Expect Fed speakers to address normalization of monetary policy

Outlook:

It's a slow data week, with Japan releasing PMI on Thursday and the eurozone on Friday. In the US, we get existing home sales on Wednesday and new homes sales on Friday. We'd mention the current account tomorrow but nobody has paid attention to the current account since the 1980's.

Wall Street in Advance's Lynne notes that Thursday brings the Fed's big bank stress test results. Which of the 11 big banks will fail this time? Maybe the ethically challenged Wells Fargo. Lynn suggests the stress tests might be one of the "regulations" Trump will target. Next week (6/28) is the capital adequacy tests and the spate of dividend announcements that passing the test permits.

Two other equity market developments are the newly re-jiggered US indices that should generate some volume today, and how MSCI will treat Chinese shares tomorrow. The FT reports the big question is whether MSCI includes A-shares (domestic Chinese companies) after excluding them for the past three years. Managers required to mirror the MSCI indices in their holdings will be forced to buy China. These days it's 169 companies vs. 448 in earlier years, or only 0.5% MSCI Emerging Markets Index. It's a big deal for China, connoting "respect."

In the absence of some decent data, where do we look for guidance on FX? Back to the central banks, maybe. Today NY Fed Dudley speaks at 8 am and he has been known to move markets. There is some talk about whether the Fed was too hawkish last week—not if you believe the bond yields—and what, exactly, is the Bank of England going to do? Three dissenters is a big deal. The Reserve Bank of New Zealand meets this week with no change expected. Overall, we are waiting for somebody, anybody, to follow the Fed toward normalization.

We need more analysis of normalization. It's a tough nut to crack, apparently. Normalization in statistics means to adjust an entire series to a new baseline. Yellen referred to this definition when she said the Fed funds rate will not return to the high end of the range and is permanently lower. Remember, the dot plots show the Fed funds rate topping out at 3% for the "longer term." We may expect at least some of the Fed speakers this week to address normalization. In addition to Dudley this morning (whose primary concern is, quite properly, liquidity, we get Chicago Fed Evans tonight, and then Fischer, Rosengren, Kaplan, Powell and Bullard later in the week. They can't all avoid normalization, can they?

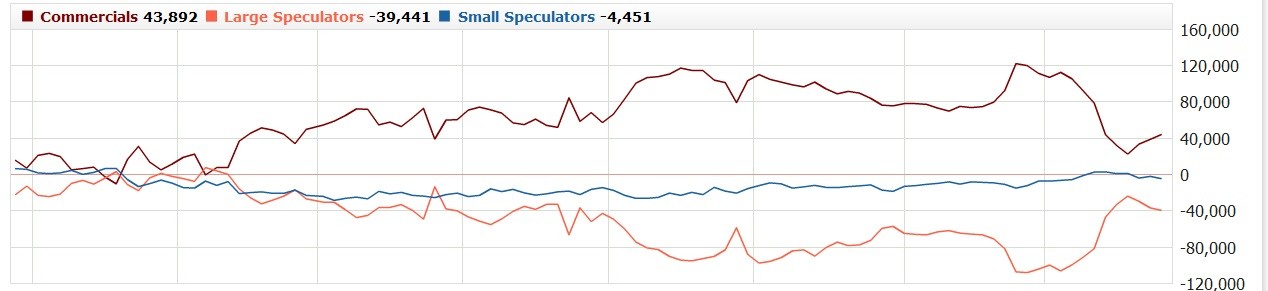

Meanwhile, support for the euro continues to build. See Oanda's COT report for non-commercial futures positions in the euro. It's getting bigger all the time. Not enough to set your hair on fire, but given the dollar's yield advantage, instructive.

The more curious situation is sterling. Both large and small specs reduced shorts recently, but sentiment remains negative. See this chart (from MyFXBook). Now we need the commercials to flip.

In the absence of decent data or positioning information, that leaves politics as an unsteady guide to financial markets. On the whole, financial markets in advanced economies with stable institutions are not much influenced by political events. That's for emerging markets. But the CAC jumped on the Macron win this weekend. Macron got a giant vote of confidence by winning a solid majority in the assembly with his allied party (350 of 577 seats). LePen's party got nine. That's right, nine. The outcome has tremendous meaning although nobody is quite sure what it is. It might be that Macron founded his party only 14 months ago, so perhaps voters are just thoroughly disgusted with the old parties. This may be a French version of the Bernie Sanders phenomenon.

In Europe, UK Brexit negotiator Davis met with EC counterpart Barnier for the first day of Brexit talks. Barnier said the immediate goal is to "identify and prioritize the first batch of topics." Amicability is the order of the day. Wonder how long it lasts. The plan is supposed to be in place by year-end.

In the US, the Republicans are crafting a secret health care bill. We keep hearing it will result in some 20 million persons losing health insurance and is designed only to deliver the $800 billion in savings needed for the tax reform bill. The goal is get it in place by July 4. Some traders are gearing up for another run at the reflation trade if we do get tax reform. This seems to consist chiefly of divining what equities the fat cats will buy with their tax windfall.

Elsewhere in US politics, the Washington Post cited five unnamed sources saying Trump is indeed being investigated by special counsel Mueller for obstruction of justice. Trump seemed to confirm it in a tweet, although he was actually trying to deride the report, resulting in his lawyer denying he is under investigation all over weekend TV. Nobody came out of it looking intelligent or reasonable. Most of all, Trump continues to show no interest in Russian intrusion into the US political process. That's the real crime. We hire presidents to care more about things like that than about their "brand."

It's the 45th anniversary of the start of Watergate and one of the cable channels is playing it up for all it's worth. One of the movies channels showed All The President's Men and the documentaries on Watergate showed some more. Clapper is right—the Russians interfering in our election is far bigger than the Watergate burglary, although Nixon did a lot worse than try to cover up the burglary—ordering the beating of war protester Ellsberg, ordering the IRS to audit critics, and surveilling/wiretapping "enemies."

The Trump presidency is not going to end well.

Note to Readers: RTS has launched a Trade Copier service. We place our trades from the Afternoon Traders' Advisory in the retail spot market and your MT4 account mirrors the trades taken in the RTS account. You don't have to lift a finger. You get to pick how much leverage and exactly which currencies you want to include. If you are interested, please contact Paul Harris at [email protected] or visit http://www.rtsforex.com/trade-copier/.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 110.97 | SHORT USD | 05/18/17 | WEAK | 110.36 | -0.55% |

| GBP/USD | 1.2806 | SHORT GBP | 06/12/17 | STRONG | 1.2701 | -0.83% |

| EUR/USD | 1.1191 | SHORT EURO | 06/12/17 | WEAK | 1.1218 | 0.24% |

| EUR/JPY | 124.18 | SHORT EURO | 07/08/17 | WEAK | 123.65 | -0.43% |

| EUR/GBP | 0.8738 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 2.92% |

| USD/CHF | 0.9717 | LONG USD | 06/12/17 | WEAK | 0.9675 | 0.43% |

| USD/CAD | 1.3229 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 2.88% |

| NZD/USD | 0.7276 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 3.03% |

| AUD/USD | 0.7609 | LONG AUD | 06/08/17 | STRONG | 0.7548 | 0.81% |

| AUD/JPY | 84.44 | LONG AUD | 06/16/17 | WEAK | 84.65 | -0.25% |

| USD/MXN | 17.9331 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 4.15% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat