US economy: Recovery without the Trump push? Why not?

Outlook:

The dollar has a chance, a slim one, of repeating yesterday's performance, however brief. GDP this morning has to be wonderful for the effect to become more than a blip. The WSJ survey gets a forecast of 2.7%, with some going all the way to 3% (from 1.4% in Q1). Let's not forget that Q1 started out at well under 1% and was revised three times to get to 1.4%.

But look again at durables. It failed to have a lasting effect in part because while the headline number was very good at 6.5%, the components say something else. Ex-transportation, orders rose a mere 0.2%. Nondefense capital goods ex-aircraft, the standard proxy for capital spending, FELL 0.1% for the first drop since December.

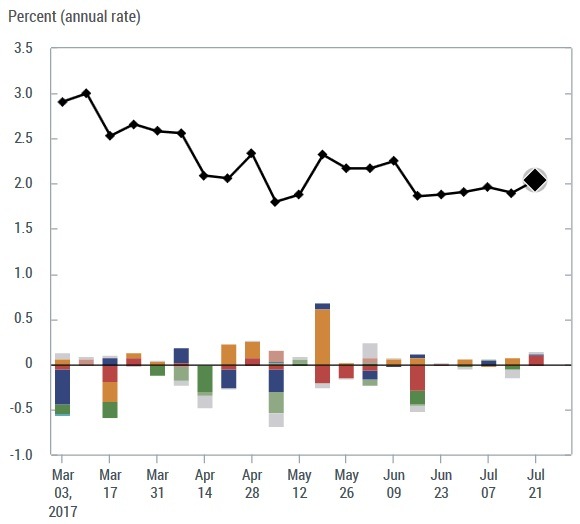

GDP today is the first official version. The Atlanta Fed has been reporting its forecasts for some time now and yesterday boosted the estimate to 2.8% (from 2.7%--it's those inventories again). Meanwhile, Bloomberg also has 2.8% and Reuters has 2.6%. Cold water--the New York Fed gets 2.04% as of July 21. That sounds discouraging but see the chart—it looks like a bottom is forming and the chances or re-covery are not zero. Recovery without the Trump push? Why not? The US economy is resilient About a high GDP number this morning, a Markit economist told the WSJ that forecasters should calm down. "The economy is on a 2% growth path...the same path it's been on since 2010. The economy is nearing full employment and so we're not going to see surges in growth because we just don't have the labor force to make that happen."

Not to diss the excellent economists at Markit, but poppycock. The US has a ton of people unemployed or underemployed who can be induced to re-enter the workforce under the right conditions. That in-cludes decent wages, jobs with benefits (including healthcare), and decent working conditions, which in some cases might include the ability to form unions. One of the issues is a lack of skilled workers or at least skilled workers in the right locations. American labor mobility has been on a decline so some time, and labor mobility is often named as one of the key virtues of an efficient labor market. Unfortu-nately, the falling supply of houses plus rising prices has a tendency to prevent labor mobility, even if we see the housing market as a stand-alone to be recovering from the crash. This is called a pinball ef-fect and it can ricochet far and wide.

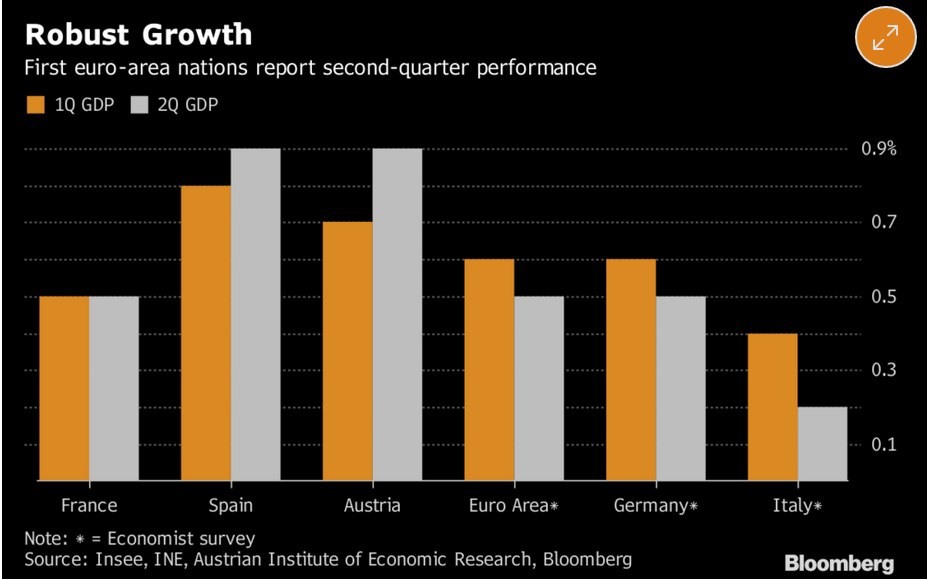

Meanwhile, nothing stands alone. Everything has to be judged in comparison to something else. US growth might improve considerably and the trajectory of US GDP may have bottomed and turned up-ward, but there's no "maybe" about Europe. See the Bloomberg chart. And for the third time, France got 1.8%. It seems as though Europe is already there. That means next week we will be talking about ECB tapering again and reconsidering the Fed. For the tide to turn in favor of the dollar will take quite a strong showing today.

