Euro advantage is on faster growth and industrial recovery, not Draghi talk

Outlook:

The euro rally on Draghi perhaps being less dovish is a case of sentiment over fact or even anything resembling reasonable interpretation. We listened to every minute of Draghi's press conference and found only the tiniest sliver of a hint that tapering might be discussed in the fall. Bloomberg analysts then proceeded to debate whether the Sept 8 policy meeting qualifies as "autumn."

Bloomberg has a cute story on how Draghi is tapering his number of words if not the content, shortening the press conferences from an hour to about 45 minutes. Talk about stretching a point.

This would be ridiculous if it were not deadly serious. And consider the context. The Fed is supposed to be hiking again in Sept or at least before year-end, with many analysts picking the December meet-ing as the likeliest date, while the ECB chief is busy denying the bank is even talking about reducing QE purchases, let alone hiking. You'd think the dollar has an obvious advantage.

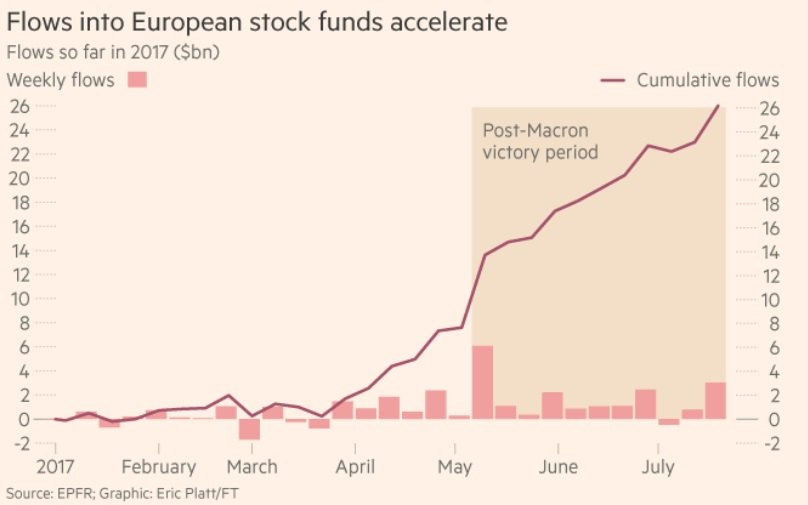

But it doesn't. Some of the advantage enjoyed by the euro pertains to faster growth and industrial re-covery. European PMI's and other measures are beating the US versions. "Soft" sentiment indicators are higher in the Europe, too. And here's a kicker: inflows to European equities are soaring, despite projected rate hikes traditionally dimming the equity lightbulb.

The FT reports "Investors added more than $3bn to dedicated European equity funds in the week to July 19, lifting inflows for the year to more than $26bn, according to data provider EPFR. With the backdrop of a quickening economic recovery — providing central bank policymakers an opening to debate when to reduce stimulus measures — sectors typically tied to faster growth have regained an edge in Europe.

"... The additions to European stocks contrasted with the fifth straight week of redemptions from US equity funds. Investors withdrew $840m in the week to July 19, buoying outflows since late-June to nearly $20bn." Investors still favor US tech, however, despite Trumpian shenanigans cutting the heart out of growth expectations in the US.

Across the channel, we are giving Brexit short shrift. That's because there is an overabundance of com-mentary but very little hard news. Bloomberg reports today "Two rounds into its Brexit fight, Britain may be learning to love the idea of a transitional deal.

"Four days of talks in Brussels involving 140 officials laid bare just how little each side is willing to concede. Everyone wanted a quick deal, but the sticking points in the second round of negotiations are the bill Britain will pay, what to do about the Irish border and even the rights of British and EU citi-zens.

"The talks suggest it may be unrealistic to think the divorce can be wrapped up in two years, and Fri-day's newspapers in the U.K. say the nation may be considering adopting a more conciliatory ap-proach."

Conciliation or not, Britain is woefully unprepared for Brexit. One former official said UK players are living in "cloud cuckoo land" if they think they will get a deal by March 2019. Yesterday the govern-ment met with business organization, including the British Chamber of Commerce, for the first time... more than year after the Brexit vote. But a YouGov pols shows that while the EU comprises 85% of trading partners, almost half of British exporters have not reviewed their strategies.

The UK press reports the UK seems to accept that EU citizens will have free access for four years after the final exit. Yeah, so what then? The alternative to muddling through is... utter failure.

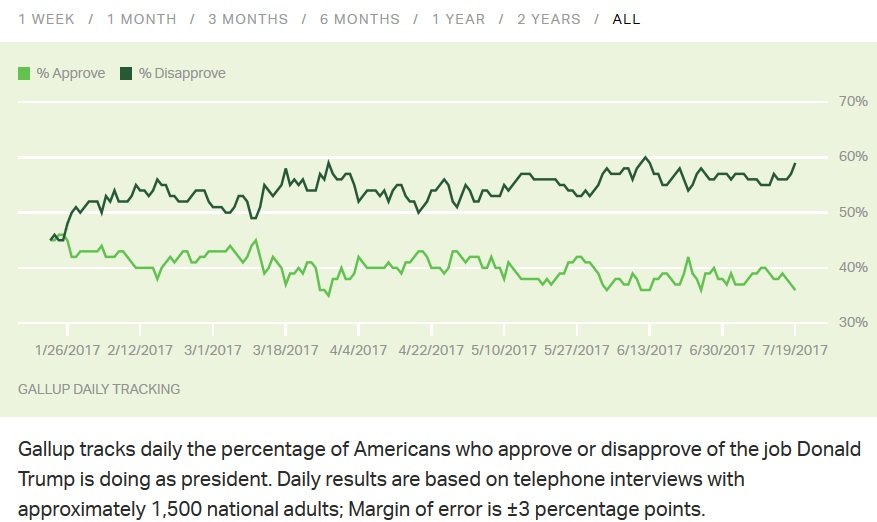

We have to say, again, that we don't know and can't judge how much anti-US and anti-Trump senti-ment is affecting the dollar. We are inclined to think it's a lot. The man we elected is an utter jackass. He's not doing his job. The ship of state is adrift while the captain concerns himself with self-image. Worse, he looks ridiculous on the global public stage and looks weak and emotionally unstable because he can be so easily played. See the Gallup approval ratings below. Nearly 60% disapprove of Trump and his performance, something echoed in the Rasmussen polls. We have learned the hard way to dis-trust polls, but still. Based on the likely increasing instability of US leadership, we say the dollar is toast.

Politics: The White House chief ethics officer resigned because he lacked the tools to deal with con-flicts of interest in the Trump administration. He has started to appear on TV. Trump's chief legal spokesman resigned yesterday because of Trump's NYT interview, which Trump didn't bother to tell the staff or legal team about. As one lawyer said of Trump earlier this year: he's a bad client—he doesn't pay and he doesn't listen.

Now Trump is projecting that the special counsel team of Mueller has conflicts of interest. This seems to consist chiefly of some having given campaign contributions to Dems, as Trump himself did for dec-ades before becoming a Plub.

But the point is that Trump is trying to intimidate those who are investigating him. He considers him-self above the law and even asked whether he could pardon his family, his staff and himself... note that when a person accepts a presidential pardon, he also accepts a guilty plea.

Trump keeps saying he can fire Mueller. Not without setting off a "chain reaction," according to the chief Bloomberg editor. Technically only the Attorney General can fire the special counsel and even then he needs "cause." So Trump could have to fire acting AG Rosenstein first, and then try to get someone else approved by the Senate who would fire Mueller. In other words, a Nixonian Saturday night massacre. It's not hysterical overstatement to say we are on the threshold of a constitutional cri-sis. This is not going to end well.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.62 | SHORT USD | 07/19/17 | WEAK | 111.96 | 0.30% |

| GBP/USD | 1.3006 | LONG GBP | 06/28/17 | WEAK | 1.2701 | 2.40% |

| EUR/USD | 1.1646 | LONG EURO | 06/28/17 | STRONG | 1.1218 | 3.82% |

| EUR/JPY | 129.99 | LONG EURO | 06/27/17 | WEAK | 125.73 | 3.39% |

| EUR/GBP | 0.8954 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 5.47% |

| USD/CHF | 0.9501 | SHORT USD | 06/28/17 | WEAK | 0.9675 | 1.80% |

| USD/CAD | 1.2572 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 7.70% |

| NZD/USD | 0.7441 | LONG NZD | 05/30/17 | STRONG | 0.7062 | 5.37% |

| AUD/USD | 0.7928 | LONG AUD | 06/08/17 | STRONG | 0.7548 | 5.03% |

| AUD/JPY | 88.49 | LONG AUD | 06/16/17 | WEAK | 84.65 | 4.54% |

| USD/MXN | 17.4814 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 6.57% |

| USD/BRL | 3.1211 | SHORT USD | 07/17/17 | WEAK | 3.1794 | 1.83% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat