Takaichi doesn’t want higher rates, and the Japanese Yen doesn’t like it

The Japanese Yen has been underperforming against major currencies and there’s little reason to expect a turnaround anytime soon.

Persistent worries about Japan's fiscal health and reduced chances of rapid interest rate hikes by the Bank of Japan certainly don’t help the Japanese currency.

Prospects of more stimulus fuel fiscal concerns

The emergence of Prime Minister Sanae Takaichi in October 2025 fueled speculations about more aggressive fiscal policies aimed at securing stronger economic growth in Japan.

These expectations were recently reaffirmed by Japan's weak GDP report, which showed that the economy expanded at an annualized rate of just 0.2% in the fourth quarter of 2025, narrowly avoiding a technical recession following a downwardly revised 2.6% contraction in the previous quarter.

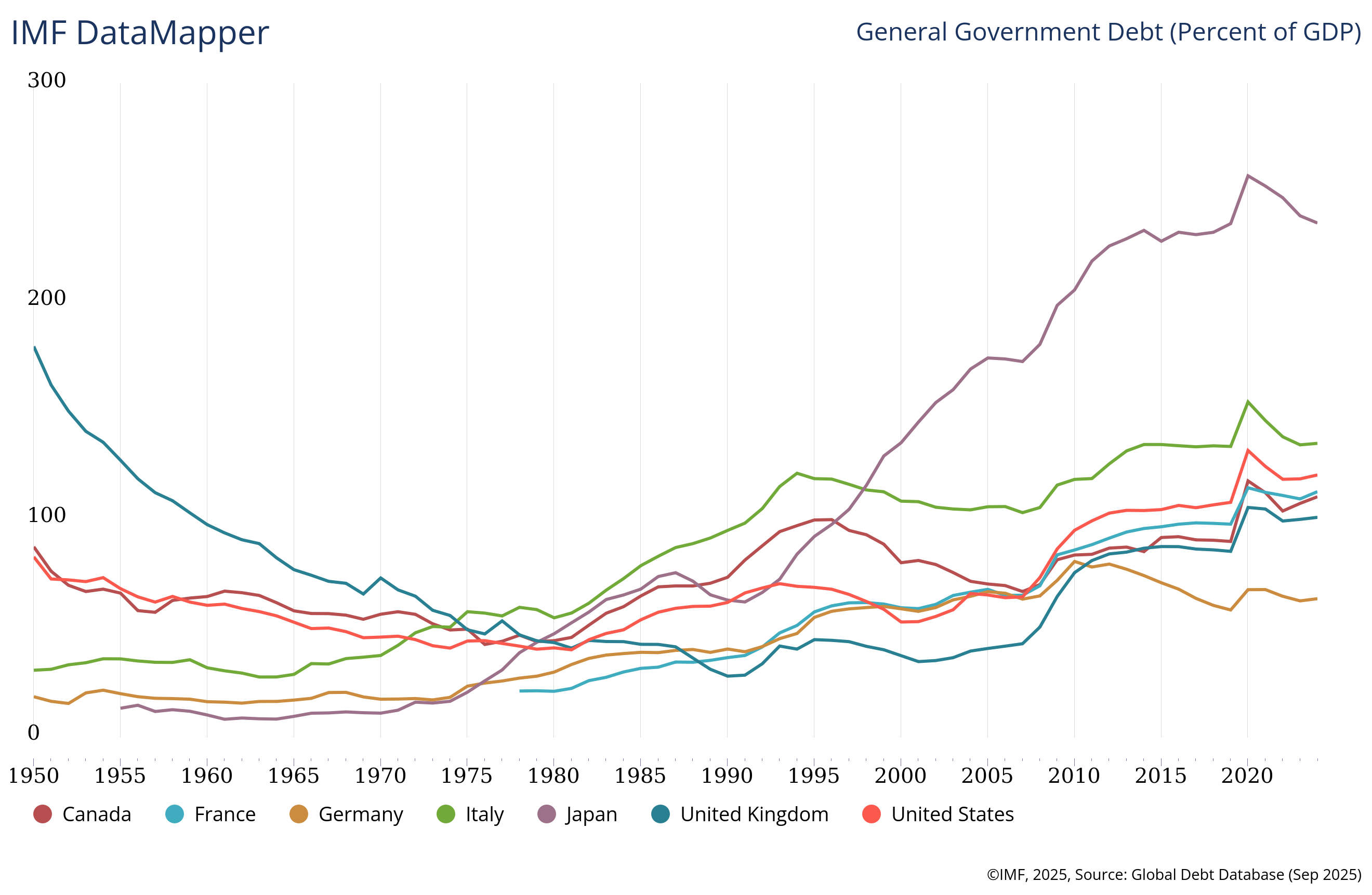

Low growth isn’t good news for the country, whose public debt-to-GDP ratio exceeds 230% and is the highest among G7 economies.

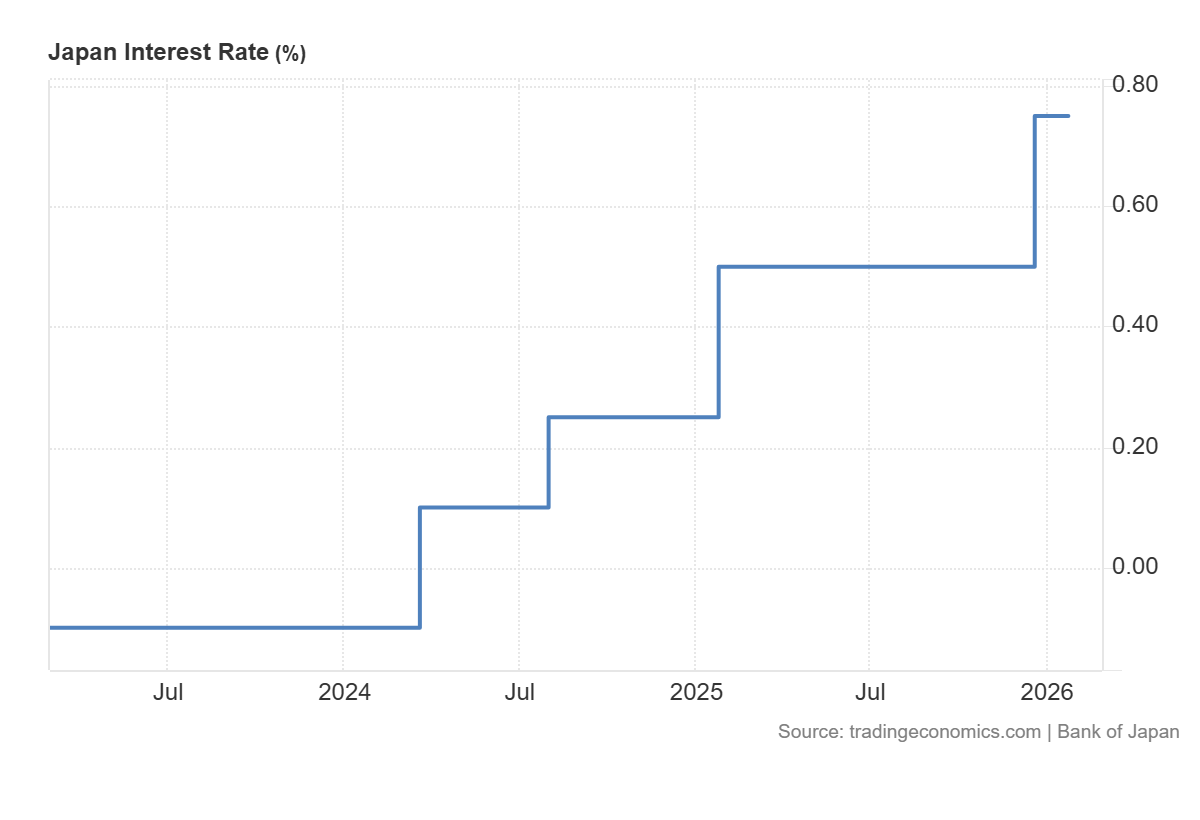

Given that the BoJ has begun to normalize its monetary policy after more than a decade of massive stimulus, the sustainability of this debt is a major concern. The central bank has increased the policy rate four times since 2024, for a total of 85 basis points. Moreover, the BoJ has indicated that it will stick to its historic process of policy normalization, which makes fiscal spending even more expensive to fund.

A custom-made BoJ?

The new administration led by the recently reelected PM Takaichi is starting to extend its tentacles into the BoJ to make sure the central bank supports her pro-growth stance.

Recent reports suggest that Takaichi herself expressed her reservations about more rate hikes in a meeting last week with the BoJ Governor Kazuo Ueda. Furthermore, the Japanese government on Wednesday nominated two reflationists (doves) – Toichiro Asada and Ayano Sato – to join the central bank's nine-member board, offering signs of how Takaichi may influence monetary policy.

Of course, these moves forced investors to temper bets for rate hikes by the BoJ.

The interaction between de-prioritizing debt reduction and central bank independence suggests that the government may force the BoJ to keep rates low to make interest payments manageable.

This could overshadow talks of official involvement by policymakers to stop the persistent weakening of the JPY.

No respite in sight for the Japanese Yen

The recent repeated rebounds from a technically significant 200-day Exponential Moving Average (EMA) favor the USD/JPY bulls. This sets the stage for a move beyond the recent swing high, towards testing the intervention threshold level near the 160.00 psychological mark.

-1772097342665-1772097342667.png)

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.