Non-Farm Payrolls Preview: defying the economic odds

- US labor market takes on even greater importance with equities falling, global economic and political concerns

- Underlying US economy continues to perform, forecast for status quo on jobs, wages, and unemployment

The US Labor Department will issue its Employment Situation Report on Friday December 7th at 8:30 am EST, 13:30 GMT. More colloquially known as the non-farm payrolls report for its headline statistic the monthly release details the state of the US labor market tracking job creation, the unemployment rate, earnings and other information. It is currently the most carefully followed American economic statistic.

Forecast

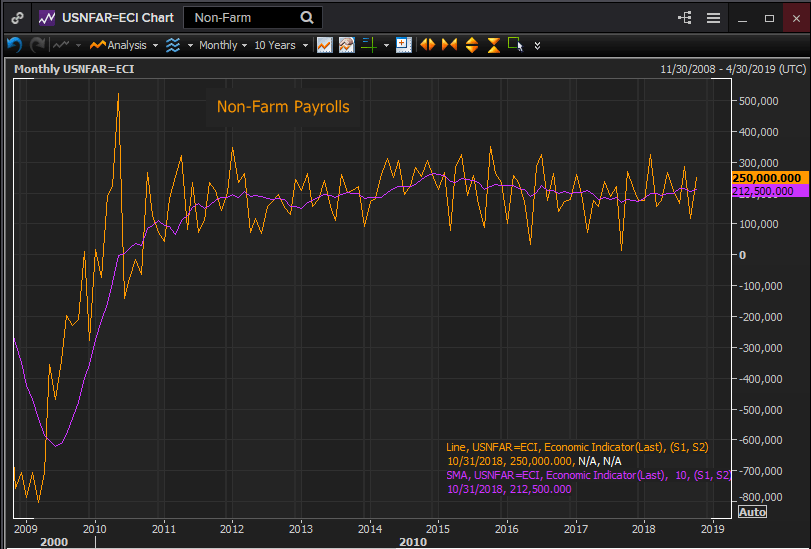

Non-farm payrolls are expected to rise by 205,000 in November, down from the prior month's exceptional 250,000. The unemployment rate is predicted to remain at 3.7% and annual average hourly earnings to have increased 3 % last month as in October.

US economic data: reality versus fear

The overall health of the American economy continues to be good and is reflected in US statistics.

Non-farm payrolls have averaged 212,500 per month this year through October. This is the best job creation since 2015. The unemployment rate has been at 3.7% for two months and below 4% for six of the last seven months. In the decades before the financial crash this would have been considered full employment and have the Federal Reserve looking over its shoulder for oncoming inflation.

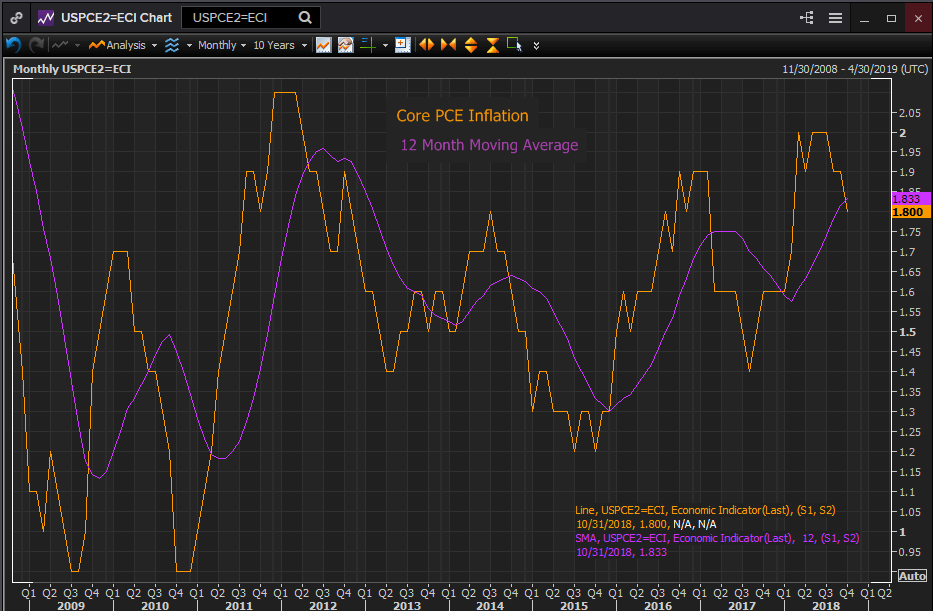

Instead the Core Personal Consumption Price Index, (core PCE prices) the Fed’s chosen measure dropped 0.1% in October to 1.8% annually. Over the past year it has averaged 1.8%. At no point in the more than nine years since the end of the recession in June 2009 has the 12 month average reached the central bank’s 2% target.

Business and consumer sentiment has sustained at high levels. The ISM manufacturing purchasing managers’ index came in at 59.3 in November. The average this year has been the highest since early 2005. Consumer outlook gauged by the Conference Board registered 135.7 last month and here also the average this year has been the strongest in 17 years.

The ADP private payrolls scored 179,000 in November, missing the 195,000 forecast. Its average since December of 200,900 is consistent with a robust labor market.

Gross domestic product, (GDP) has been 3.3% through the first three quarter and is on track for the best year since the financial crisis and the first over 3%.

There is one discordant note, minor but worthy of notice. Weekly jobless claims, the most accurate early indicator in the job market have been rising since the end of the third quarter. The four week moving average has gone from 206,000 in the week of September 15th to 228,000 the first week in December. However, that September average was a historical low and the rise to December still leaves the statistic below almost the entire historical record.

Equity concerns

Despite the excellent economic statistics equites have had a rough Fall. The major US indexes are now flat or just below for the year. The Dow is off 9% from its October high and the S&P 500 has entered correction down 10% from its September top.

The concerns for equity holders are not primarily centered in the US but reflect global political and economic turmoil. The trade dispute between the US and China, while in assumed abeyance since the agreement between Presidents Trump and XI after the G-20, is far from being settled.

In Europe the British exit from the EU is in chaos with Prime Minister May likely to lose the approval of the Commons leaving the entire departure project in confusion.

On the continent Italy is at loggerheads with the EU Commission over its budget deficit and France has seen some of the worst street riots in decades forcing President Macron into retreat on the government’s fuel tax.

Germany had negative GDP in the third quarter and Italy was flat. The EU has a whole seems headed into recession as politics takes its toll on business and consumer sentiment.

Federal Reserve policy

The Fed has begun to scale back the expectation for next year’s rate increases after this month’s assumed 0.25%. The FOMC Projection Materials that will be issued after the December 19th meeting will detail any changes in outlook.

The labor market has been a major success for US economic and rate policy over the past two years. That will need to continue to keep the Fed on even a reduced rate increase policy in 2019 and beyond.

Charts: Reuters

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.