Bank of America wins Q3 pair-off vs. Wells

BofA gazumps Wells in mortgages

Wells Fargo, still wrestling with fallout from a fake accounts scandal saw a much older conduct issue come back to bite in the third quarter leaving it with the most disappointing results among rivals so far. Shares in the world’s second largest bank by market value were also dragged by the fourth consecutive quarterly slump in its dominant mortgage business. Wells’ earnings contrasted markedly with close rival in residential property, Bank of America, where profits rose 15%. BofA posted an increasingly successful cost-control campaign, and a loan book that increased 6% hand in hand with toughening margins. How the pair fared corroborates our view that theoretically improving U.S. banking conditions won’t lift all boats immediately, particularly as the third quarter is turning more variable than investors anticipated.

Priced to sell

Wells’ shares look to be amongst the most at risk of a ‘flight to quality’ among the ‘Big 6’, signalled by a 4% stock dip on Friday. Wells investors were reacting to the size of previously reported $1bn legal charge which WFC said stemmed from before the financial crisis and a 37% collapse in mortgage revenue which pushed reported earnings below Wall St’s already pessimistic view. The group remains the least cash-generative among giant North American lenders; its trend of operating cash flow is the better part of 50% worse than five years ago. At the same time, Wells is not priced for the kind of reversal it has just reported. At 1.48 times total equity, its tangible book value projected for next year pokes above the pack, including JPMorgan, even as ratings ease across the sector. Wells Fargo is expensive.

Wells earnings quality slips

Generally speaking, where BofA was firm in the quarter, its East Coast rival produced an unsatisfactory showing. Its quarter demonstrates that it is fast catching up to hit 10% return on equity—the rule of thumb rate which investors generally expect to divide profitable and unprofitable integrated banks. By contrast, Wells’ 9.06% outcome in Q3 is sharply lower than a trailing 12-month rate of 11.5%, indicating material deterioration in the quarter. Elsewhere, BofA’s consumer lending was up 8% against the 2.6% drop in community banking at WFC. BofA’s lower than forecast bad debt provisions also outperformed the group whilst at Wells, loan loss provisions were sharply up on the quarter and barely flat on the year. We see more risk that WFC’s bad debt provisions will blow out as U.S. credit quality softens than at any of its peers.

Pair-off

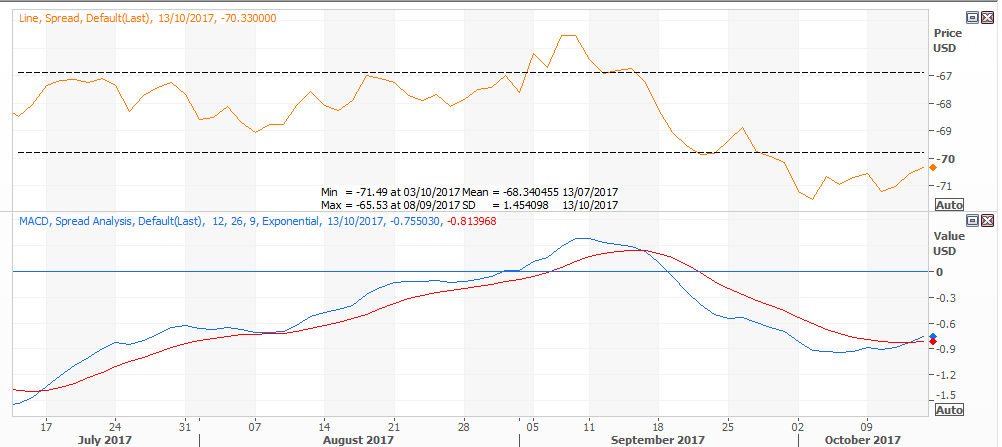

With shares of the largest U.S. lenders looking set to diverge further we expect yield hungry investors to seek out optimal pairs. A model of the most obvious two after Friday’s spate of results—long Bank of America and short Wells Fargo—has positive three-month cash flows of $2,775 on notional 100-share positions in each. However it is a BAC/JPM spread that we expect to prove most tempting to hedging investors. The pair is also in the black over the same time frame and conditions above. But in this case the spread is reverting back into its three-month standard deviation soon after a bullish crossover of its moving average convergence divergence.

Figure 1 - daily chart: Bank of America/JPMorgan Spread (3 months)

Author

Ken Odeluga

CityIndex

Ken Odeluga has over 15 years' experience of reporting and analysing global financial markets.