Traditional IRA vs Roth IRA: Understanding the differences to make the right choice

With the proliferation of retirement planning options in the United States, the choice between the types of Individual Retirement Accounts (IRA), mainly a Traditional IRA or a Roth IRA, remains one of the most common dilemmas. While both offer tax advantages, they do so in very different ways.

This article offers a comparison of these two account types to help everyone make an informed decision, tailored to their personal situation.

The decisive factor: Taxation... but when?

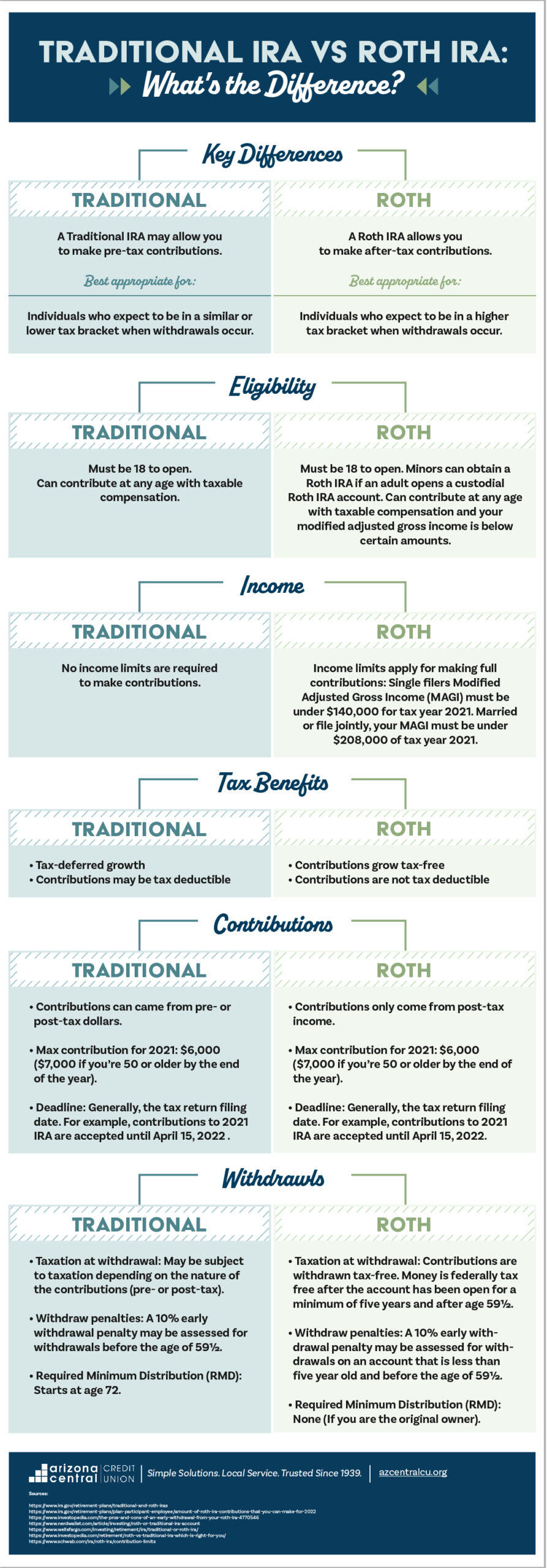

The main distinction between a Traditional IRA and a Roth IRA lies in the timing of the tax advantage.

With a Traditional IRA, contributions are generally tax-deductible in the year they are made, reducing taxable income. On the other hand, withdrawals at retirement are taxed as ordinary income.

The Roth IRA, on the other hand, is funded with income that has already been taxed. It offers no immediate tax reduction, but future withdrawals, including earnings, are tax-free, provided certain age and account aging conditions are met.

This choice may also be influenced by other sources of retirement income, such as Social Security, which is taxed according to your overall income. The type of IRA you choose can therefore have an impact on the amount of your net benefits.

Eligibility conditions and income limits

Access to these accounts is not identical. A Traditional IRA is open to anyone with income, with no income limit. However, tax deductibility may be restricted if you are already covered by a company retirement plan and your income exceeds certain thresholds.

The Roth IRA is however reserved for taxpayers below a certain modified adjusted income level (MAGI). In 2025, the ability to contribute begins to decrease as early as $150,000 for a single person (with total elimination at $165,000), and as early as $236,000 for a married couple filing jointly (with total elimination at $246,000).

Withdrawal rules: Flexibility versus obligation

Traditional IRA withdrawals are permitted from age 59 and half, but taxed. Before that age, a 10% penalty applies, except for certain purposes (real estate purchase, medical expenses, disability, etc.). Required Minimum Distributions (RMDs) must begin at age 73 (or 75 for those born in 1960 or later), even if you don't need the funds.

With a Roth IRA, you can withdraw your contributions at any time, tax-free and penalty-free. However, earnings are tax-exempt only after five years and if you are at least 59 and half years old, or in specific cases (disability, death, first real estate purchase). There are no RMDs to pay during your lifetime, offering greater flexibility at the end of your life or when passing on an inheritance.

Contribution limits: Identical ceilings

For the 2025 tax year, the rules are the same for both Traditional and Roth IRAs:

- Maximum contribution: $7,000

- Catch-up contribution from age 50: $8,000

These limits are cumulative for all your IRAs (Traditional + Roth). It is possible to contribute to both types simultaneously, provided the total contribution does not exceed the overall annual limit.

Other criteria to consider

- Impact on aid and tax credits: A Traditional IRA, by reducing your taxable income, may improve your eligibility for certain credits (such as the child tax credit or the student interest rebate).

- Flexibility in times of need: The Roth IRA allows freer access to your pre-retirement contributions, which can be an advantage for younger workers or those without a safety net.

- Inheritance: The Roth IRA is often favored in estate strategies, as heirs also benefit from tax-free withdrawals, albeit subject to a distribution schedule.

- Finally, the combination of income from an IRA and Social Security can vary your effective tax rate at retirement. Good retirement planning can help you manage the cross-taxation of these two sources.

A personal decision, not a universal one

Neither the Traditional IRA nor the Roth IRA is inherently "better". The choice depends on your current income, your tax expectations for retirement, your need for short-term flexibility and your long-term wealth objectives.

And don't forget that withdrawals from a Traditional IRA can increase your taxable income, which could make a larger portion of your Social Security benefits taxable. Once again, your choice of account type will influence your overall tax situation in retirement.

Many people also choose to diversify by opening both types of accounts within the authorized limit.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.