The ECB is starting to get itself in trouble

Outlook:

The ECB meets next week and don't forget it as you get short euros. Expectations are fully cooked that the bank will announce tapering, i.e., lesser asset purchases per month. One story has it that before QE began, there was an informal consensus that the QE balance sheet should not expand past €2.5 trillion. It's on track to near that level by year-end, implying a drastic cut in monthly purchases from €60 billion, already down from €85 billion, to avoid exceeding this cap.

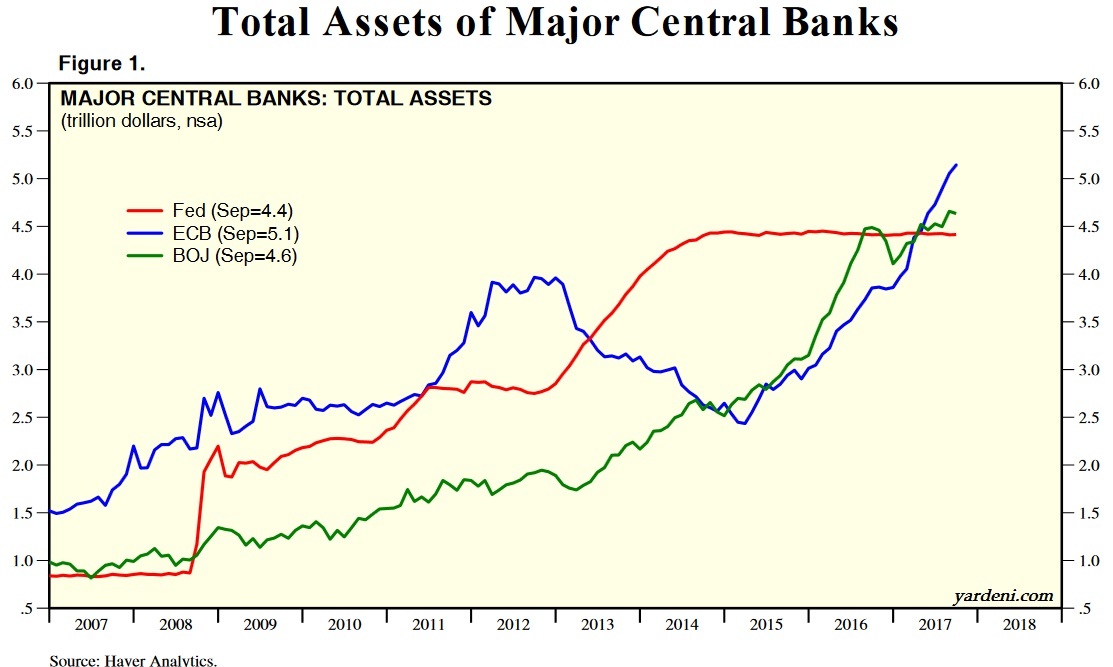

We don't know if there is a secret cap on the ECB balance sheet, but right now it's not a trivial matter. Remember that in March Bloomberg reported the ECB balance sheet had already exceeded the Fed's. By Sept, the ECB balance sheet (€4.3 trillion) matched Japan's GDP. And yesterday Yardeni published a series of stunning charts that will set your hair on fire.

First up is the three big QE players. ECB total assets are over €5 trillion and higher than the US and Ja-pan, with the QE portion at a little under half. The total assets of the three central banks is $14.2 trillion as of September.

Another chart shows total central bank assets as a percentage of GDP in local currency terms. The Fed has 23%. The ECB has 37.7%. The BoJ has... 92.2%. Nobody has ever written a rule about how much is too much, but if we assume bond issuance, both sovereign and corporate, is a function of GDP or at least related to it somehow, the ECB is far more exposed to charges of bubble-creation than the Fed. Let's not even talk about Japan.

Among the ECB details is a chart showing reserves, including gold, at a little over $600 million. We are not quite sure what this means. We toyed around with some scenarios and tried to find some litera-ture on the subject, but the connection between reserves (to buy food and arms when in dire need) and central banks asset levels is not something you can Google.

