![]() Brandon Wendell, CMT

Brandon Wendell, CMT

Brandon Wendell

A few weeks ago I started the discussion on protecting your retirement against a market crash or even a severe correction. We discussed the use of derivatives such as options and futures to hedge a market position. In this article, I will continue diving into strategies that could be used for protecting your money in case you have it tied up in a 401k or similar retirement account and are unable to withdraw the funds in a market drop.

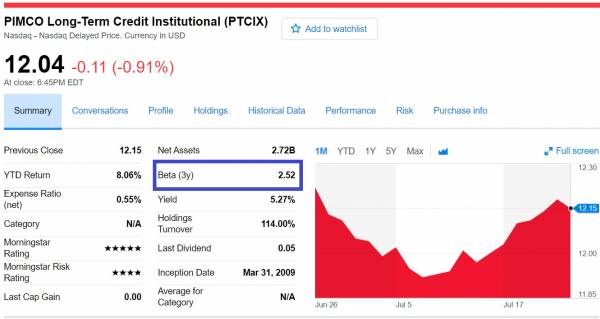

If you recall, the first thing you need to do to hedge is to determine the Beta Weighting of your portfolio. Most retirement plans consist of mutual funds and even mutual funds have a beta. This can usually be found on most financial websites.

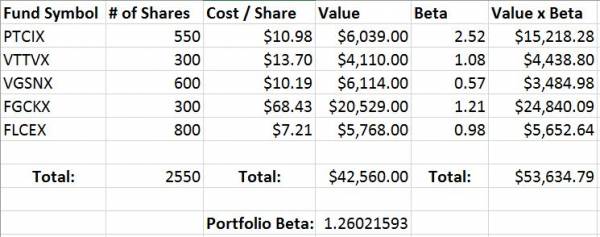

Once you have found the individual betas for each mutual fund in the account, calculate the portfolio’s total beta using the method I mentioned previously. I have selected several mutual funds from different companies to create a hypothetical portfolio below.

As you can see, this portfolio’s beta is 1.26 and consists of 2550 shares. This means that the investor needs insurance for 3213 shares (1.26 x 2550). If they were to sell S&P 500 eMini futures, six contracts would provide enough insurance for the portfolio. The problem is that the margin requirement for each contract is $4620 so the insurance would cost $32,340 to insure a $44,000 portfolio. This hardly seems efficient.

Fortunately, there are additional ways to trade the S&P futures that will offer a more cost-efficient method with similar protections. I had previously mentioned that most investors will trade options to hedge a position. Specifically, they will purchase puts on shares that they own. This works for individual stocks as they are optionable. Mutual funds do not have options available however.

Since we were planning to use the S&P 500 derivatives to hedge a portfolio, we can instead use the options on the futures. This will greatly reduce the cost of the insurance for our portfolio but still provide the same coverage.

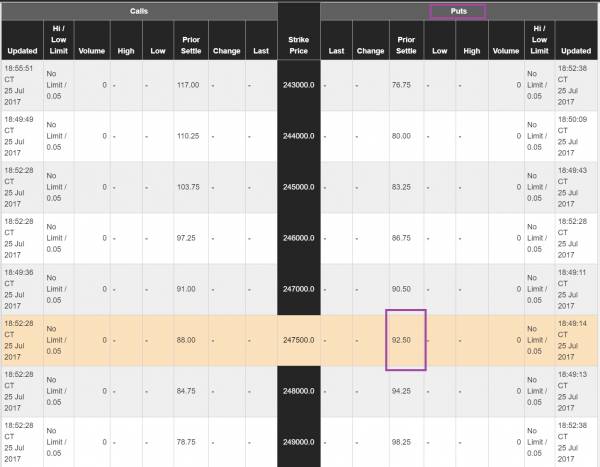

Looking at the S&P 500 eMini’s options, I am using the price level of 2474 for the start of the hedge. You will also notice that I am using the March 2018 contract and options instead of the current September one. This is done for two reasons. First, you want to insure yourself for enough time and you must also be aware of the time decay of options. If you do not buy enough time, you will lose premium and may be forced to roll over your position which results in additional commissions.

This example would insure this portfolio from now until early 2018! Buying the puts would cost approximately $4625 for each S&P 500 eMini put option we want. Wait, isn’t this the same price as selling the futures? Yes it is, but if you are better versed in options trading and are able to determine both supply and demand levels with a high degree of accuracy, you can create a bear put spread position and greatly reduce the cost of the insurance.

This hedge can be still less expensive than buying individual puts on stock, shorting the SPY, selling the ES (S&P 500 eMini), or simply holding on. As you can see there are several additional factors that you must be aware of. You need to know a little about options as you may want to buy a different put option due to pricing. You can also look to do the hedge in a retirement account such as an IRA so that there are different tax ramifications.

Even more important is knowing when to put on the hedge and when to remove it. You will need to know Online Trading Academy’s core strategy of market timing to learn when your portfolio is vulnerable and when to remove the hedge to let your portfolio grow. In our ProActive Investor course you can even learn Dynamic Portfolio Management and other strategies that can increase your chances of retiring how and when you want to. Come see what we can do to help you move out of the fear zone and achieve your goals as an investor.

Neither Freedom Management Partners nor any of its personnel are registered broker-dealers or investment advisers. I will mention that I consider certain securities or positions to be good candidates for the types of strategies we are discussing or illustrating. Because I consider the securities or positions appropriate to the discussion or for illustration purposes does not mean that I am telling you to trade the strategies or securities. Keep in mind that we are not providing you with recommendations or personalized advice about your trading activities. The information we are providing is not tailored to any individual. Any mention of a particular security is not a recommendation to buy, sell, or hold that or any other security or a suggestion that it is suitable for any specific person. Keep in mind that all trading involves a risk of loss, and this will always be the situation, regardless of whether we are discussing strategies that are intended to limit risk. Also, Freedom Management Partners’ personnel are not subject to trading restrictions. I and others at Freedom Management Partners could have a position in a security or initiate a position in a security at any time.

Editors’ Picks

EUR/USD holds firm near 1.1850 amid USD weakness

EUR/USD remains strongly bid around 1.1850 in European trading on Monday. The USD/JPY slide-led broad US Dollar weakness helps the pair build on Friday's recovery ahead of the Eurozone Sentix Investor Confidence data for February.

GBP/USD hovers near 1.3600 as UK government crisis weighs on Pound Sterling

GBP/USD moves sideways after registering modest gains in the previous session, trading around 1.3610 during the European hours on Monday. The pair could come under pressure as the Pound Sterling may weaken amid a fresh government crisis in the United Kingdom.

USD/JPY keeps the red below 157.00 on intervention risks

The Japanese Yen sticks to its modest intraday recovery gains against a broadly weaker US Dollar on the back of speculations that authorities will step in to stem weakness in the domestic currency. In fact, Japanese officials stepped up intervention warnings and confirmed close coordination with the US against disorderly FX moves. This, in turn, triggered an intraday USD/JPY turnaround from the 157.65 region, or a two-week top, touched in reaction to Prime Minister Sanae Takaichi's landslide win in Sunday's election.

Editors’ Picks

EUR/USD holds firm near 1.1850 amid USD weakness

EUR/USD remains strongly bid around 1.1850 in European trading on Monday. The USD/JPY slide-led broad US Dollar weakness helps the pair build on Friday's recovery ahead of the Eurozone Sentix Investor Confidence data for February.

USD/JPY keeps the red below 157.00 on intervention risks

The Japanese Yen sticks to its modest intraday recovery gains against a broadly weaker US Dollar on the back of speculations that authorities will step in to stem weakness in the domestic currency. In fact, Japanese officials stepped up intervention warnings and confirmed close coordination with the US against disorderly FX moves. This, in turn, triggered an intraday USD/JPY turnaround from the 157.65 region, or a two-week top, touched in reaction to Prime Minister Sanae Takaichi's landslide win in Sunday's election.

Gold remains supported by China's buying and USD weakness as traders eye US data

Gold struggles to capitalize on its intraday move up and remains below the $5,100 mark heading into the European session amid mixed cues. Data released over the weekend showed that the People's Bank of China extended its buying spree for a 15th month in January. Moreover, dovish US Fed expectations and concerns about the central bank's independence drag the US Dollar lower for the second straight day, providing an additional boost to the non-yielding yellow metal.

Cardano steadies as whale selling caps recovery

Cardano (ADA) steadies at $0.27 at the time of writing on Monday after slipping more than 5% in the previous week. On-chain data indicate a bearish trend, with certain whales offloading ADA. However, the technical outlook suggests bearish momentum is weakening, raising the possibility of a short-term relief rebound if buying interest picks up.

Japanese PM Takaichi nabs unprecedented victory – US data eyed this week

I do not think I would be exaggerating to say that Japanese Prime Minister Sanae Takaichi’s snap general election gamble paid off over the weekend – and then some. This secured the Liberal Democratic Party (LDP) an unprecedented mandate just three months into her tenure.

RECOMMENDED LESSONS

Making money in forex is easy if you know how the bankers trade!

I’m often mystified in my educational forex articles why so many traders struggle to make consistent money out of forex trading. The answer has more to do with what they don’t know than what they do know. After working in investment banks for 20 years many of which were as a Chief trader its second knowledge how to extract cash out of the market.

5 Forex News Events You Need To Know

In the fast moving world of currency markets where huge moves can seemingly come from nowhere, it is extremely important for new traders to learn about the various economic indicators and forex news events and releases that shape the markets. Indeed, quickly getting a handle on which data to look out for, what it means, and how to trade it can see new traders quickly become far more profitable and sets up the road to long term success.

Top 10 Chart Patterns Every Trader Should Know

Chart patterns are one of the most effective trading tools for a trader. They are pure price-action, and form on the basis of underlying buying and selling pressure. Chart patterns have a proven track-record, and traders use them to identify continuation or reversal signals, to open positions and identify price targets.

7 Ways to Avoid Forex Scams

The forex industry is recently seeing more and more scams. Here are 7 ways to avoid losing your money in such scams: Forex scams are becoming frequent. Michael Greenberg reports on luxurious expenses, including a submarine bought from the money taken from forex traders. Here’s another report of a forex fraud. So, how can we avoid falling in such forex scams?

What Are the 10 Fatal Mistakes Traders Make

Trading is exciting. Trading is hard. Trading is extremely hard. Some say that it takes more than 10,000 hours to master. Others believe that trading is the way to quick riches. They might be both wrong. What is important to know that no matter how experienced you are, mistakes will be part of the trading process.

The challenge: Timing the market and trader psychology

Successful trading often comes down to timing – entering and exiting trades at the right moments. Yet timing the market is notoriously difficult, largely because human psychology can derail even the best plans. Two powerful emotions in particular – fear and greed – tend to drive trading decisions off course.