EUR/USD Forecast 2018: get ready to embrace a stronger EUR despite Draghi & Trump

What it was supposed to be the year of the Fed and the USD, ended up being the year of the ECB and the EUR. For sure, central banks were the main market motor this past twelve months, sharing the leadership with politics.

As promised, the US Central Bank ended 2017 rising rates three times, while the ECB maintained its QE, trimming it by half, but extending it well into 2018. Both economies grew throughout the year, but the EU outpaced the US.

"Surprisingly," inflation remains subdued. At least that is what the US Federal Reserve´s head, Janet Yellen, says. But inflation is not only an issue in the US, it's also a drag in the Eurozone, and the main reason why QE has been extended. That, and the fact that policymakers fear a too-strong EUR will affect the pace of economic growth.

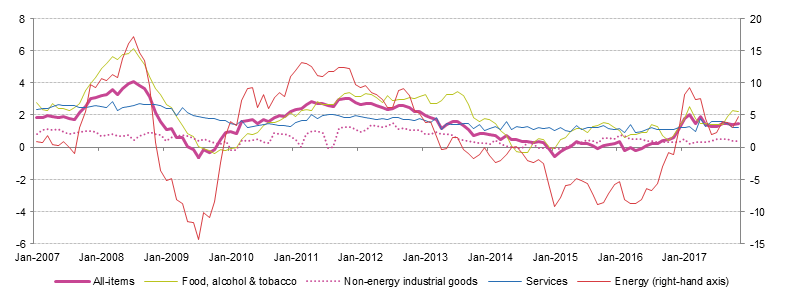

According to the latest official release by Eurostat, the Euro area annual inflation was 1.5 % in November 2017, up from 1.4 % in October 2017. Looking at the main components of euro area inflation, energy had the highest annual rate in November (4.7 %, compared with 3.0 % in October), followed by food, alcohol & tobacco (2.2 %, compared with 2.3 % in October), services (1.2 %, stable compared with October) and non-energy industrial goods (0.4 %, stable compared with October).

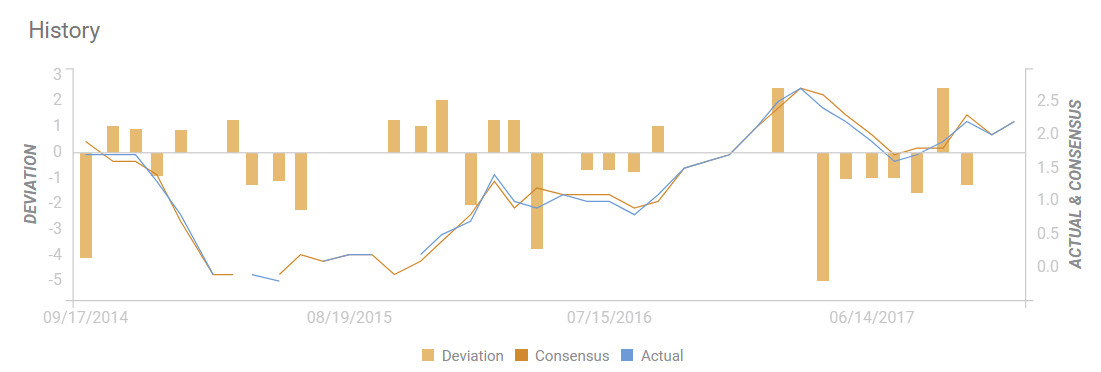

The latest US Bureau of Labor Statistics reported that the CPI for All Urban Consumers (CPI-U) rose 0.4 percent in November on a seasonally adjusted basis, the U.S. Over the last 12 months, the all items index rose 2.2 percent. The energy index rose 3.9 percent and accounted for about three-fourths of the all items increase. The gasoline index increased 7.3 percent, and the other energy component indexes also rose. The food index was unchanged in November, with the index for food at home declining slightly.

US Consumer Price Index (YoY)

In both cases, is clear that energy prices are behind inflation gains, not precisely what the central banks need. Core reading excluding volatile food and energy prices are well below the desired 2% by the US Federal Reserve, or the "below, but close to, 2%" from the ECB.

Central banks heading into 2018

The ECB reduced its bond-purchasing program to €30 billion from €60 billion, starting in January, extending its monetary stimulus program until at least September, "or longer if needed." A rate hike in the Union is out of the table for now.

The Federal Reserve, on the other hand, foresees three rate hikes for this 2018, and will continue shrinking its balance sheet, a process that started last October with just $10 billion a month to start, $6 billion in Treasuries and $4 billion in mortgage-backed securities per month, amounts that will slowly rose every three months until reaching $30 billion and $20 billion per month, respectively. There's a loose wire within the Fed, and that is the end of Yellen's mandate: next February, Jerome Powell will become the new central bank's chief, and the market is yet to see how he will handle monetary policy.

Beyond the "Powell" factor, central banks are expected to continue in the path of normalization, with no major surprises expected for this year.

Politics: "make America great again"

A whole book won't be enough to describe how politics affected the FX board along this 2017. Brexit and Trump's victory in the US presidential election have been in the spotlight for the past 12 months and nothing indicates that they will move to the background next year. In fact, seems that politics will continue to share the leadership with central banks, if not outpace it.

Trump has made promises when he took the office, and not even one has been fulfilled by the end of December. But maybe one will fall in place 10 days before the year end, as on this December 20th, there are big chances that the tax-reform project will become a law. The Obamacare reject bill has failed uncountable times, despite the Republican majority in the Senate that by the way, has been shrinking.

There is no news on "infrastructure investment," but protectionism´s measures and veiled menaces of a war with North Korea have been at the top of the headlines at least twice every single month of his Government. The wall hasn't been built yet.

Trump reviled China, and Canada, and Mexico, and.. pretty much every other country that stood in his way. Among the unfilled campaign promises is getting tougher on trade with China, but on contrary, he opened talks with the country on improving economic ties. He also threatened continuously to break the 23-year-old free-trade agreement with Mexico and Canada. In a world that moves deeply into the globalized model, the US Government just wants to "make America great again."

The world will likely survive with the USA leaving the model, and the US will probably do the same, despite Trump, but be sure, interesting times are ahead of us.

In Europe, the main drag on the political side is Brexit. But so far, EU's chief negotiator Michel Barnier has imposed the EU´s will over the UK that will pay a much higher cost that the so-called "divorce bill" with its decision to leave the Union.

Powell will have to deal with stubbornly low inflation and Trump's measures. Draghi, with a stronger EUR that, he thinks, could harm the delicate balance between strong growth and moderate increasing inflation.

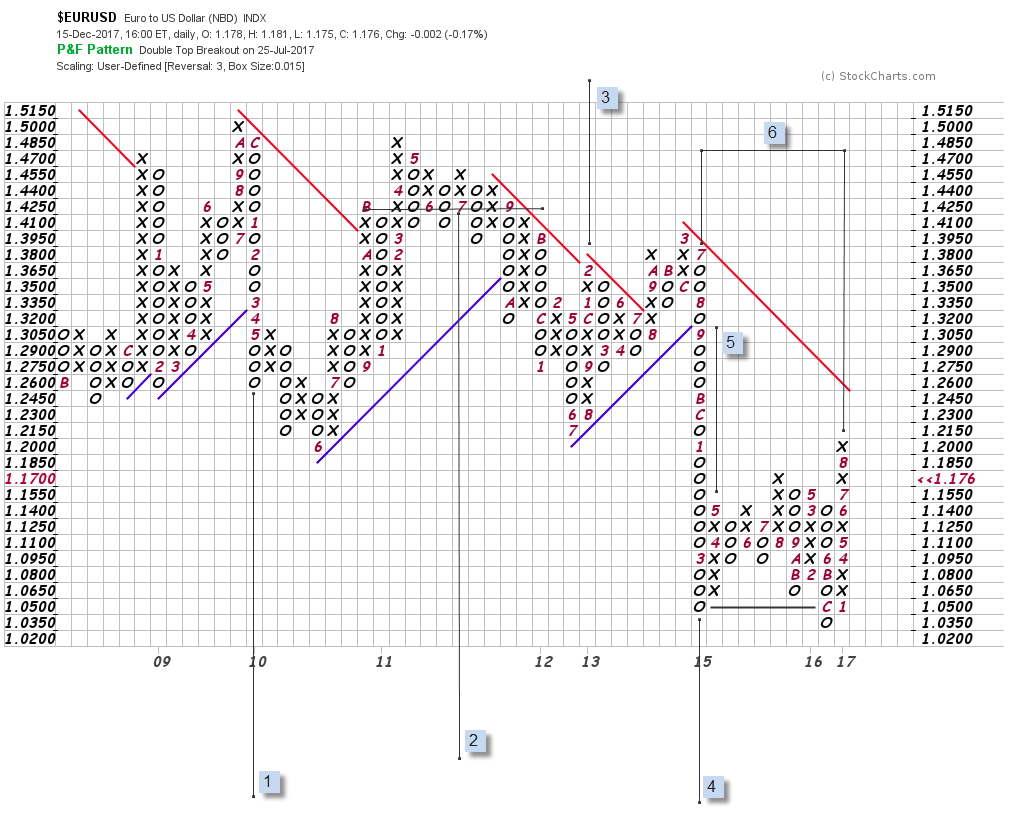

EUR/USD technical outlook

-636495496029356392.png)

The EUR/USD pair gained roughly 13% in 2017 from its lows at 1.0340 to the current 1.1850 region, having topped at 1.2092 in September. Between January 2015 and July this year, the EUR/USD pair was confined to a well-defined range between 1.0400 and 1.1460. The following bullish breakout has entered in a consolidative phase after September's monetary policy meetings from both central banks, and given that, at this point, upcoming decisions are highly predictable, investors are seeking for new catalysts to define the trend. Clearly, politics have most of the numbers to win that place.