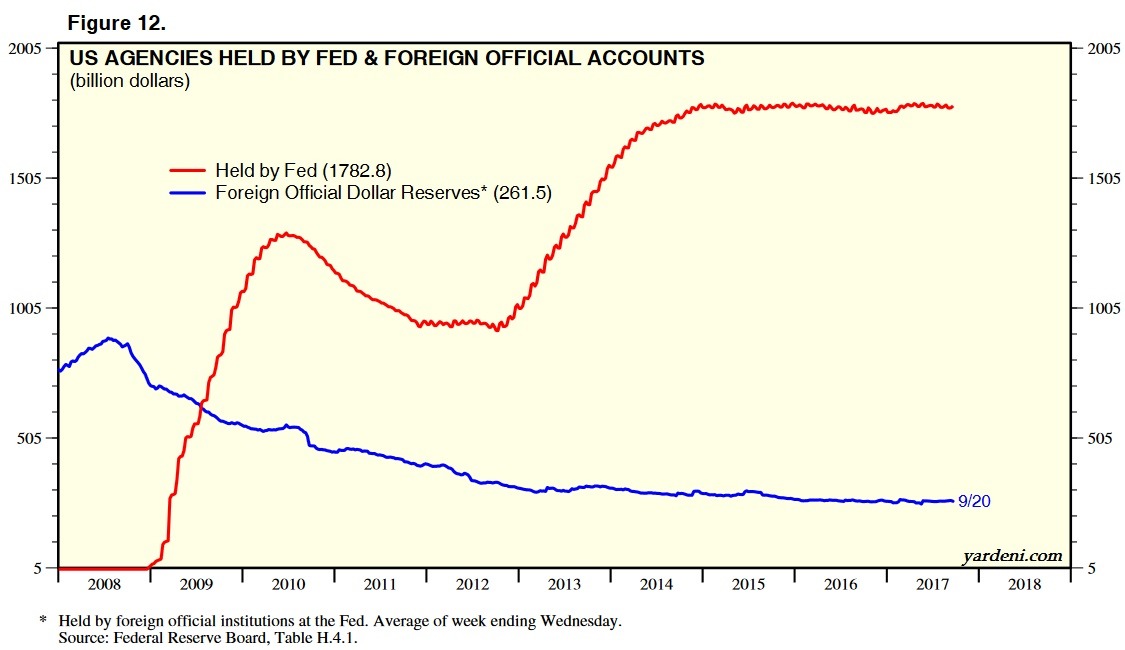

The scary chart is the last one. It shows Agency paper held by the Fed and that held by foreign central banks as reserves. We don't know why Yardeni included this chart—there is no narrative—but we can jump to the idea all too easily that when the Fed dumps Agencies, there won't be any foreign demand for them. Yields will spike.

In fact, that is probably the point of all this fretting over central bank balance sheets. Not that it's im-moral and wrong to let them get so big, but that when you contract them, you really don't know how the market is going to react. The obvious worry is that yields will have to rise, perhaps by a whole lot, to lure demand away from stock markets and real estate. We will have a classic burst bubble.

Burst bubbles mean dislocations, misallocations, and failures and bankruptcies. When the failed entities are big managed funds and pensions, there will be hell to pay. Too-cheap money drives excessive bor-rowing by people who can't or won't repay. Central bankers might do better to forget about the mys-tery of inflation and raise rates just to promote financial stability. This was the point of view of the BIS' Borio at the monetary policy conference last week.

Central bankers are probably not thinking about it, but the failure of the US justice system to put some of the bums in jail for the financial crisis of 2008 and the resulting disillusionment with the Establish-ment bears some blame for giving us Trump. Next time the justice system, and not only in the US, may have to prosecute the three-piece suit crowd, including the ratings agencies.

To return to the main point: the ECB is starting to get itself in trouble, regardless of whether there is a secret cap on QE purchases. The difficulties finding qualifying supply have been well-worn by now. In the absence of tapering, the balance sheet could go from 38% of GDP to some Japanese level. Japan gets away with all kinds of things in the financial world that nobody else can do but in the end, it's the scariest model of dysfunction and disobeying the rules of finance anyone has ever seen. The ECB doesn't want to emulate Japan lest it be accused of having the Japanese disease, a vaguely insulting terms that means the inability to exit deflation despite heroic measures.

