What will the Q3 earnings season show?

Here are the key points:

-

For 2025 Q3, total S&P 500 index earnings are expected to be up +5.2% from the same period last year on +6.0% higher revenues.

-

The positive revisions trend makes the overall setup for the Q3 earnings season favorable, but it raises the odds of actual results coming up short of expectations. In other words, it is reasonable to worry whether expectations for the period are too high, particularly for the Tech and Finance sectors.

-

Excluding the Tech sector contribution, Q3 earnings for the rest of the S&P 500 index would be up only +2.2% (vs. +5.2% otherwise).

-

For the Magnificent 7 group, Q3 earnings are expected to be up +12.1% from the same period last year on +14.6% higher revenues, which would follow the group’s +26.4% earnings growth on +15.5% revenue growth in the preceding period.

Are Q3 earnings expectations too high?

As we have consistently highlighted in recent weeks, the overall revisions trend remains positive, with estimates for the back half of the year steadily going up.

For 2025 Q3, the expectation is for earnings growth of +5.2% on +6.0% revenue gains. We have consistently shown in this space how Q3 estimates have steadily increased since the quarter began.

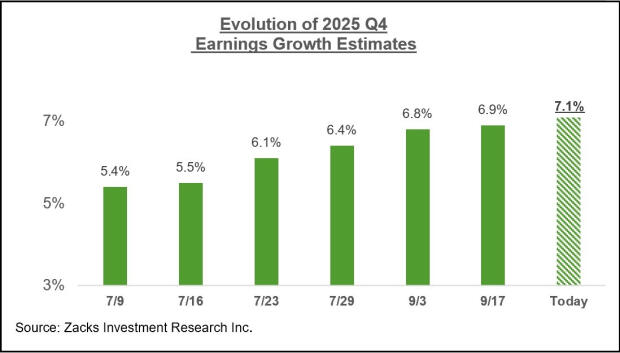

A comparable trend has been at play with respect to estimates for the last quarter of the year, when S&P 500 earnings are expected to increase by +7.1% on +6.7% higher revenues. The chart below shows how Q4 estimates have evolved over the last couple of months.

Image Source: Zacks Investment Research

Some of the same sectors that have been enjoying a favorable revisions trend for Q3 are in play for Q4 as well, particularly the Tech, Finance, and Energy sectors.

JPMorgan (JPM - Free Report) and Wells Fargo (WFC - Free Report) will kick off the Q3 earnings season for the Finance sector on October 14th. While Q3 estimates for Wells Fargo have barely moved higher, those for JPMorgan have clearly increased lately. A comparable trend is at play for JPMorgan and Wells Fargo for 2025 Q4 as well.

The earnings big picture

The chart below shows expectations for 2025 Q3 in terms of what was achieved in the preceding four periods and what is currently expected for the next three quarters.

Image Source: Zacks Investment Research

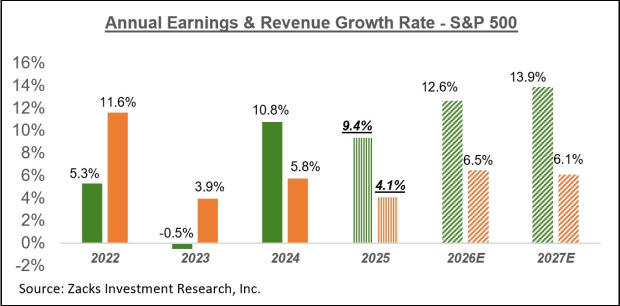

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

Image Source: Zacks Investment Research

The aforementioned favorable revisions trend validates the market’s rebound from the April lows. It will be interesting to see if this positive revisions trend will remain in place as we get into the Q3 reporting cycle.

The robust recent results from Oracle and Micron suggest that the trend can continue. But we have to keep in mind that the profitability strength from these Tech players primarily reflects developments in the artificial intelligence space that were already being credited for the Mag 7 group’s prominence. It remains to be seen whether the favorable trend will be reflected in non-tech areas of the economy.

Stay up to date with what's moving and shaking on the world's markets and never miss another important headline again! Check ActivTrades daily news and analyses here.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.