Don't mistake employment and investment with inflation

Outlook:

The ECB meets in ten days (Oct 26) and may announce a cut in asset-buying to begin next year, aka tapering. This is going to be euro-supportive no matter what else happens ahead of time, even a clash between Catalans and Spanish national police. At this point it looks like the Catalans will retreat, not least because of political parties squabbling but also because the independence "mandate" is feeble, with only 40% of voters turning out for that referendum. Rajoy is giving Catalonia plenty of rope and they are hanging themselves. The FT headline reads "Madrid gives Catalonia until Thursday to drop secession--Puigdemont refusal to clarify intentions paves way for Spanish government's ‘next steps.'"

The euro's current corrective dip is permitted by total confusion over how to think about the US econo-my and US political situation. The incoherent foreign policy statements by the Jackass-in-Chief—getting support from the spineless foreign affairs advisors—is being ignored, since it is literally not understand-able. The inflation data had only a fleeting effect, in part also because of double-talk. The FOMC minutes said there are worries low inflation might be persistent and due to factors not understood, but Yellen says she guesses it's not persistent.

For the US outlook, that pretty much leaves the question of who replaces Yellen when her term ends in February—and tax reform. The replacement story is turning into one of Trump's reality TV shows and not worth the time to follow. As for tax reform, from what we know so far, all the proposals end up being a tax cuts for rich people, exactly as we have come to expect from Republicans. Krugman has a blazing op-ed in the NYT about every single White House assertion being a lie. The fun part is that if the deductibility of state and local taxes is not removed, there goes several hundred billion in tax savings that Trump wants to spend on The Wall.

Even the IMF is now assuming no US fiscal stimulus in the 2018 WEO forecasts. In addition, Yellen says the Fed has not incorporated any tax cuts or changes in domestic fiscal policy in its plans. "We're uncertain about the size, timing and composition of changes that will actually be put into effect." According to the NYT, she says "anticipation of changes like tax cuts has buoyed measures of consumer and business confidence, but there is little evidence so far of increased investment. She said the Fed similarly is taking ‘a kind of wait-and-see attitude.'"

Whatever happens on the political front, inflation is always and forever a key factor. We just had a dis-appointing US release and while it's not the Fed's preferred measure, it's a measure. It's simply not good enough for the Fed chief to say the lack of inflationary pressure is mysterious in the context of low unemployment and moderate growth in things like industrial production. So to whom should we write to complain? We are stuck with that judgment.

This week we get inflation data from China, already out, New Zealand, Canada and the UK. Tomorrow's UK data is not likely to change the overall market judgment, based on Carney's comments, that a hike is a certainty. At a guess, the hike will overpower the Brexit mess.

We get more inflation-related data from the US, too, in the form of housing data. We hear anecdotally that houses and condos are selling like hotcakes in Florida. We get existing home sales on Friday. We also get earnings this week and next from some big names, including Goldman Sachs, IBM, J&J, and UnitedHealth Group on Tuesday alone, according to Wall Street in Advance.

We like to contrast Yellen's discussion of the puzzling and mysterious absence of inflation, and her assertion that it can come to a swift end, with the data provided by Econoday. At G-30 yesterday, Yellen repeated the economy is in good health and warrants inflation meeting the 2% benchmark. The evidence? "The American economy added an average of 171,000 jobs per month during the first eight months of the year, a little lower than the monthly average of 187,000 in 2016, but well above the growth of the working-age population. Reported employment shrank in September for the first time in seven years, but that is most likely the result of Hurricane Irma, which hit Florida while the government was conducting its monthly survey. Ms. Yellen said the damage from recent storms, while ‘terrible,' was unlikely to leave a lasting imprint on the economy. ‘History suggests that the longer-term effects will be modest and that aggregate economic activity will recover quickly.'"

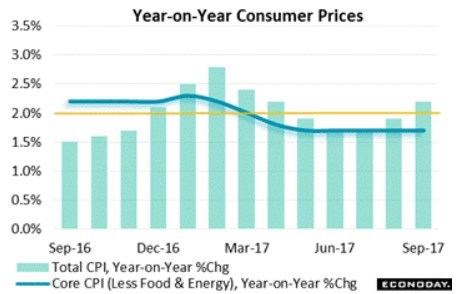

But employment and investment and increased exports are not inflation. Inflation is the only thing that is inflation. Using other data sets to substitute for inflation is double-talk. Consider the Econoday data. The 3-month average for core inflation is 0.16% and that's the best since February. On the year-over-year basis, "the core rate didn't accelerate at all, holding at the 1.7 percent line for the 5th month in a row. Note the Fed's target is tied to its own inflation index, not the CPI, but let's not quibble." See the chart.

