USD/JPY Weekly Forecast: Inflation’s differing impact in the US and Japan

- US inflation data drives Treasury yields, dollar higher.

- Fed funds futures posit three rate hikes in 2022.

- US-Japan 10-year bond yield spread widens 4 basis points.

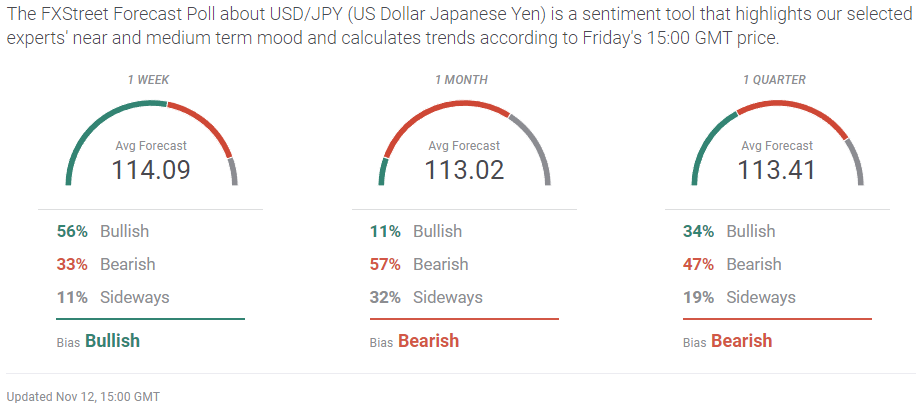

- The FXStreet Forecast Poll sees short term gains followed by weakness in the USD/JPY.

Four sessions of slow USD/JPY descent ended with a bang on Wednesday with the release of US consumer inflation figures for October at 8:30 am local time.

The predicted 0.4% increase in the annual CPI rate, from 5.4% to 5.8%, came in doubled at 0.8% and the resulting 6.2% yearly pace was the fastest in over 30 years. The monthly rate jumped to 0.9% from 0.4% in September.

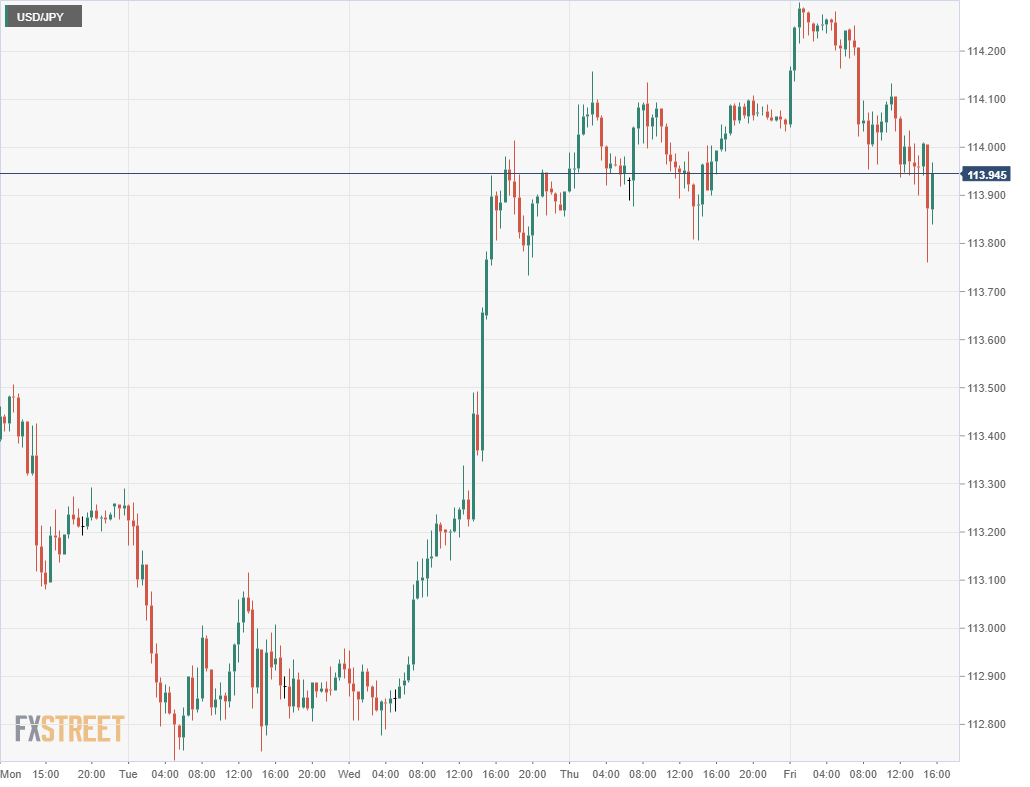

Reaction was immediate. The US dollar jumped in every major pair. The USD/JPY rose 20 points to 113.49 in the first 15 minutes, paused briefly before 113.50, then continued higher the rest of day closing in New York at 113.89, over a figure above its open.

The US currency climbed sharply against the euro finishing the day at 1.1478, its first conclusion below 1.1500 since July 27. The sterling lost a figure-and-a-half to 1.3408 and the USD/CAD soared through 1.2500 for the first time in a month closing at 1.2589.

When the Treasury market opened an hour later, yields raced higher. The 10-year added 5 basis points within minutes to 1.490% and ended up 12 points to 1.560%. The 2-year rose 10 points to finish at 0.505%, as did the 30-year 1.918%.

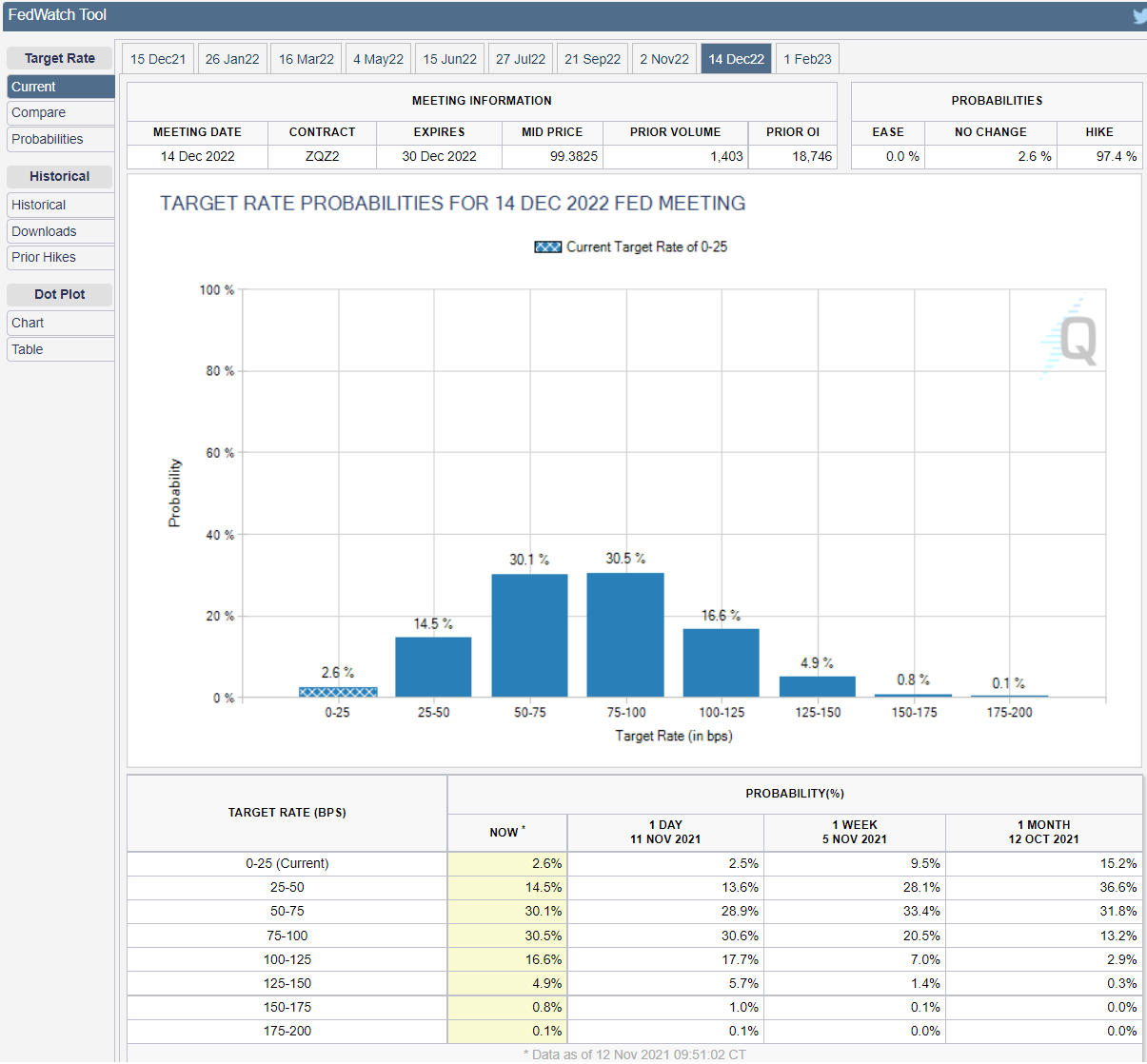

When the Federal Reserve launched its bond program taper two weeks ago with a $15 billion reduction in monthly purchases, only November and December were spoken for in the FOMC statement. Beyond that the governors said they expected the cuts to continue but the decision would turn on progress of the US economy.

Credit markets clearly view inflation at a generational high as leaving the Fed little policy choice. While the September Projection Materials envisioned just one 0.25% fed fund increase next year, the Treasury market is far more aggressive. The Chicago Board Options Exchange, (CBOE) FedWatch Tool, based on fed funds futures, predicts three increases by year end 2022.

CBOE

The Treasury market was closed on Thursday for the US Veterans Day holiday.

Inflation data will be updated on November 24 when the Bureau of Economic Analysis (BEA), a division of the Commerce Department releases its Personal Consumption Expenditure Price Index (PCE) for October. The core version of this is the Fed’s chosen measure. Due to its different statistical composition, the PCE has historically produced a lower overall inflation rate than the older CPI gauge. It is likely that PCE will show the same acceleration in consumer prices as did CPI. The September PCE readings at 4.4% for the headline measure and 3.6% for core were already the highest on record for this series.

The spread between the US 10-year Treasury yield and its Japanese Government Bond (JGB) counterpart widened 4 basis points this week. That alone is sufficient to keep the USD/JPY bid.

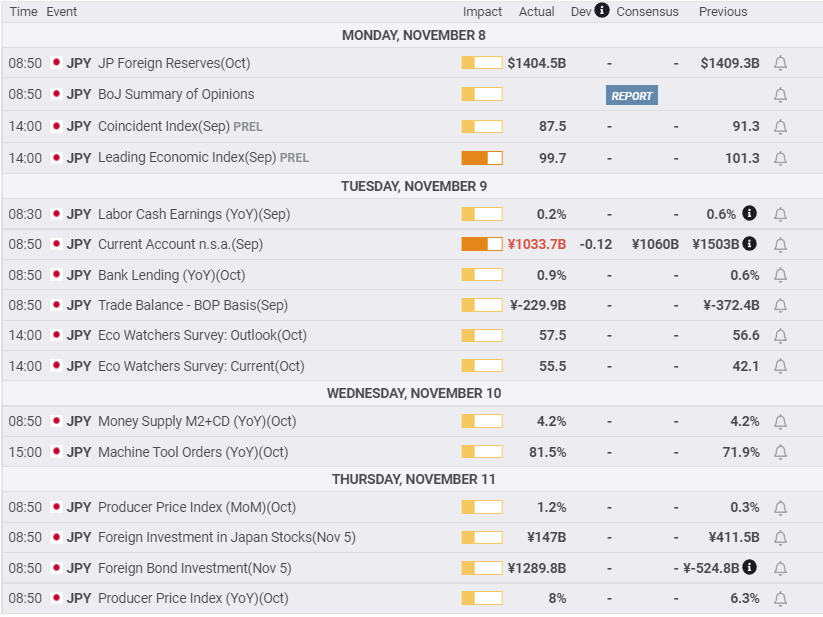

Japanese economic information improved though consumer weakness continued. Labor Cash Earnings were but 0.2% higher in September down from 0.6% in August. The Eco Watchers Survey, which tracks regional economic trends, rose for both the Outlook and Current polls. The Producer Price Index (PPI) rocketed 1.2% in October, four times its September pace, and the annual rate at 8% was up from 6.3% and the highest in over a decade.

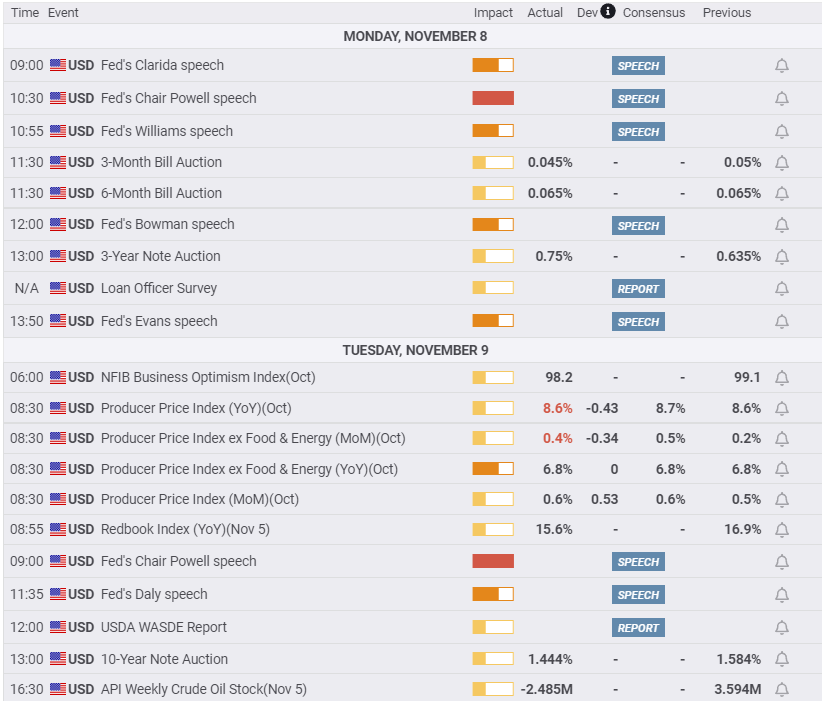

On the other side of the dateline, US inflation data on Wednesday, as above, was the market driver. Not only was CPI at a three decade record in October but PPI stayed at its own all-time heights of 8.6% and 6.8% core in October, promising more consumer price increases in the months ahead. US Consumer Price Index: Falling real wages and the Fed's credibility problem, US Producer Price Index: Gains promise higher consumer costs

Initial Jobless Claims dropped to 267,000 in the first week of November, a level not far from the success of the second half of 2019 before the pandemic.

The Job Openings and Labor Turnover Survey (JOLTS) maintained its near record number of open positions in September. It is not the US job market that is depressing consumer attitudes.

Consumer Sentiment in the Michigan Index unexpectedly dropped to 66.8 in November from 71.7. A rise to 72.4 had been forecast. As the likely cause is burgeoning inflation it adds the threat of a sharp pullback in consumer spending to the lengthening list of economic worries.

American consumer prices rose at a 10.8% annualized rate in October. Inflation has become the standard metric for Fed monetary policy and market prospects.

USD/JPY outlook

The interplay between US inflation rates and Treasury yields has been the determining factor for USD/JPY since the September Federal Reserve meeting. That relationship was strengthened this week by the dramatic increase in October’s CPI.

The surge in Japan’s PPI rate in October indicates that the supply dislocations and shortages are a global phenomenon.

Tokyo’s policy response will be very different. The Bank of Japan (BOJ) has spent a decade and more trying to fend off the deflationary impulses in an export oriented economy beset with weak domestic consumption from an aging and declining population.

Prime Minister Fumio Kishida has promised the standard fiscal spending and monetary stimulus policies and a desire for a weaker yen that have routinely failed to improve the nation’s economic prospects over three decades. The BOJ is likely to see inflation as an assist in defusing the economy’s deflationary tendencies.

The economic conditions, primarily inflation, will play out very differently in the United States and Japan. In the US, the October CPI report prompted a 10 basis point run higher in the 10-year Treasury yield. The 10-year JGB return rose less than 1 basis point. Even If Japanese inflation accelerates far beyond its current 0.2% (YoY) rate in the months ahead, the BOJ is likely to welcome the change. It will certainly not ramp up interest rates in response.

Japanese statistics next week will feature the National CPI for October. Tokyo inflation, usually seen as an indicator for the country as a whole, was issued on October 28 and at 0.1% (YoY) was down from 0.3% in September. It missed the 0.5% forecast by a wide margin. Core prices were unchanged at 0.1% (YoY) from September, also below their 0.3% prediction. There is no reason to expect any difference in the countrywide numbers.

Markets will focus on US Retail Sales for October on Tuesday. The consensus estimate is 0.7% as in September. Any weakness here, especially with the drop in November’s Consumer Sentiment, will add urgency to the Fed’s inflation fight and support US yields.

The widening interest rate profile between the Fed and the BOJ and the two economies is the overriding fundamental logic for the USD/JPY. The bias for the pair is higher.

