The Fed is the only thing that might upstage Trump

Outlook:

Markets are girding their loins for this week's data, but also for a full day of press attention to Trump's speech tomorrow night to Congress. Trump craves attention so badly he will kick off the day with TV appearances in the morning with just enough tempting crumbs to hold commentators all day in a state of speculation. At a guess, there will be promises of the best-ever tax reform, stunning deregulation, and wondrous infrastructure re-building and just enough detail ahead of time to keep the suckers talking about Trump. Congress will be more circumspect but craven—they will put up with all kinds of nonsense to get what they want.

So far we have TreasSec Mnuchin saying the new budget will not cut Social Security or Medicare, which will keep the Boomers quiet. The NYT reports the budget will cut non-defense spending like the EPA but ramp up defense spending. Today state governors visit the White House, long lists of infra-structure projects in their grubby hands. Maybe Trump wants all the attention, all the time for a full week.

Some analysts are already saying Wall Street is fed up with hyperbole from the Entertainment President and want real policy substance. We are not so sure—we don't want to underestimate the Trump need to shock. The only thing that might upstage Trump is the Fed. We have a gaggle of no fewer than eleven Fed speakers this week, leading to Yellen on Friday, and the March meeting in two weeks. Normally Fed speakers go their own way and do not coordinate their comments or need any kind of permission to say whatever they want, but it's conceivable that this time Yellen and Fischer have gently suggested a more hawkish tone.

Wall Street in Advance guru Lynn notes that March might be preferable this time because of the UK invoking Article 50 (no exact date known) and maybe the first French election in April. The Fed had to defer the hike last summer and fall in part because of the turmoil caused by Brexit in June. But May is worse. The May FOMC meeting is on May 3, between the first and second rounds of France's presi-dential election. The majority of the bond gang is sticking to June.

And we have data galore this week. Today we get durables, expected up a hefty 1.6% after -0.5% in Dec, and the NAR pending home sales, expected up 1%. Note that the job report is not coming on the first Friday this time (Mar 3) but rather the week following (Mar 10). See the calendar on the last page. We get GDP from a slew of places, including the US (tomorrow), plus manufacturing PMI's, inflation, retail sales and sentiment indicators. The calendar is just stuffed full.

All that data generates noise, but if there is a signal in there, it could be the divergence between stocks and bonds. The WSJ wrote over the weekend "The U.S. bond market is parting ways with the stock market—a red flag for investors who piled into the reflation trade. While the Dow Jones Industrial Av-erage has soared more than 1,000 points so far this year and closed at a record of 20821.76 Friday, the yield on the benchmark 10-year Treasury note fell to 2.317% Friday, the lowest since late November, from 2.446% at the end of 2016."

The divergence between equities and bond yields is generating debate. Some money managers and traders wonder whether a rising bond market is a warning that valuations of riskier assets may be stretched. The Dow closed at a record for the 11th consecutive session Friday, the longest streak since 1987." It's still a low-yield world (hence the rush into emerging markets). But managers prefer bonds, anyway. "... some big money managers say they are returning to the $13.8 trillion Treasury market, the foundation for global finance and a yardstick for valuations of riskier assets, amid increasing concern that exuberance for Mr. Trump's policy outlook may be overdone." One analyst says ""The bond mar-ket is showing a more realistic view on the fiscal policy outlook than the stock market. The bond mar-ket has it right."

And the dollar follows the bond. The WSJ says the falling dollar is another sign of worry. But no, it's really the same sign. One analyst has two scenarios: "the 10-year Treasury yield could rise to 2.75% or higher if ‘everything works out well' with fiscal policy, but the yield could fall to 2% if policy details disappoint."

Contributing to demand for Treasuries is the political situation in Europe, which drove the 2-year Ger-man Schatz to a record low (again) on Friday at -0.959%, according to Tradeweb. And the 10-year to 0.188%. It's 0.195% this morning. And "Net wagers on higher bond yields via Treasury futures were $73 billion for the week ended Feb. 21, down from a recent peak of $100.7 billion in January, accord-ing to TD Securities." This could be a set-up for a short squeeze, which has the unhappy effect of am-plifying any yield drop.

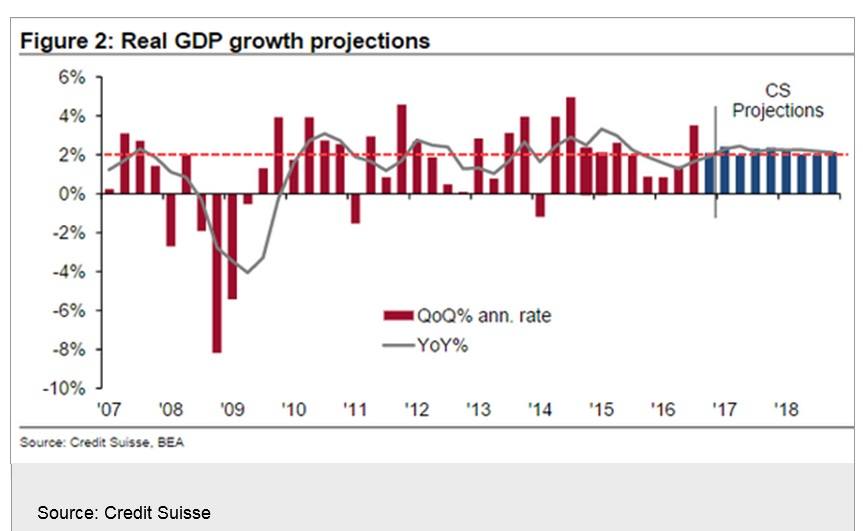

The Fed is caught between a rock and a hard place. The timing of the hike, March or Not-March, really is critical this time, given all the other events about to fall down on our heads. This would argue sooner is better. But to justify a hike, the Fed has to believe in both growth and inflation. You don't get inflation without growth, and growth is more iffy than we think. One GDP forecast, from Credit Suisse, is below (from the Daily Shot). Because of demographics, the participation rate, low capital investment, and a dozen other factors, Trumpian talk of 4% growth is simply not realistic. The Fed has its own ide-as, of course, but they also don't go anywhere close to 4%.

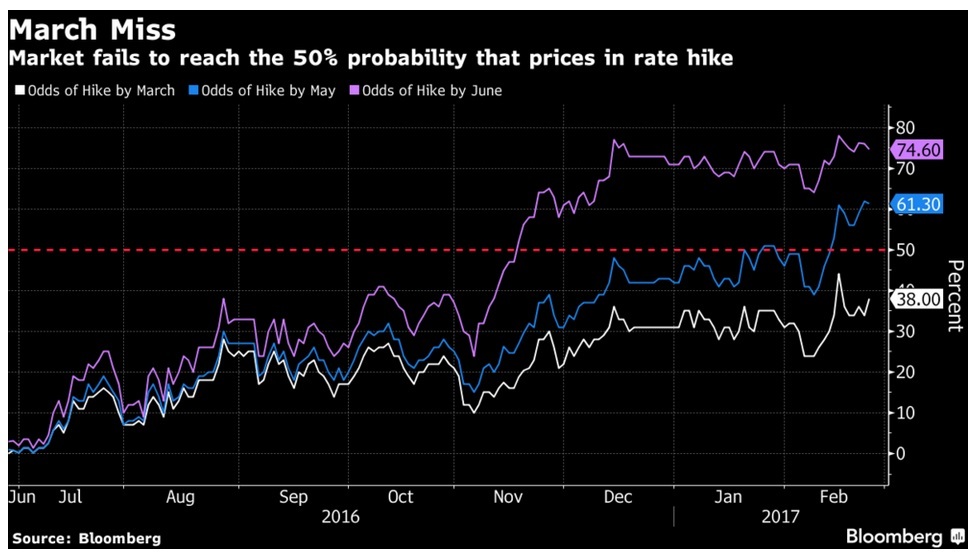

And Bloomberg notes, trying to provoke, that the Fed trying to sell March to the bond gang is not working. The market has an effective "veto" over it. The Bloomberg version of the probability of a March hike is 40% (it's lower in the CME version, 28%). Bianco Research say "Since they began an-nouncing their target for the Fed funds rate in 1994, a period encompassing 191 meetings, policy mak-ers have never surprised traders by lifting rates when they were expecting the central bank to stay put." The Fed does not like to surprise the market. But May is worse. The May FOMC meeting is on May 3, between the first and second rounds of France's presidential election. Bottom line--unless the Fed acts in March, we will probably be waiting for June. This is not dollar-favorable.

Finally, we have two "new" political effects on financial markets. The first is "reasonable expectations" of major changes in tax, regulation and fiscal spending policies. Analysts are straining to keep their attention focused on policy per se, as in TreasSec Mnuchin's comment that he hopes for a tax plan by the August recess. This comment dimmed the lights a little but came across as sane.

Then there's the batshit crazy stuff. It's hard to say focused on serious policy issues when Trump and his minions (like Bannon) are spewing lies and nonsense. At some point, the crazy stuff will over-whelm the serious stuff—some new kind of tipping point. Financial analysts (and corporate executives making capital spending and earnings repatriation decision) may continue to have reasonable expecta-tions of reform and change, but an increasing proportion will start deciding that it would be unwise to count on those changes. That will be because Trump and the Trumpettes are not likely to last. Trump will be impeached or resign before any real policy change can be announced and implemented. Lad-brokes has a 30.77% probability Trump will leave office this year, 2017. The probabilities go down, the farther out you go on the calendar.

If you Google "impeach Trump," you get 17 million hits. Impeachment is most likely to come from conflicts of interest, or maybe Russia-gate, but now lack of mental fitness could be the key. Former Nixon aide John Dean says Watergate took over 900 days but this one is at an accelerated pace. "And what I see or hear are echoes of Watergate. We don't have Watergate 2.0 yet, but we have something that is beginning to look like it could go there."

The gambling websites all have good odds Trump will resign or be impeached. Ladbrokes has10/11. Something named Paddy Power has 2 to 1. We had to go find out what these numbers mean... and dis-covered betting expert.com. Here it is (as of Friday; the weekend could move the numbers). We book-marked the page. It may come in handy.

Trump says major news outlets report "fake" news and has barred them from White House briefings. He is also declining to attend the White House Correspondents Dinner. (The last time a president did not attend was when Reagan was in the hospital after being shot.) The supposedly fake news purveyors are the New York Times, Washington Post, Los Angeles Times, CNN and Politico. They do not report false stories, they just report stories that show Trump in a bad light. The AP and Time mag boycotted the last briefing to show solidarity. And we were shocked by Nixon's "enemies list," which became a badge of honor for those on it.

Politico reported "The key to keeping Trump's Twitter habit under control, according to six former campaign officials, is to ensure that his personal media consumption includes a steady stream of praise. And when no such praise was to be found, staff would turn to friendly outlets to drum some up — and make sure it made its way to Trump's desk....A former senior campaign official said Nunberg and his successor, former communications director Jason Miller, were particularly skilled at using alternative media like Breitbart, Washington Examiner, Fox News, Infowars and the Daily Caller to show Trump positive coverage."

Bottom, bottom line: markets are prepared to be skeptical about the growth-and-inflation pushing capa-bilities of the upcoming Trump policies, assuming they have any substance at all and get past the ad-vertisement stage. It's conceivable that another round of reflation trades emerges, but it's equally possi-ble that yields falls further as the Fed is stymied in its effort to sell the March hike. Bloomberg calls it a bluff, which is sort of insulting (isn't it?). It's hard to get a deduction of a rising dollar out of this. In-stead we could get ranging and dueling channels. Traders, prepare to take losses.

Quote from a Reader: "As democracy is perfected, the office of president represents, more and more closely, the inner soul of the people. On some great and glorious day the plain folks of the land will reach their heart's desire at last and the White House will be adorned by a downright moron."

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.24 | SHORT USD | 02/17/17 | WEAK | 112.86 | 0.55% |

| GBP/USD | 1.2407 | LONG GBP | 01/24/17 | WEAK | 1.2451 | -0.35% |

| EUR/USD | 1.0586 | SHORT EURO | 02/10/17 | WEAK | 1.0643 | 0.54% |

| EUR/JPY | 118.80 | SHORT EURO | 02/03/17 | WEAK | 121.56 | 2.27% |

| EUR/GBP | 0.8532 | SHORT EURO | 02/16/17 | WEAK | 0.8490 | -0.49% |

| USD/CHF | 1.0070 | LONG USD | 02/10/17 | WEAK | 1.0024 | 0.46% |

| USD/CAD | 1.3112 | LONG USD | 02/22/17 | STRONG | 1.3174 | -0.47% |

| NZD/USD | 0.7193 | SHORT NZD | 02/10/17 | STRONG | 0.7185 | -0.11% |

| AUD/USD | 0.7673 | LONG AUD | 01/05/17 | WEAK | 0.7343 | 4.49% |

| AUD/JPY | 86.12 | LONG AUD | 02/09/17 | WEAK | 85.92 | 0.23% |

| USD/MXN | 19.8323 | SHORT USD | 01/31/17 | WEAK | 20.8108 | 4.70% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat