Big picture: Patience is a virtue

In this week's Big Picture series we discuss key market signals and preview the upcoming week's ECB decision.

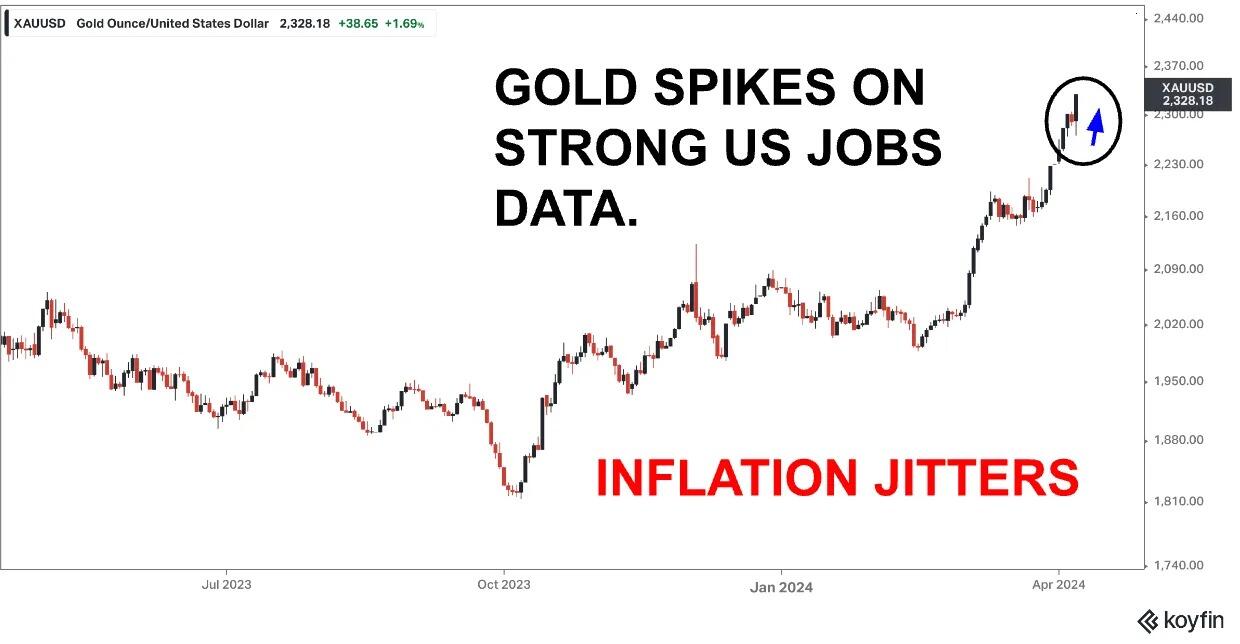

Price action in commodity and fixed Income markets this past week continue to signal the need for higher rates despite central banks desire to ease monetary policy. Global manufacturing PMI’s are rising again, business sentiment is improving, and US labor markets remain robust. Easing financial conditions and forward guidance by central banks on rate policy is providing a powerful boost to underlying economic conditions at a time when short term inflationary pressures are again rising. While central banks are keen to at least begin the process of normalizing policy, we think for now patience is warranted.

-638481080868404825.jpg)

Central banks

Core inflation rates both in North America and Europe hover near or just above 3% while Headline inflation rates have declined more drastically. The decline in headline rates has been good news but is unlikely to continue.

Energy markets have rallied aggressively and will now begin to meaningfully exert upward pressure on main CPI indexes in the coming months. Europe, in particular, could be susceptible.

Headline inflation in Europe has experienced a sharp deceleration recently due to favourable base effects in energy. This is unlikely to continue as past base effects wane and recent upward movements in the price of Oil start to show up in the numbers. We worry that the ECB’s current policy of messaging to markets a desire to cut rates this summer is in fact boxing themselves in. It’s likely that their inflation forecasts for this year at 2.3% are now too low given underlying trends. Having to revise inflation forecasts up while still promising near term rate cuts would be awkward indeed and perhaps imprudent from an inflation risk management perspective. Let us see what they have to say at this week’s upcoming monetary policy decision.

The Bank of Canada, which is also set to meet this upcoming week, has been forceful in maintaining a more neutral tone relative to other central banks as domestic inflationary pressures have remained. They will continue to watch global inflationary dynamics and be more wary in signalling rate cuts this week as some recent activity data has also come in stronger. It was interesting to note that even Chairman Powell of the Federal Reserve has also started to signal a level of caution on rate policy in between meetings as was evident in his speech made to markets last week.

For now, patience is indeed a virtue.

-638481081143123612.jpg)

Week ahead

We have an important week ahead of us on the Global Macro calendar as both the Bank Of Canada and the European Central Bank are set to meet and discuss monetary policy. China and the US are due to release their individual CPI reports for the month of March with China additionally providing markets with their latest data on export activity, money supply conditions and underlying lending activity.

The market will be keen to see ongoing evidence that Chinese stimulus efforts are working to support key activity indicators as they have been judging by recent economic releases.

It will be an interesting week for sure.

Author

Mohammad H. Ali, CFA

Independent Analyst

A former Global Head of Currency Trading at TD Bank with over 20 years of institutional trading experience in FX and Fixed Income Markets.