When are the FOMC minutes and how could they affect DXY?

The US FOMC minutes, of the July 31/August 1 meeting, will be released on Wednesday at 18:00 GMT. At that meeting, the FOMC, kept the Fed Funds rate target unchanged at 1.75% to 2.0%, in a unanimous decision.

Key notes

At the last meeting, the Fed kept rates unchanged as expected and left the doors open to two more rate hikes during 2018. The statement had no significant impact back then, and if the minutes offer no new information it could also be the case today. The current path of monetary policy is for gradual rate hikes. So far, trade war tensions and concerns about emerging-markets have not affected monetary policy expectations. Recently President Donald Trump criticized the Federal Reserve for rising interest rates.

“Given that it was a meeting with almost nothing material to come from it, the minutes are unlikely to throw up much of interest, although our US economists noted that this could present the opportunity for the Fed to discuss longer-term issues, potentially including discussion around the balance sheet and the implementation of monetary policy (e.g. floor v corridor system), especially given the speech from NY Fed Markets Group chief Simon Potter immediately following the FOMC meeting earlier this month”, wrote Deutsche Bank analysts.

The US central bank is expected to deliver two more rate hikes this year: one at the next meeting in October and the other in December. Regarding today’s minutes, analysts at Danske Bank, are more interested in any discussions on how long to continue shrinking the balance sheet and the future monetary framework.

Overall, most analysts do not expect much from today’s minutes. Without surprises, they will focus on clues of the medium to long-term monetary policy trajectory, given that in the short-term, no change is seen, at least for a few months.

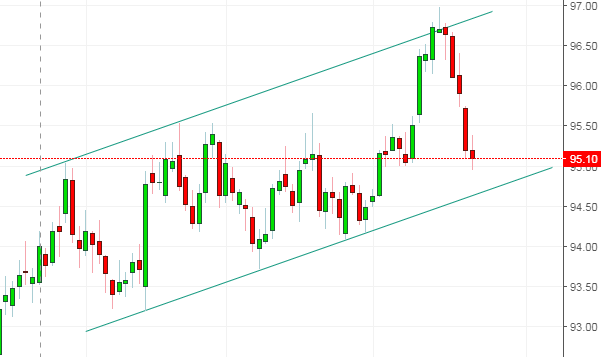

Implications for DXY

The US Dollar Index is falling today for the sixth trading day in a row. The decline started the same day it peaked at 97.00 (Aug 15), the highest level since June 2017. Since then it has fallen almost 2% making a correction that it is starting to look more like a reversal.

It would need very hawkish minutes to push the greenback to the upside. Under that scenario, DXY could rise back above 95.50 recovering the bullish tone. Above the next resistance levels might be seen at 96.10 and 96.40. Considering the oversold extreme readings in many USD crosses, an upside correction seems likely ahead of the Asian session.

A cautious tone from the Fed could add more fuel to the slide of the greenback. To the downside, the key support is seen at 94.60 (uptrend line). A close below that area would signal more losses ahead. A potential target is seen at 92.50 but before that level, supports are seen at 94.00 and 93.30. If the DXY manages to hold on top of 94.60, a rebound seems likely, particularly taking into account the sharp slide of the previous days.

About the FOMC minutes

FOMC stands for The Federal Open Market Committee that organizes 8 meetings in a year and reviews economic and financial conditions, determines the appropriate stance of monetary policy and assesses the risks to its long-run goals of price stability and sustainable economic growth. FOMC Minutes are released by the Board of Governors of the Federal Reserve and are a clear guide to the future US interest rate policy.

Author

Matías Salord

FXStreet

Matías started in financial markets in 2008, after graduating in Economics. He was trained in chart analysis and then became an educator. He also studied Journalism. He started writing analyses for specialized websites before joining FXStreet.