So, bottom line, we believe the chatter about tapering. Assuming the ECB makes the tapering an-nouncement next week, rates should respond immediately (sell on the rumor). Granted, the Bund has a long way to go to catch up to the US 10-year, but maybe we should be looking only at the 2-year, the central bank barometer. The German 2-year is still negative at -0.73% and falling. The US 2-year is 1.551% and rising. You have to ask how long it will take for the ECB to find an additional 2.25% for the 2-year issues to break even. Then you have to ask what we have been asking since Fed tapering be-gan--why the euro is relatively strong when the yield diff so clearly favors the dollar. And what hap-pens to it when that differential narrows, which now looks like not happening for many months but you never know.

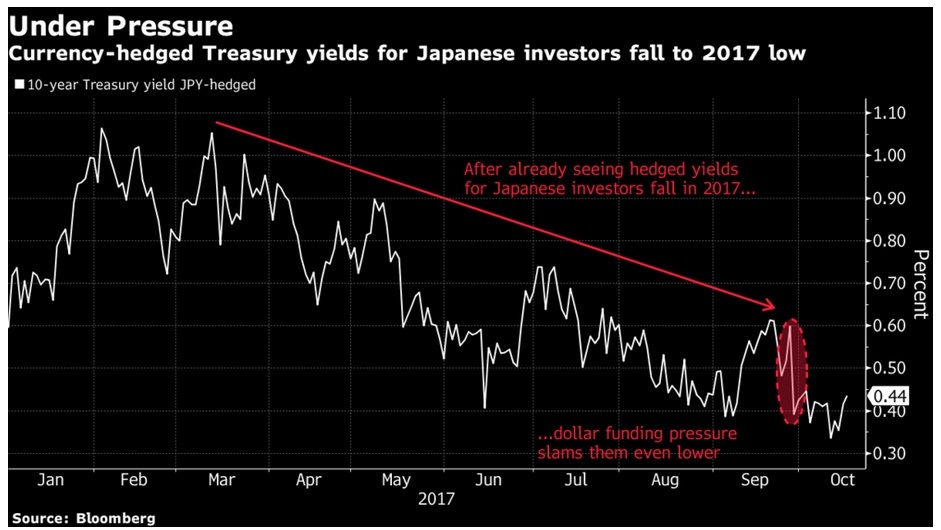

The only reason to favor the dollar under these conditions is if you expect US growth to become more robust. Meanwhile, the cost of currency swaps is higher so that those converting local currency debt to a dollar basis are paying more, while investors are getting less. According to Bloomberg, this price trend is the same thing as a dollar funding shortage, and if we get a repatriation bonus for US corpo-rates, it can only get worse. For example, "For Japanese investors who hedge currency risk, yields on 10-year Treasury notes fell to 0.34 percent last week, the lowest level of 2017 and down from over 1 percent in February and March. It's still more appealing than it was in mid-2016, when dollar funding markets got so tight -- and Treasury yields so low even on absolute basis -- that hedged 10-year yields turned negative for Japanese buyers." See the chart.

Wells Fargo notes that FX forwards imply a higher hedging cost for 13 of 15 currencies. And dollar asset holders do want to hedge. "Overseas investors have gobbled up U.S. corporate debt, leaving that market more vulnerable to currency volatility. International buyers own about $3.6 trillion of U.S. com-pany borrowings, a $600 billion increase in the past two years... "Wells Fargo says "The recent period of dollar strength alongside tighter spreads has drastically reduced relative value for global investors into USD credit." Yield-starved euro-based investors are seeing a contraction in the 5-year to under 20 bp from 60 bp in April. "... the no-brainer trade -- simply snapping up dollar credit -- is no more, lead-ing them to take on more duration and credit risk to juice returns."

If your mind is reeling from the disconnect between real assets and contingent ones like swaps, you are not alone. Notes and bonds are things for which one pays with real on-the-balance sheet money. They may be only electronic and not paper and ink, but they are real. Swaps, on the other hand, whether an investment or a hedge, are not real in the sense that they are not on the balance sheet and nearly always get unwound/reversed before maturity, leaving only the cost or return as a "real" cash payment. Is it correct or fair to consider a rising dollar premium to be a reflection of a dollar shortage? No, not in the real world, but derivatives can be not-real and still wreak havoc.

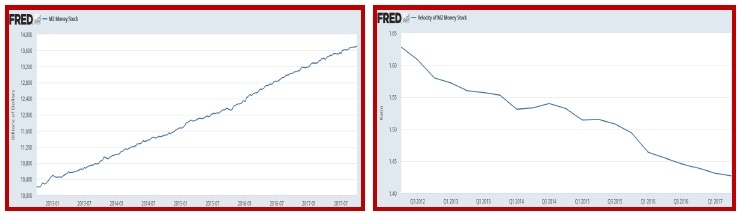

It seems silly to speak of a dollar shortage when so many are complaining about the Fed's engorged balance sheet at the same time. The Fed has been pumping money into the banking system for years. Money supply has increased from about $10.25 trillion in 2013 to $13.71 trillion as of Oct 2, according to the Fed. There is an even larger amount sitting in international banks in London. This money mostly sits in banks and is fully available to swaps-makers.

But sitting in banks is precisely the problem. It's not out circulating and multiplying. Velocity is still on the downswing. The twin charts show M2 money supply on the left and M2 velocity on the right. We continue to insist this is why we don't have inflation, but this time the reason to name velocity is to demonstrate that bankers' appetite for using that money in things like swaps, let alone authentic busi-ness activity, is very low. In other words, there is no actual shortage of dollars to fund anything. There is a shortage of bankers' interest in applying money to fund activities, including swaps. Banks would rather earn the paltry return on reserves than take risks. We do not know what the Dodd-Frank/Volcker Rules have to do with it, but they are probably a drag on swap activity, too.

This doesn't mean we shouldn't look at the swaps market as telling us something about the future of the dollar. It does mean that swaps prices have a far wider set of implications, too. What if de-regulation does get done? Does this mean swaps become cheaper? Yeah, probably.

Elsewhere, the UK picture has yet to be clear enough to see, but doom-and-gloom stories are not in short supply. If Brexit occurs without a trade deal, according to Bloomberg, many bad things will hap-pen to the UK economy. Economic growth will contract by £400 billion by 2020 (Rabobank). Exports will fall by £17 billion in four sectors alone (Baker McKenzie). Per capita income will drop by 2.6% (Brookings). Dire outcomes could occur in food and medicines, and smuggling in and out from N. Ire-land and the EU will take off, emboldening gangsters. The real economy consequences of a no-deal Brexit seem to outweigh the rate hike, which may well be one-and-done, anyway.

Tomorrow we get another chapter in the Catalonia story. We also get additional information about the Brexit talks. For the top item on the US agenda, tax reform (and repatriation), we will probably have to wait. And NAFTA seethes in the background. We would bet a dollar that Trump declares the US is withdrawing.

Bottom line, we honestly don't see why the dollar is being favored against the euro. We judge it's a correction from an oversold condition, and that makes the expected retracement levels more relevant. There is no "natural law" that says corrections should be x% of a move, but plenty of FX market play-ers see it that way, so it would be silly to ignore the idea.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 112.71 | SHORT USD | 10/15/17 | WEAK | 111.82 | -0.80% |

| GBP/USD | 1.3182 | SHORT GBP | 10/03/17 | WEAK | 1.3247 | 0.49% |

| EUR/USD | 1.1748 | SHORT EURO | 09/27/17 | WEAK | 1.1741 | -0.06% |

| EUR/JPY | 132.41 | SHORT EURO | 10/15/17 | WEAK | 131.86 | -0.42% |

| EUR/GBP | 0.8912 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 1.34% |

| USD/CHF | 0.9811 | LONG USD | 09/25/17 | WEAK | 0.9732 | 0.81% |

| USD/CAD | 1.2526 | LONG USD | 09/27/17 | WEAK | 1.2389 | 1.11% |

| NZD/USD | 0.7130 | SHORT NZD | 10/06/17 | STRONG | 0.7088 | -0.59% |

| AUD/USD | 0.7826 | SHORT AUD | 09/25/17 | WEAK | 0.7963 | 1.72% |

| AUD/JPY | 88.20 | SHORT AUD | 10/11/17 | WEAK | 87.35 | -0.97% |

| USD/MXN | 18.7880 | LONG USD | 09/22/17 | STRONG | 17.8066 | 5.51% |

| USD/BRL | 3.1577 | LONG USD | 09/27/17 | WEAK | 3.1670 | -0.29% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat