Wake Up Wall Street (SPY) (QQQ): Walmart reassures, Home Depot inventories a concern, but market flatlines

Here is what you need to know on Tuesday, August 16:

Equity markets continued their ascent on Monday in the face of some less than stellar economic data. The New York Fed survey was bad, really bad, Great Financial Crisis bad. At least prices paid did confirm the CPI data, but overall it was not a positive report. Overnight from China, some news about possible moves to insure bondholders in the property sector is not positive and is helping keep a lid on European equities and US futures.

Meme stock momentum began to slow on Monday, which may be a sign that the recent return of the day trader could begin to slow and from their sections of the market begin to stall. For now though big tech remains the place to be as Apple and Tesla run into big resistance levels. Both stocks gained on Monday and helped the main indices close just in the green. Walmart has just come out with earnings in line with a slight beat on revenue, but the most important metric is maintaining guidance for the remainder of the fiscal year, a big plus, and WMT stock is up in the premarket.

Bond yields remain under pressure, but in a so far overlooked development the MOVE index of bond volatility spiked a bit yesterday on the back of the poor economic data. That has been a portent of doom for equity markets this year, so stay tuned. Technically though, the equity market is getting into some decent resistance with the 200-day moving average nearby on the S&P 500, and SPY is now overbought on the Money Flow Index (MFI) and the Relative Strength Index (RSI).

SPY daily

Oil has moved lower on the back of renewed fears of a recession, not only in the US but globally. Weak US data and fears over the China property bubble have tracked oil back to $89.40 for WTI. Gold is at $1,776, and Bitcoin is flat at $24,100. The dollar index is a tad stronger this morning at $106.85.

European markets are higher: Eurostoxx: flat FTSE +0.3% and DAX +0.5%

US futures are flat, totally flat for Dow, Nasdaq and S&P, come back tomorrow!

Wall Street top news (SPY) (QQQ)

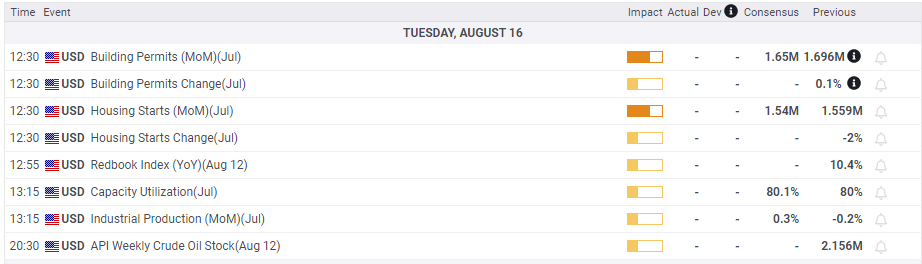

US Housing starts lower than forecast: 1.446m versus 1.53m forecast.

Walmart (WMT) beats on earnings and maintains FY guidance.

Genius Sports (GENI) beats on earnings.

Sea Limited (SE) drops on average earnings and no guidance.

Apple (AAPL): Bloomberg reports that is let go of contracted recruiters.

American Airlines (AAL) cuts November schedule by 16%.

AstraZeneca (AZN): UK stops buying covid drug Evushield on concerns over efficacy versus new variants.

Home Depot (HD) beats on earnings, maintains guidance, but inventory is higher than expected.

Ally Financial (ALLY): Berkshire Hathaway increases stake.

ZipRecruiter (ZIP) down despite strong earnings.

BHP up on strong earnings as mineral prices boost profit.

Nu Holdings (NU) up on strong earnings.

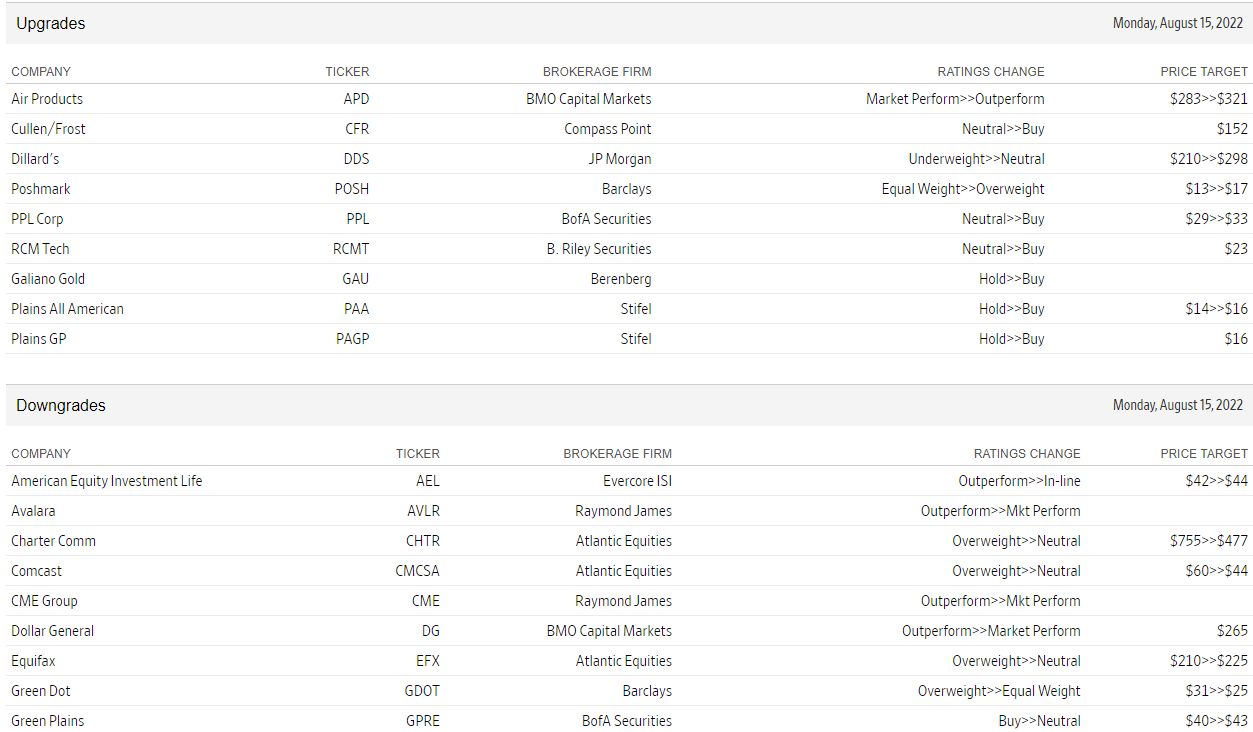

Upgrades and downgrades

Source: WSJ.com

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.