Wake Up Wall Street (SPY) (QQQ): Fed hikes, BOJ intervenes and equities look lower

Here is what you need to know on Thursday, September 22:

Wow, things are getting busy around here. It is central bank week, and so far it is hikes as far as the eye can see. First up, the Fed duly raised rates by 75 basis points last night and surprised markets with the dot plot of future rates. This shows no cuts in 2023 and perhaps a modest increase. This was at least 50bps higher than interest rate markets had been predicting and led to an immediate crash in risk assets. However, once the press conference Q&A began equities took some hope from more restrained talk before selling off again into the close.

Next up the Bank of Japan did nothing on the interest rate front but did intervene to halt the inexorable rise in the dollar. This is likely to only provide some short-term relief as no other central banks are on board. The Bank of England went all lovey-dovey in going for 50bps as the hoped-for energy price cap will put a lid on inflation. The Swiss National Bank also went for a 75 basis point hike.

Where equities trade from here is likely lower, but in the short term we may get a positioning rally as everyone was a tad bearish. Overall, things are getting harder and harder for equity valuations as TINA is dead now with rates heading for 5%. Bitcoin though is 3% higher this morning, reinforcing our short-term bounce thesis. I mean very short term like the rest of this week! Attention will now begin to look ahead toward third quarter earnings. Since last time out the dollar has continued higher and economic conditions have worsened, so this is likely to be a challenging season.

Oil is higher at $85, and Bitcoin is at $19,200, up 4% now. Gold is trading at $1,681, while the dollar index is lower at 110.68.

European markets are mixed: Eurostoxx +1%, FTSE +0.6% and DAx -0.6%.

US futures are higher: S&P flat, Dow +0.1% and Nasdaq is flat.

Wall Street Top news (SPY) (QQQ)

Fed hikes rates 75 bps and sees higher rates for longer.

Bank of Japan intervenes in FX market to support Yen, selling dollars.

Bank of England hikes rates 50bps.

Swiss National Bank hikes rates 50 bps.

Royal Caribbean (RCL) announces note offering.

Target (TGT) to hire 100k workers for the holiday season, same as 2021.

Costco (COST) earnings after the close.

Darden Restaurants (DRI) revenue misses but restates guidance.

American Tower (AMT) increases dividend to $1.47 per share.

Ideanomics (IDEX) files for a secondary offering.

LiAuto (LI) to host an early launch event for L8 premium car on September 30.

Tilray (TLRY) gets Italian approval for distrubution of THC25.

Accenture (ACN): EPS beats, revenue in line.

Honda Motors to reduce car output by 40% at two Japanese plants by up to 40% in October due to supply chain issues-Reuters.

Toyota plans to produce 100k less vehicles in October due to semiconductor chip shortages. Reuters.

Salesforce (CRM) announced plans to operate more efficiently.

Eli Lilly (LLY): FDA approves Retevmo for new uses.

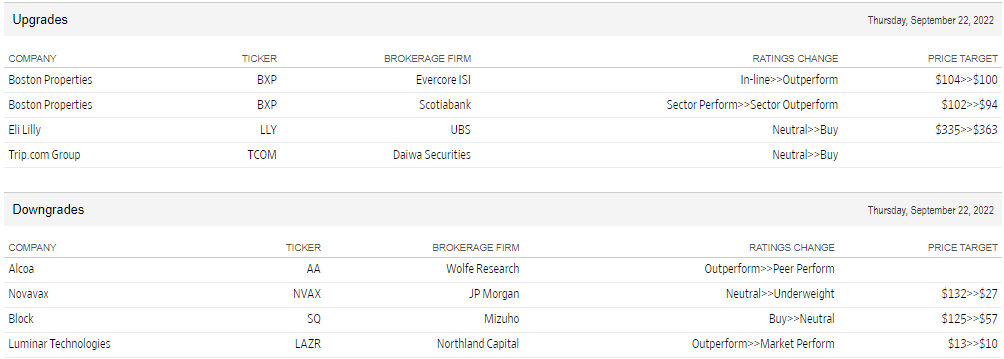

Upgrades and downgrades

source: WSJ.com

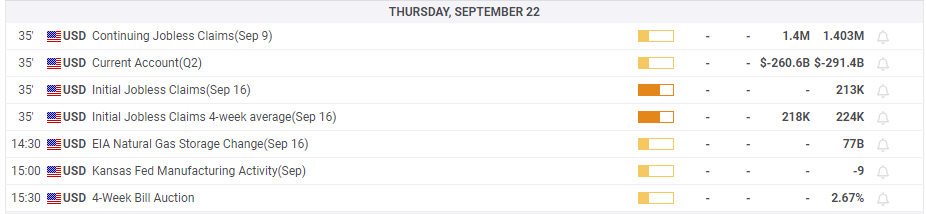

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.