Tidbits: "They're rioting in Africa, they're starving in Spain..." Lyrics from an old song can get stuck in your head. The ending is "and I don't like anybody very much." The world is not exactly going to hell in a handbasket, but we are getting stories that evoke earlier days. The Pakistani head of state was just indicted for corruption, the main outcome of the Panama Papers scandal.

Venezuela goes to the polls on Sunday to override the constitution with a "constituent assembly" that can override all other institutions and laws. In a word, dictatorship. The US ordered all the embassy families to leave the country.

So far two failed states are not contaminating the rest of the emerging markets.

Politics: The Senate again failed to pass even the skimpiest repeal-and-replace healthcare bill. Nobody had seen its contents ahead of time and the CBO had not done a cost/benefit analysis. Two lady sena-tors and McCain were the decisive votes. Earlier McCain had said Congress is not Trump's lapdog. Bravo.

The whole thing is disgraceful as well as bonkers. Earlier, Trump sent a minion to a senator saying her state (Alaska) could be singled out for retaliation by withholding federal funds if she persisted in voting against the bill. This is precisely the unethical and illegal behavior that got three of NJ Gov Christie's staff sent to jail. Trump's ignorance and unwillingness to learn legal and standard norms and practices is appalling. His latest appointment is a hedge fund jerk who has uses vulgar language to threaten vari-ous people, in some cases without bothering to get facts. This is a guy who is not even if office yet. First he has to sell his company—to the Chinese. Wonder what perks they expect to get?

What outrage is next? Trump needs a steady diet of distractions from the incompetence and dysfunc-tionalty of his presidency. Trade was always going to be a recurring theme and this time Japan may get the spotlight. Japan raised the tariff on frozen beef from the US (and Canada and NZ) from 38.5% to 50%, to start Aug 1. In the absence of a trade deal, Japan is allowed to do that if it deems imports rising too much. The WSJ reports "Recently, frozen beef imports from the U.S. have been on the rise, partly because Japanese importers likely sought to secure the meat before China resumes U.S. beef imports as a part of a trade deal..." Last year, the US exported $1.5 billion of beef to Japan.

Trump is notoriously thin-skinned. Get ready, Mexico.

To be fair, off on the side and not getting much press, the House of Representatives rejected the Trump Border Adjustment Tax. The BAT was supposed to fund The Wall along the Mexican border as well as other aspects of still-undefined tax reform. Assuming BAT is rejected in the Senate, too, that will leave the executive's ability to break trade agreements at will, although he is supposed to have a national se-curity basis for doing so.

The showdown would then be between the president and the Commerce Dept. Well, Trump has picked fights with the Justice Dept, why not Commerce? This would put Commerce Sec Ross in a confronta-tional position with the president. Ross may not be much liked but nobody thinks he is stupid or unpat-riotic. Imposing tariffs on Mexico if BAT gets shot down would be petty and would be political. Ross knows the oath he took is to the Constitution and the best interests of the people, not to Trump person-ally. Trump doesn't know that, or if he knows it, does not accept it. Ross knows his own reputation is on the line and Ross is no spring chicken. So, oddly, it could be Ross's Commerce Dept and not the FBI or Justice who challenges the jerk in the White House.

Stay tuned. We expect something this weekend, possibly Trump firing the attorney general.

| Currency | Spot | Current Position | Signal Date | Signal Strength | Signal Rate | Gain/Loss |

| USD/JPY | 111.18 | SHORT USD | 07/19/17 | WEAK | 111.96 | 0.70% |

| GBP/USD | 1.3084 | LONG GBP | 06/28/17 | WEAK | 1.2701 | 3.02% |

| EUR/USD | 1.1714 | LONG EURO | 06/28/17 | STRONG | 1.1218 | 4.42% |

| EUR/JPY | 130.23 | LONG EURO | 06/27/17 | WEAK | 125.73 | 3.58% |

| EUR/GBP | 0.8955 | LONG EURO | 04/25/17 | STRONG | 0.8490 | 5.48% |

| USD/CHF | 0.9703 | SHORT USD | 06/28/17 | WEAK | 0.9675 | -0.29% |

| USD/CAD | 1.2548 | SHORT USD | 05/17/17 | STRONG | 1.3621 | 7.88% |

| NZD/USD | 0.7475 | LONG AUD | 05/30/17 | STRONG | 0.7062 | 5.85% |

| AUD/USD | 0.7952 | LONG AUD | 06/08/17 | WEAK | 0.7548 | 5.35% |

| AUD/JPY | 88.41 | LONG AUD | 06/16/17 | WEAK | 84.65 | 4.44% |

| USD/MXN | 17.7569 | SHORT USD | 05/17/17 | STRONG | 18.7098 | 5.09% |

| USD/BRL | 3.1539 | SHORT USD | 07/17/17 | WEAK | 3.1794 | 0.80% |

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat