Will the Fed's interest rate pause make mortgage loans more expensive?

What if high interest rates weren't a parenthesis, but the new normal?

With many borrowers eagerly awaiting a drop in interest rates to finally take or refinance a mortgage loan, the US Federal Reserve (Fed) has just sent a clear message: there's no rush.

Despite signs of easing inflation, the central bank prefers to wait before further cutting rates. As a result, mortgage loan interest rates remain high, squeezing household purchasing power and freezing part of the housing market.

Behind this apparently technical decision from the Fed lies a very concrete reality: the cost of borrowing remains high, monthly payments are weighing more heavily on budgets, and access to housing is becoming more difficult, particularly for first-time buyers.

Against a backdrop of economic resilience, geopolitical tensions and aggressive trade policy, the Fed prefers to play it safe, even if it means prolonging the pressure on households. Here's why high interest rates could last... and what it means for mortgage loans.

A prolonged pause from the Fed

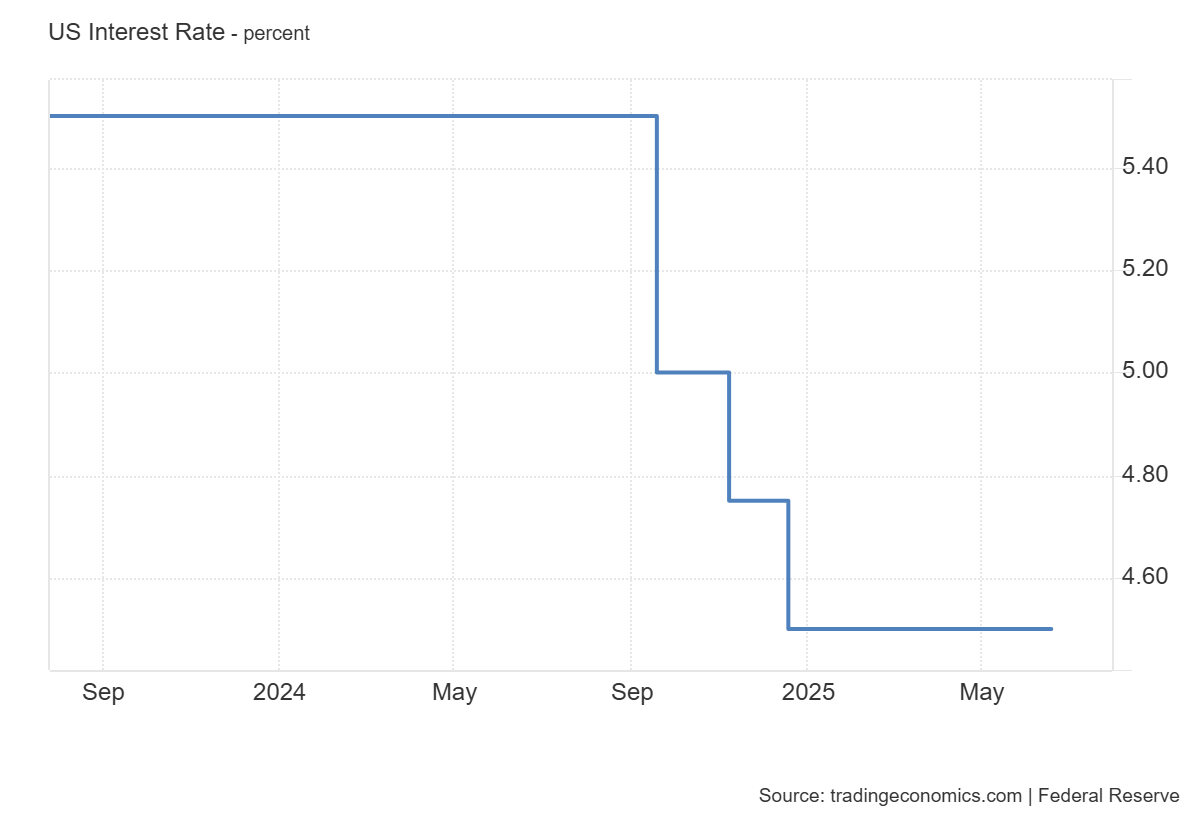

With inflation still above the 2% target set by the Federal Reserve, and US economic growth remaining resilient, the Fed decided to keep its key interest rates unchanged at its June 18 meeting.

This decision extends a sequence of status quo that began at the start of the year. The key rate thus remains fixed in a range of 4.25% to 4.50%.

At his press conference, Fed Chairman Jerome Powell struck a cautious tone, stressing that "monetary policy remains slightly restrictive" and that the institution has "the time needed to observe the evolution of the data". Despite some signs of easing on the price front, the Fed is in no hurry to revive the economy by cutting interest rates.

Especially as the political and commercial environment remains unstable, notably with the return in force of an offensive tariff policy driven by the Trump administration, is likely to fuel new inflationary tensions.

"While inflation prints and labor metrics have softened at the edges, the Fed's tone stayed composed, even borderline hawkish. Powell called the economy "solid," brushed off labor cooling as "nothing concerning," and made it clear that the bar for a Summer cut remains high", noted Stephen Innes at FXStreet.

Interest rate cuts postponed... and uncertain

The Fed is still officially considering two rate cuts between now and the end of the year. But this scenario is becoming less and less credible in light of Powell's statements and revised projections.

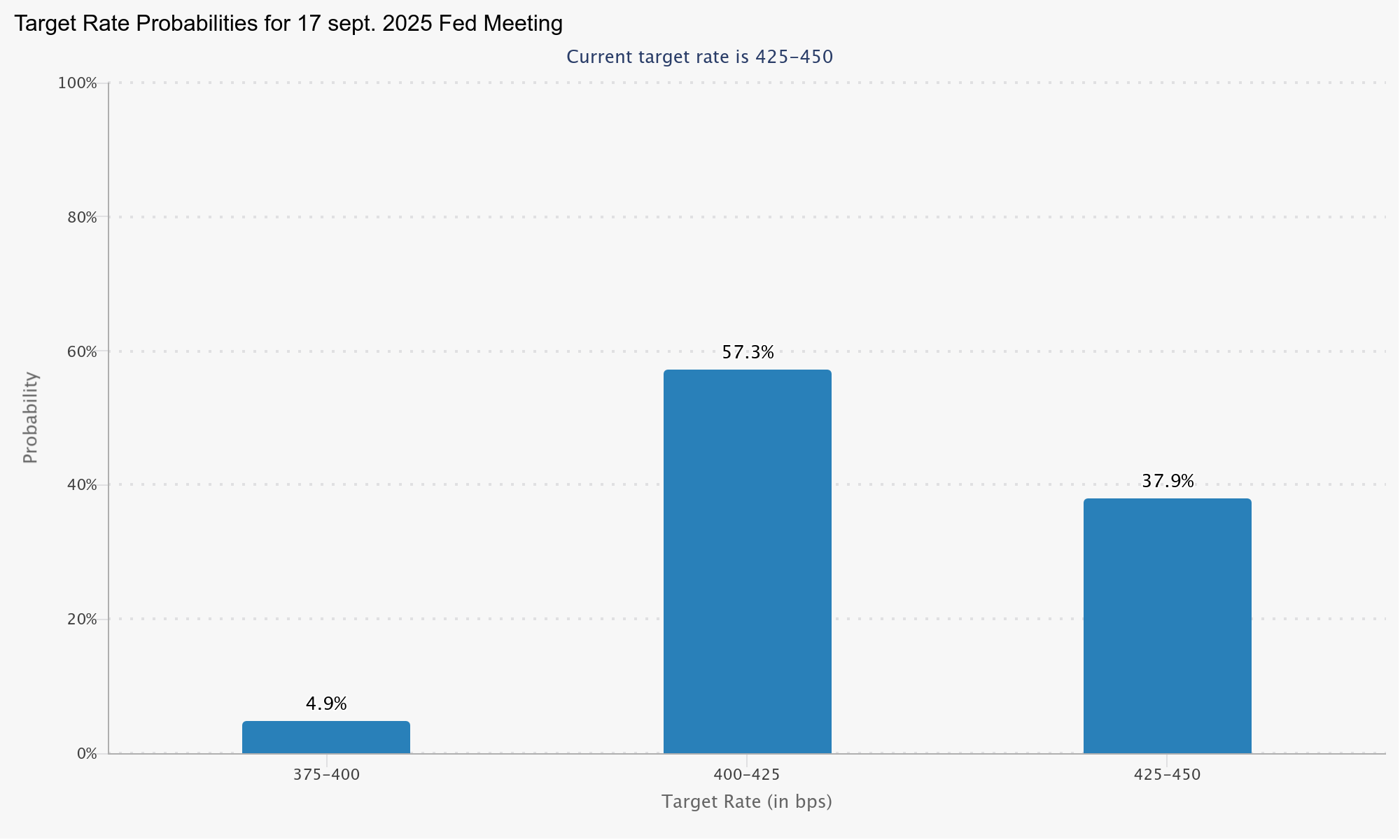

Financial markets are now cautiously anticipating an interest rate cut in September with a 57.3% probability, and then in December but with much more uncertainty, with a lower likelihood of 42.1%.

Source: CME Fedwatch Tool.

The main obstacle to rapid interest rate cuts remains the risk of new tariffs being passed on to consumer prices. Powell himself has acknowledged that the transfer of cost increases to consumers is a threat to be closely monitored.

Against this backdrop, cutting interest rates too soon could be counter-productive, jeopardizing efforts to keep inflation under control.

Sustained high real estate rates

The Fed’s wait-and-see stance has a direct impact on real estate financing conditions. Although mortgage loan rates are not mechanically indexed to key interest rates, they are closely linked to monetary policy expectations, via the bond markets.

Today, the average 30-year mortgage rate is around 6.9%, according to Mortgage News Daily, and has fluctuated little since the beginning of the year.

This high level is explained by the resistance of 10-year bond rates, which incorporate both inflationary risk and the lack of visibility on the timing of future Fed decisions.

In addition, variable-rate loans and mortgage credit lines, which are directly linked to the policy rate, frequently exceed 8%, according to Bankrate.

Since 2022, the Fed's successive interest rate hikes have mechanically increased the cost of credit. Monthly payments for the same property have soared in three years. Despite Fed rate cuts since 2024, mortgage rates have remained high.

Source: CNET

This situation is weighing heavily on demand, particularly among first-time buyers, whose borrowing capacity is more sensitive to financial conditions.

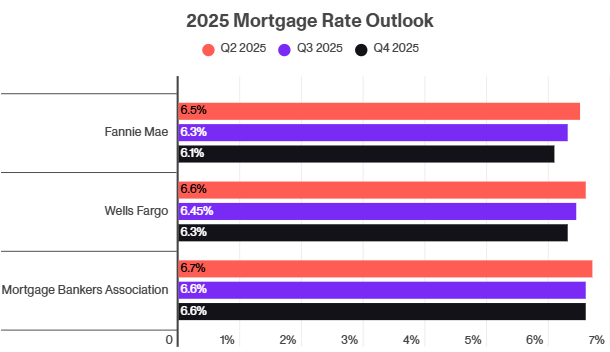

Several institutions now expect mortgage rates to remain high throughout the current year, barring a major external shock.

"Average rates are likely to stay in the 6.75% to 7.25% range unless the Fed signals multiple cuts," said Nicole Rueth from Movement Mortgage, according to CNET.

Matt Schulz, chief credit analyst at LendingTree, added: "I don't see any major changes coming in the immediate future, meaning that those shopping for a home this summer should expect rates to remain relatively high.", according to CNBC.

Weakened demand and more difficult access to credit

Maintaining such high rates has a dual effect on the property market: it discourages buying, but also slows down resales, since homeowners already committed to low-rate loans have no interest in selling to borrow on much less favorable terms.

This contributes to the shortage of available housing, which keeps prices high in many urban areas, exacerbating the problem of affordability.

For households, access to credit is becoming more selective. Loan conditions are tightening, and applications with low capitalization or unstable incomes are more likely to be turned down.

An environment of long-term constraints for borrowers

Against this backdrop, borrowers have little room for maneuver. Those contemplating a property purchase have to contend with high financing costs, limited supply and growing pressure on their debt capacity.

Opportunities for renegotiation remain limited, except for borrowers who took out mortgages at rates well above today's, which has become rare.

Caution is also called for by those planning to enter the real estate market in the months ahead. Without a clear shift in Fed policy, credit conditions are unlikely to improve significantly before 2026.

This doesn't mean that you shouldn't buy, but that you should buy in full awareness of the real cost of credit, and taking into account the possibility that rates may not come down as quickly as hoped.

An impact far beyond real estate

The Fed's decisions are not limited to housing. They are having an impact on the entire US credit market, directly affecting credit cards, car loans, lines of credit and student loans.

Variable-rate credit cards are among the most sensitive to rate hikes. The average now exceeds 20%, not far from last year's all-time record, notes Bankrate.

"Card rates are painful because they are extremely high," sums up TransUnion's Charlie Wise, quoted by CNBC. Even a two-point cut in the benchmark rate would only provide a slight reprieve, he adds.

Auto loans are also under pressure. Rates are hovering around 7.3% for new vehicles and 11% for used models, according to Edmunds data quoted by CNBC. Added to this are the inflationary effects of tariffs on imported vehicles.

"Financing a vehicle is simply becoming unaffordable for a growing number of consumers," notes Edmunds' Ivan Drury.

As for student loans, federal loans will remain relatively stable, with a slight drop to 6.39% on July 1, notes CNBC. But private loans, often at variable rates, continue to climb, exposing the least creditworthy borrowers to increasingly stringent conditions.

High interest rates: a reality that's taking hold

The latest Fed meeting confirms the maintenance of a resolutely cautious monetary policy, in an environment still marked by geopolitical uncertainty and inflationary risks.

For borrowers, and in particular for low-income households and young buyers, this means more expensive and more difficult access to credit. In the absence of any clear signs of easing, high real estate rates look set to last.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.