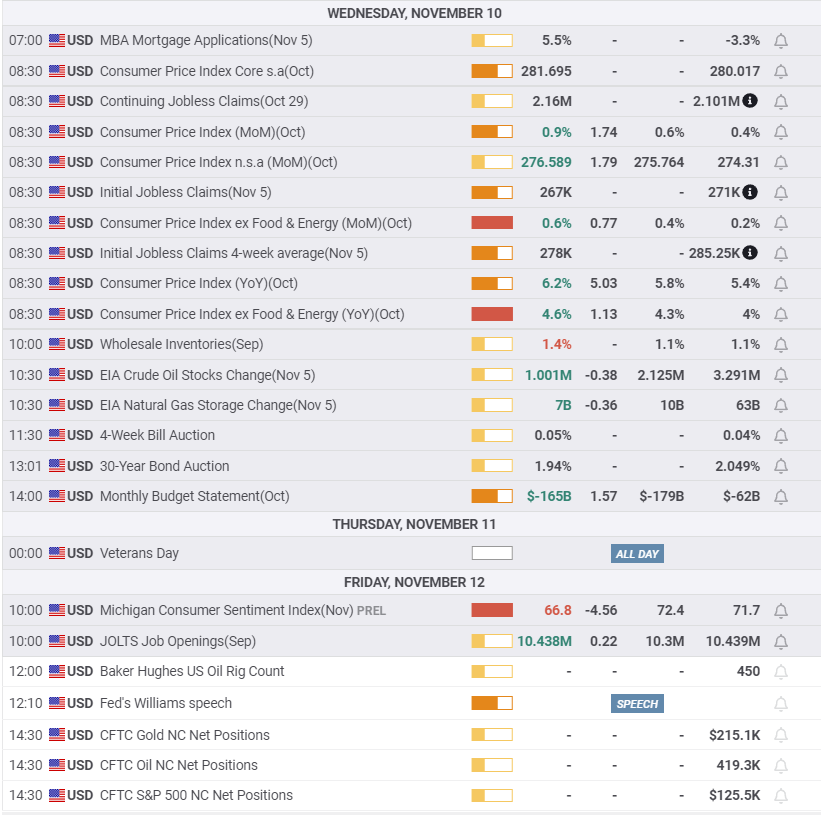

Japan statistics November 8–November 12

US statistics November 8–November 12

FXStreet

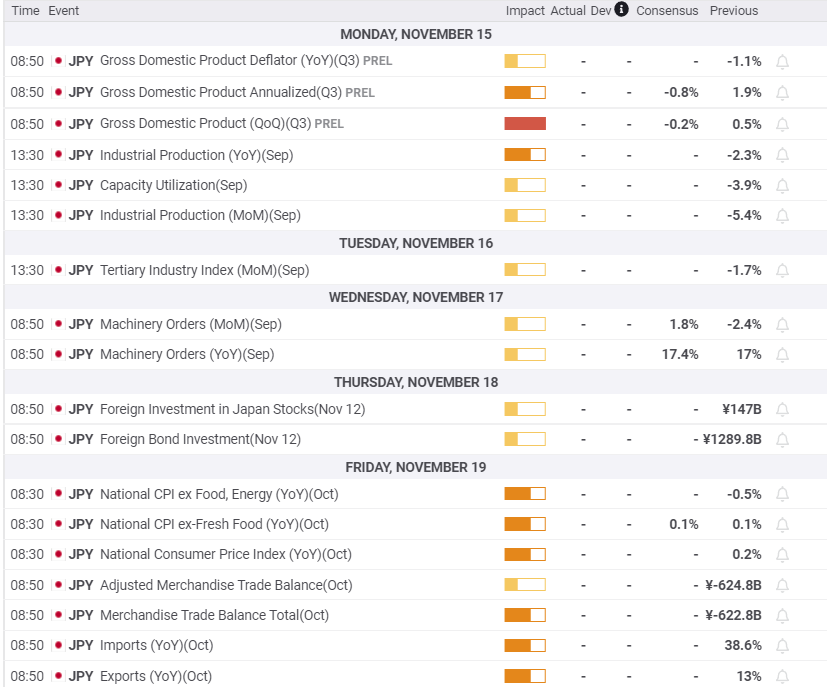

Japan statistics November 15–November 19

FXStreet

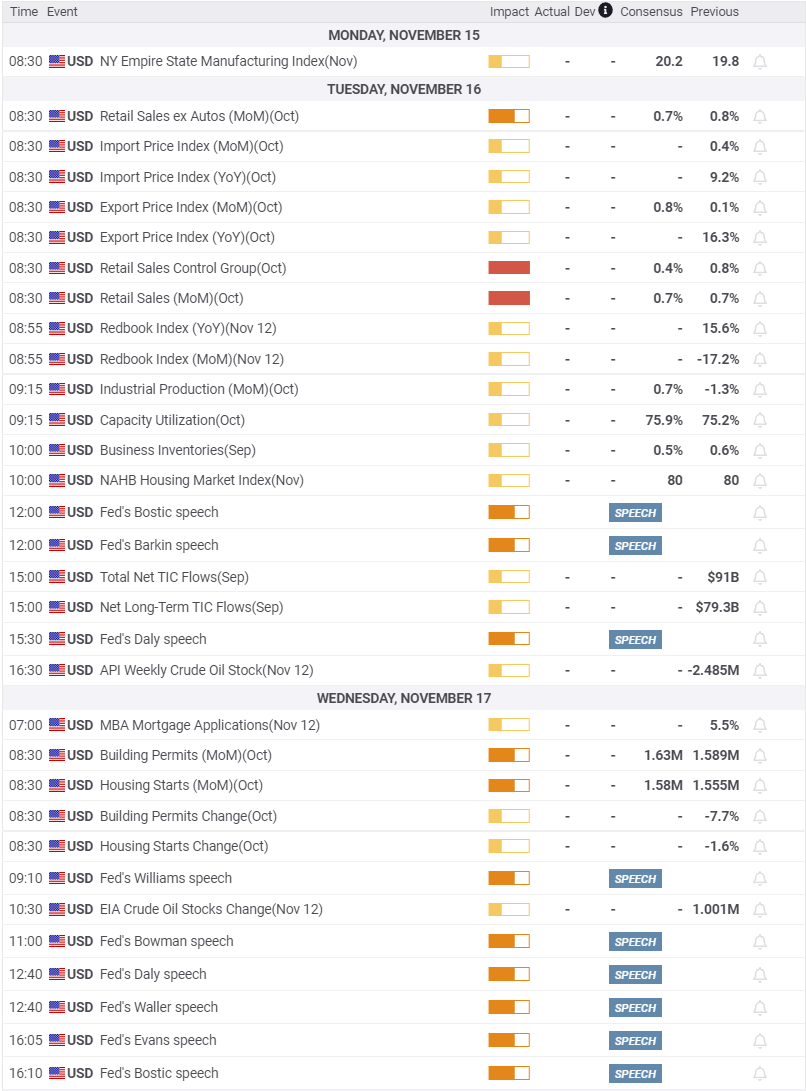

US statistics November 15–November 19

USD/JPY technical outlook: Performance questions above 114.00

Fundamental factors and technical support favor the USD/JPY but performance has been capped above 114.00. The USD/JPY had been positioned for a break higher from October 15 on. The failure to do so led to November's decline. Despite the strong boost from US Treasury rates on Wednesday, the USD/JPY was unable to penetrate above the recent highs and did not approach the three-year top of 114.70 of October 20. If the USD/JPY again fails to achieve a new high, a retracement becomes likely. The 112.25 to 113.25 range is vulnerable.

The MACD (Moving Average Convergence Divergence) line moved below the signal line on October 26. The subsequent two weeks of price action saw a drop to below 113.00 until reversed by the US Treasury yield surge on Wednesday. The MACD line has not recrossed the signal line. The divergence between the two lines decreased this week indicating a rising chance of a decline in the USD/JPY.

Wednesday's rise in the Relative Strength Index (RSI) brought it about half-way to overbought status but the fade on Thursday and Friday left it without strong indication.

The 21-day moving average (MA) at 113.80 was effective support on Thursday and Friday and is the only relevant MA. The 50-day MA at 112.15 will be a substantial backing for the support line at 112.25 should the USD/JPY penetrate lower. The 100-day MA at 111.10 and the 200-day MA at 109.87 are outside the likely scope of near term trading.

Resistance: 114.00, 114.20, 114.50

Support: 113.85 (21-day MA 113.80), 113.25, 112.85, 112.25, 112.00, 111.50

FXStreet Forecast Poll

The FXStreet Forecast Poll highlights the USD/JPY dependence on economic fundamentals for support. Without a widening yield spread for US Treasuries, technical factors will tend to pull the pair lower.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.