sector in Europe.

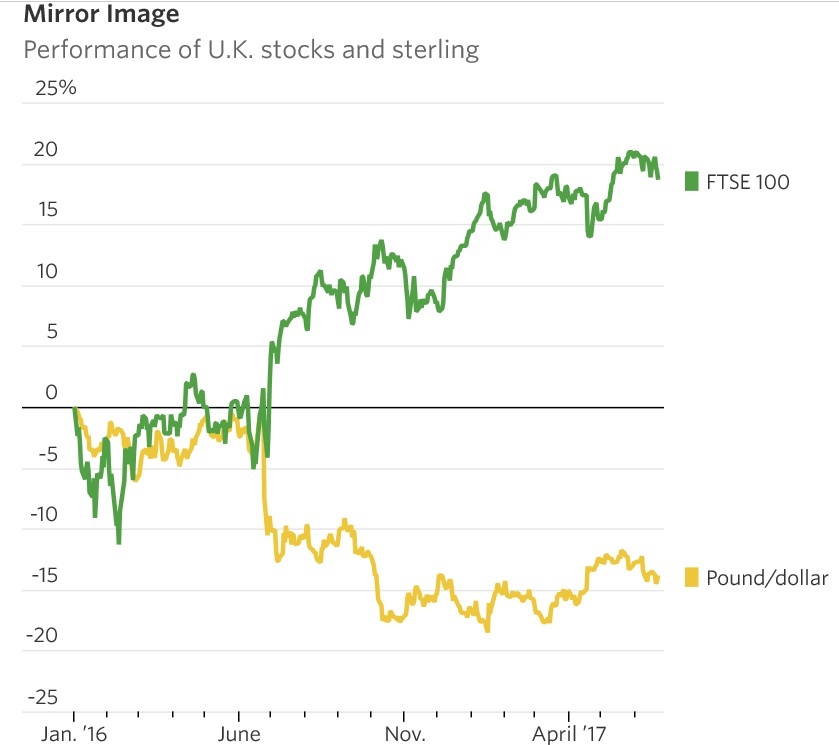

It's the one-year anniversary of the Brexit referendum tomorrow. The WSJ has a dandy chart showing the inverse relationship of the pound and the FTSE 100.

But commentary on the pound in the WSJ and elsewhere is muddy. Maybe sterling has already deval-ued as much as it needs to. Or maybe not. Nobody knows. The Brexit talks are starting out okay. PM May offered a special "accepted" status for Europeans who have lived in the UK for at least five years. We'd say that was pretty good but it got only a tepid reception.

A Bloomberg survey of Brexit experts comes up with a mixed bag of forecasts for condition in March 2019, when Brexit is scheduled to be done. Something called the German Council on Foreign Relations gives a 50% probability that talks collapse. Others put collapse at 30%. "Carsten Nickel of Teneo Intel-ligence even imagines a world where Prime Minister Boris Johnson is plotting to keep the U.K. inside the bloc. Separately, JPMorgan's Malcolm Barr told clients yesterday there is a greater than 50 percent chance that the March 2019 deadline is extended to the end of that year."

We agree with the JP Morgan guy. One thing we know about the British—if they can muddle it up, they will, and usually for the darnedest reasons that nobody off the island can foresee. It's Murphy's Law—if anything can go wrong, it will.

Churchill said the Americans end up doing the right thing after trying everything else first, but that was gratuitous bitchiness. The Brits do exactly the same thing and more often than in the US, end up with egg on their face. The end of colonialism, for example, was very badly handled indeed. Another one—Britain leaving the ERM at a $1 billion profit for Mr. Soros.

And one small note: after 70 years of tamping down nationalism, Europe is not open-minded about the concept of "sovereignty." It might as well be re-named "selfishness." Talks can stumble on this single word. The problem is that we can't necessarily deduce a sterling forecast from the ups and downs of the Brexit talks.

Politics: Trump admitted he had no Comey tapes, 41 days after suggesting he did. If Trump had not tweeted about possible tapes, Comey would not have given his friend the notes on his meetings with Trump. Comey's motivation was to get a special counsel appointed to determine that he, Comey, was not the liar. Comey laid out this line of events directly in his televised testimony to a Congressional committee. In other words, Trump could have avoided a special counsel looking into obstruction of justice if only he could have restrained himself from lying about possibly having tapes.

Trump lies even when it's against his own best interests. That makes him a "pathological" liar. As not-ed before, the Trump base is willing and able to ignore lies, and even to believe they are not lies but rather "alternative facts." This is very sad but nobody should be surprised that about 35% of the popu-lation is unread, stupid or gullible. It's not even the tail of the distribution curve of brains and judgment among the public. That is to say, Americans are not more stupid and gullible than, say, the French. They are just more stupid and gullible this year.

Trump made twelve lies just in a campaign speech in Iowa on Wednesday, according to fact checking by the NYT. One of the whoopers is about to hit, too—that Trump won't touch Medicare or Medicaid. We don't get the Congressional Budget Office cost/benefit analysis until Monday, but analysts already suspect that some 20 million persons will lose medical coverage for a saving of some $800 billion (to be used, of course, for a tax cut for the rich). Protests by people in wheelchairs are already erupting.

The core issue is not taking government benefits from the poor to give to the rich, as one might suspect. It's that the poor think they have a social contract with the government to take care of them when in dire need. The Dems mostly accept the social contract concept and the Plubs mostly reject it. The dire need arises because of the incompetence and greed of the medical industry, including Big Pharma. Big Pharma the very embodiment of the swamp Trump promised to drain. $90 for a teaspoon of eye drops is nothing but pure greed.

The core issue is not taking government benefits from the poor to give to the rich, as one might suspect. It’s that the poor think they have a social contract with the government to take care of them when in dire need. The Dems mostly accept the social contract concept and the Plubs mostly reject it. The dire need arises because of the incompetence and greed of the medical industry, including Big Pharma. Big Pharma the very embodiment of the swamp Trump promised to drain. $90 for a teaspoon of eye drops is nothing but pure greed. The public is literally crying out for relief from unconscionable medical charges, just as it cried out for the government to step in and regulate unsanitary food production and unsafe workplaces. Obama side-stepped the issue. It's one of his biggest failings. The insurance model should have worked, in theory, but could never work without outright price controls of some sort, even controls disguised as bargain-ing for discounts. But price control is a dirty phrase. Capitalism is supposed to be free—free to hose the consumer.

Trump was born rich. He has no idea what Medicaid really means to the ordinary person. But breaking his promise to keep Medicaid is one lie that is going to come back to haunt him, possibly in the 2018 mid-term elections.

Note to Readers: RTS has launched a Trade Copier service. We place our trades from the Afternoon Traders' Advisory in the retail spot market and your MT4 account mirrors the trades taken in the RTS account. You don't have to lift a finger. You get to pick how much leverage and exactly which curren-cies you want to include. If you are interested, please contact Paul Harris at [email protected] or visit http://www.rtsforex.com/trade-copier/.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.22 | LONG USD | 06/21/17 | STRONG | 111.09 | 0.12% |

| GBP/USD | 1.2720 | SHORT GBP | 06/12/17 | STRONG | 1.2701 | -0.15% |

| EUR/USD | 1.1169 | SHORT EURO | 06/12/17 | WEAK | 1.1218 | 0.44% |

| EUR/JPY | 124.22 | SHORT EURO | 07/08/17 | WEAK | 123.65 | -0.46% |

| EUR/GBP | 0.8780 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 3.42% |

| USD/CHF | 0.9716 | LONG USD | 06/12/17 | WEAK | 0.9675 | 0.42% |

| USD/CAD | 1.3228 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 2.89% |

| NZD/USD | 0.7280 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 3.09% |

| AUD/USD | 0.7564 | LONG AUD | 06/08/17 | STRONG | 0.7548 | 0.21% |

| AUD/JPY | 84.14 | LONG AUD | 06/16/17 | WEAK | 84.65 | -0.60% |

| USD/MXN | 18.0708 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 3.42% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat