Fed’s dot plot likely to go through a downgrade - ING

"Good times are hard to come by and that's why we expect the USD's cyclical decline to continue after Wednesday's September FOMC meeting," notes Viraj Patel, Foreign Exchange Strategist at ING.

Key quotes:

"This week's FOMC event may prove to be slightly more difficult for Chair Yellen to navigate as the division with the FOMC over the appropriate near-term policy approach grows. It will be interesting to see how she manages the two emerging camps – i.e. those members looking for a continuation of the current normalisation cycle and those looking for an extended (or even permanent) pause in hikes until there is more confidence in the US inflation outlook. "

"The balance of risks suggests there is more evidence for the dovish camp within the FOMC. The short-run disruptive effects of Hurricane Harvey (and potentially Irma), North Korea-related geopolitical tensions and lacklustre US inflation dynamics mean that we are likely to see the Fed's dot plot reflect a lower conviction over the pace and extent of future policy tightening. "

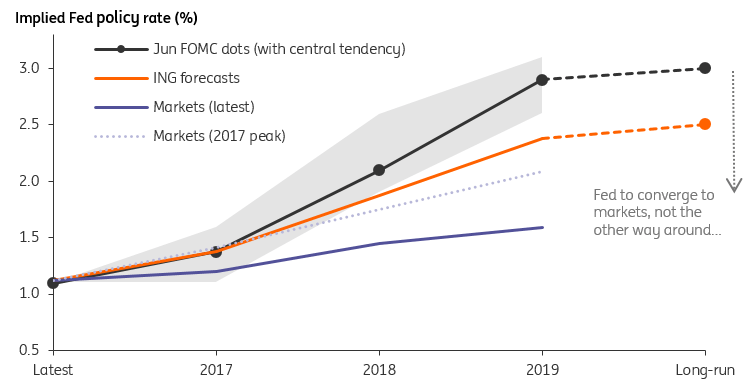

"Here are the key things to look out for when it comes to the Fed's dot plot:"

- While the median 2017 dot is still set to tentatively pencil in a December rate hike, we expect to see more members calling for a pause for the remainder of the year. Anything more than five would suggest the likelihood of additional tightening this year hangs in the balance – with markets right to price in 50:50 odds.

- More telling of a dovish shift would be if the 2018 dot also moves lower. Here we require five or more members to downgrade their views over future policy hikes – a scenario that cannot be ruled out given the softer US inflation dynamics.

- It's certainly more likely we'll see the 2019 and longer-run dots moving lower – with Fed officials acknowledging that a 2% handle on the terminal Fed funds rate is more realistic in the current economic environment.

- We'll also see the introduction of the 2020 dot this month, and we expect this to be in line with the longer-run dot, thereby putting an explicit end-date on the current Fed's hiking cycle.

Source: ING estimates, Federal Reserve, Bloomberg

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.