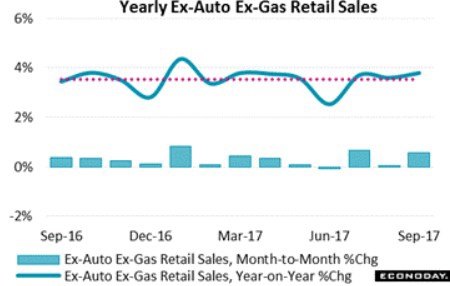

Retail sales looked strong in September, up 1.6% for the biggest gain in 2-1/2 years. "The main reason though is hurricane effects: replacement demand for autos and price-inflated sales at gasoline stations. Yet even with September's spike, growth in total retail sales has been no better than flat over the past year, trending at the 0.4 percent monthly line. Yet 0.4 percent over 12 months makes for a nearly 5 per-cent annual rate.

"But when stripping out autos and gasoline sales, 2 components that can distort the underlying picture, retail sales don't come in at the 5 percent line at all but just below 4 percent as tracked in the blue line of the graph and the red trend line. The graph's columns track monthly change which did come in at a very solid 0.5 percent in September. Restaurant sales were a key plus though the strength here follows a run of weakness in prior months. Trends for most subcomponents are in fact flat at moderate rates of growth."

This data is as flat as it can get without scaring the horses. To see an imaginary uptick in retail sales and inflation from this data is delusional. Granted, Yellen is a fine economist and the hundreds of Fed economists beavering away in the back room may have some undeclared reason to believe inflation is coming, but the chances are good that this deduction is based only on modelling. The data do not back it up, at least not so far. In a way, we are waiting for the little boy to shout "the emperor has no clothes."

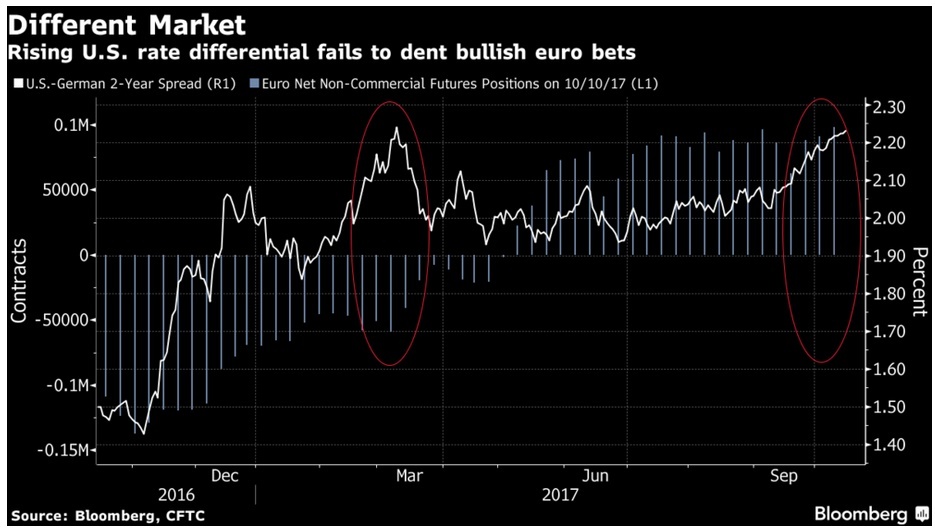

If we were not so entranced by Trump's ridiculous distractions and political shenanigans all over the place, including mishandling of Brexit by all sides, we would be in wonderment over the euro's persis-tence. We are getting a correction now, but the euro is still well above where differentials indicate it should be. The two year spread is wider and nearing the March peak, according to BBH's Chandler, quoted in Bloomberg. Here's the thing: "The rise in the differential was associated with bearish bets a year ago, but now it comes with bullish wagers.

"Euro long positions in the futures market are around 98,000 contracts -- a year ago, speculators were net short 100,000 plus." The euro longs are the highest since May 2011. ABN Amro is not alone in pre-dicting a profit-taking wave. This won't reverse the trend, but as we wrote last week, can put a big dent in it.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.82 | SHORT USD | 10/15/17 | NEW*WEAK | 111.82 | 0.00% |

| GBP/USD | 1.3295 | SHORT GBP | 10/03/17 | WEAK | 1.3247 | -0.36% |

| EUR/USD | 1.1792 | SHORT EURO | 09/27/17 | WEAK | 1.1741 | -0.43% |

| EUR/JPY | 131.86 | SHORT EURO | 10/15/17 | NEW*WEAK | 131.86 | 0.00% |

| EUR/GBP | 0.8869 | SHORT EURO | 09/13/17 | WEAK | 0.9033 | 1.82% |

| USD/CHF | 0.9762 | LONG USD | 09/25/17 | WEAK | 0.9732 | 0.31% |

| USD/CAD | 1.2500 | LONG USD | 09/27/17 | WEAK | 1.2389 | 0.90% |

| NZD/USD | 0.7186 | SHORT NZD | 10/06/17 | STRONG | 0.7088 | -1.38% |

| AUD/USD | 0.7872 | SHORT AUD | 09/25/17 | WEAK | 0.7963 | 1.14% |

| AUD/JPY | 88.02 | SHORT AUD | 10/11/17 | WEAK | 87.35 | -0.77% |

| USD/MXN | 19.0167 | LONG USD | 09/22/17 | STRONG | 17.8066 | 6.80% |

| USD/BRL | 3.1449 | LONG USD | 09/27/17 | WEAK | 3.1670 | -0.70% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat