AUD/USD Forecast 2018: Slow bleeding set to continue for the Aussie as RBA and Fed diverge

As 2017 comes to an end, it is fair to say that AUD/USD traders have been left out with a sour taste for yet another year, as the volatility in the currency vs its US peer remains far from what it once was.

The abandonment of volatility is nothing new though, with the torturous and well familiar 10c. range between 0.70 and 0.80 extending for a third year, reflective of the lack of monetary policy action by the Reserve Bank of Australia.

Are the prospects of the AUD/USD likely to change heading into 2018?

Our opinion, as tough as it sounds, is that the low-volatility status quo is unlikely to be altered significantly in 2018. This is based on the assumption that the RBA will remain overly cautious, while the Fed will refrain from delivering an overly aggressive rate hike cycle during the 2018 campaign. Ultimately, a slow and gradual bleed lower towards 0.70 is the scenario we judge with the most risk on a 12-month horizon.

The RBA should remain neutral

To get a sense of the type of volatility the Australian Dollar may be exposed to, it is critical to understand where does the Reserve Bank of Australia stand on the prospects of shifting from its neutral position on interest rates. Throughout 2017, the RBA has left the cash rate on hold, with the last rate cut dating back to Aug 2nd, 2016.

The stance by the central bank has been that the current settings remain appropriate. At this stage, arguments can be made on both camps, with hawks finding justification on the improving outlook for non-mining investment and a strong labor market, while the more doves can remain concerned about risks to household consumption on weaker income growth and elevated debt levels.

On one hand, the RBA is concerned that lower incomes are being outpaced by household debt, which has an impact on lower inflation expectations; this also has a direct effect on consumer spending. On the other hand, the labor conditions and investment intentions continue to pick up. The RBA has enough reasons to justify no significant changes in monetary policy considerations. Such stance is unlikely to be altered in a -month horizon at the bare minimum, which should result in depressed expectations in RBA cash rate changes.

The Fed has more leeway to move on rates

The Fed has raised rates by 3 times this year, the last one taking place in December to currently stand at 1.5%, reaching the same level as the RBA ironically enough. However, what's important to highlight is that the Fed managed for the first time in more than a decade to accelerate the pace of rate increases from 1x in 2015 and 2016, to 3x in 2017, reflecting the pick up in economic momentum; and again, just as in the case of the Australian economy, the main motor of economic growth has been the labour market.

As a result of higher expectations for economic growth, the FOMC raised its projections above trend from 2.1% to 2.5%, a move that only solidifies the positive outlook heading into 2018. Unlike in Australia, a larger majority of growth in the US is achieved via the consumers. One can then throw into the mix the potential stream of business investments into the country on a friendlier tax system, which may see the risk of policy divergence between the RBA and the Fed increase. However, on this front, there remain major question marks over the prospects of businesses conducting excessive shares buy-backs vs actual tangible investments in plants/machinery/etc.

Looking at the downside risks for the US, wage growth remains a headache for policy-makers, not evolving as expected; on top of that, the yield curve in the US is not communicating such policy divergence between both Central Bank to substantially expand in a mid to long-term horizon. In the short term, the yield spread between the Australian and the US 10y bond yield sees risks skewed towards the downside though, as the rate stands at multi-year lows of 0.139%. Amid this backdrop, a 2-3 Fed rate hike may potentially be on the cards.

What does this mean for the AUD/USD?

To sum up, the risk for the policy divergence between the RBA and the Fed is set to continue, but at such a slow and gradual pace that is unlikely to result on an overly volatile impact in the exchange rate but rather we see it as a slow bleeding. The Australian Dollar is not expected to find enough keen buyers from a macro perspective that can justify much higher levels from the current rate of 76-77c. Unlike the Aussie, the US Dollar remains backed up by a cautiously hawkish Fed, hence providing incentives for the market to stay more committed towards long-side bets in the US Dollar, potentially appreciating towards 0.70c. Alternatively, should the Fed fail to deliver on at least 2 rate hike during 2018, the AUD/USD risks being stuck around the 0.75, which would probably act as a magnet given the midpoint of its wide 0.70-0.80 range is substantial. If we were to combine such scenario with a more constructive RBA heading into H2 2018, it'd be then logical to upgrade expectations towards the 0.80 handle.

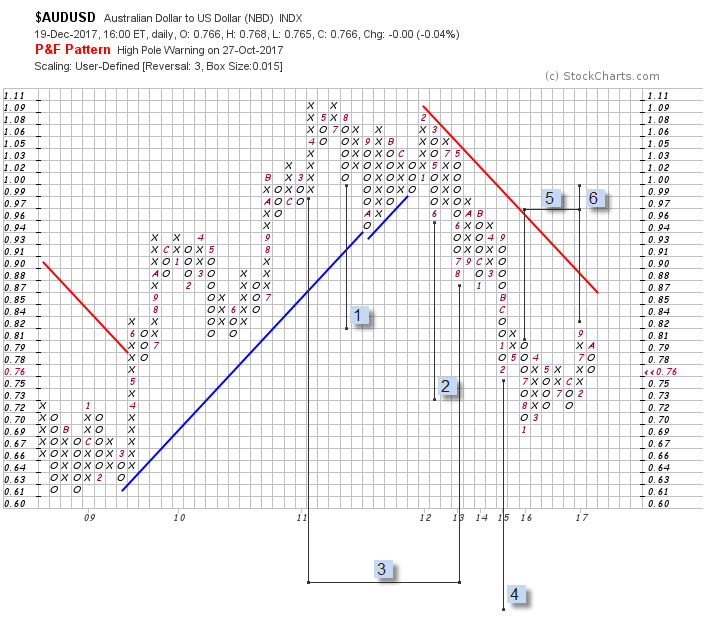

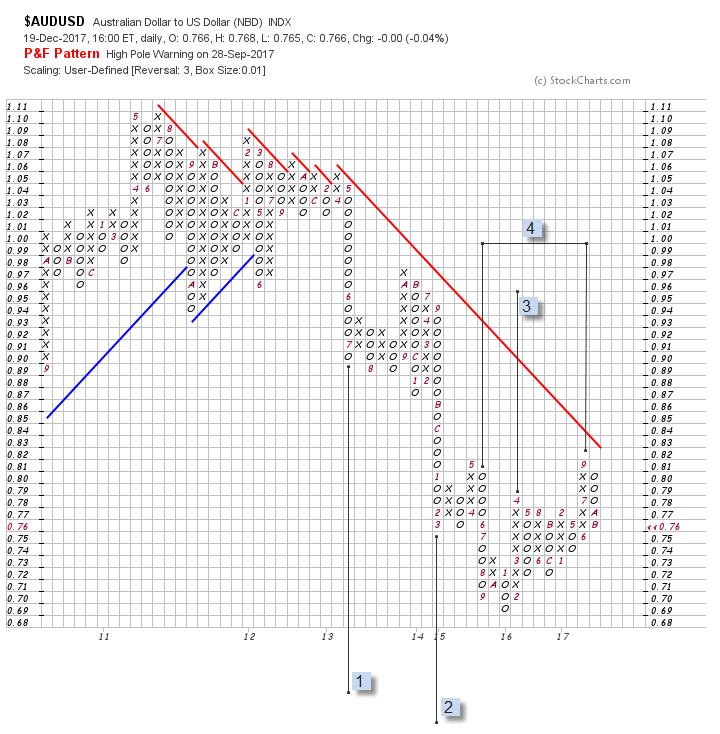

AUD/USD Point & Figure Chart

The distance to the descending 45º degree line (red) keeps the downside view as predominant in the AUD/USD, with lower projections at 0.4600, 0.4000 and fulfilled counts 1 and 2 reinforcing the bearish view.

The base building since 2015 allows price objectives at 0.9600 and 0.9900 using a combination of vertical and horizontal counts.

The case for additional upward progress is enhanced by a 100-pip box size chart, taking the same congestion pattern which has formed in recent years. This pair would appear poised of higher counts and capable of a test of 0.9500 and parity only if the red 45º line is broken. This achievement would invalidate the current downside targets 0.6000 and 0.3800 which will be the next technical targets should USD strength persist.

Author

Ivan Delgado

Independent Analyst

Established in the Asian continent since 2009, Ivan studied a degree in Business at the University Pompeu Fabra (Barcelona), while also earning a postgraduate degree in Business Administration.