A naked weekly chart clearly shows that the top of the over two-year's range has become a line in the sand for dominant bulls, as an approach to it mid-November saw the pair bouncing back toward its highs. The upward momentum eased, but as long as the price remains above the top on that range, in the 1.14/1.15 area, bears have no chance. In fact, the multiple lows around the 1.0450 region suggest that there's room for a rally towards 1.2500, with a huge psychological resistance in the way at 1.2100, as the pair topped at 1.2101 in January 2015, and at 1.2092 last September.

Against Draghi's will, get ready to embrace a stronger EUR in 2018.

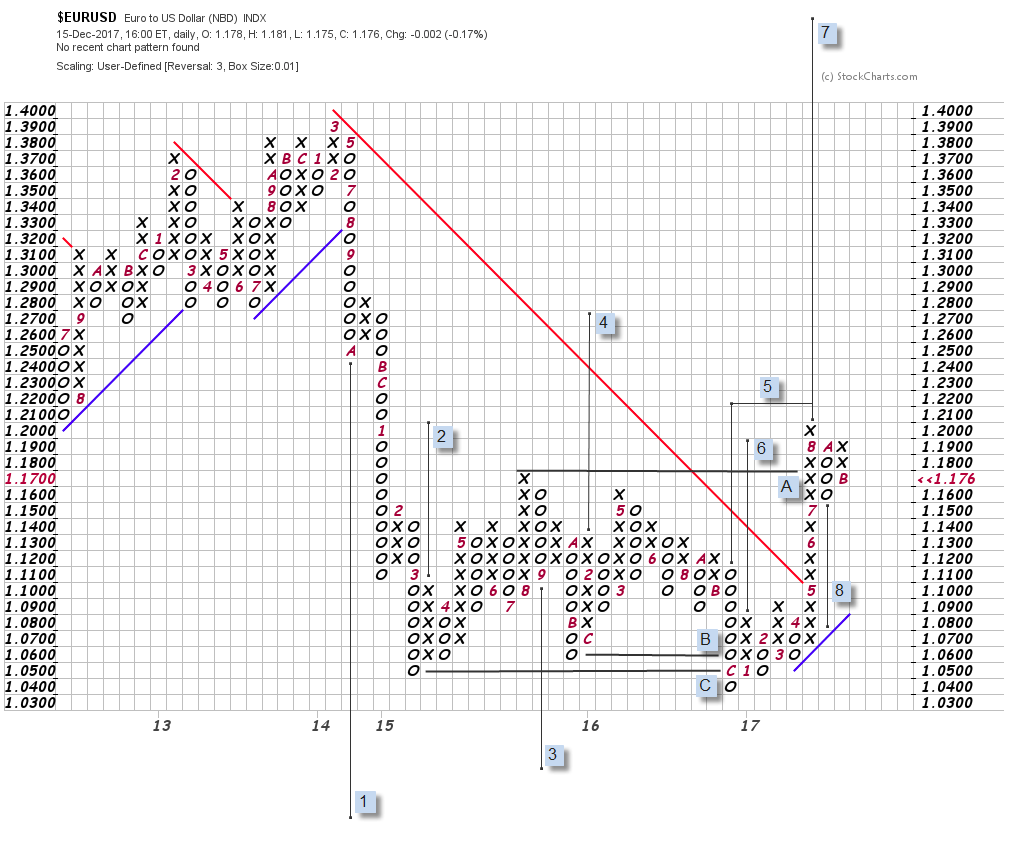

EUR/USD Point & Figure Chart

Downside count 1 established from the 2009 top is still active and points at 0.9700 as a target. Thereafter, several upside counts have been established but all of them were negated with the 2014 waterfall dive in the EUR/USD exchange rate. This is the case of count 3 at 1.66. In between, the horizontal count 2 is still unfilled and points to 0.9900. The free fall column enabled count 4 squarely eyeing the 0.3500 area which right now does not look distinctly possible. Further price development since 2015 resulted in the establishment of counts 5 (vertical) which was negated with the low of 2016, and count 6 (horizontal) which is now the strongest influence in this chart, pointing at 1.4800.

On the 100-pip box chart bellow, active counts point at 1.2200 and 1.4800 on the upside, but at the same time, activated bearish counts target 1.0800 and then 0.9700 below parity.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.