Euro remains on the defensive and supported near 1.0920

- Euro's daily decline seems to have met initial support near 1.0920.

- Stocks markets in Europe remain weak on concerns around China.

- ECB I. Schnabel argued that inflation outlook is tilted to the upside.

- US markets are closed due to the Juneteenth holiday.

- Fed-ECB divergence remains in the centre of the debate.

- US NAHB next on tap in the US docket on Monday.

The European currency (EUR) maintains the offered stance well in place at the beginning of the week and motivates EUR/USD to recede to daily lows in the 1.0925/20 band on the back of the decent recovery in the US Dollar.

Indeed, sellers remain in control of the sentiment around the euro on Monday, forcing spot to give away part of last week’s gains to the 1.0970 region, or multi-week highs, as investors continue to adjust to the recent hawkish messages from both the European Central Bank (ECB) and the Federal Reserve at their meetings on June 14 and June 15, respectively.

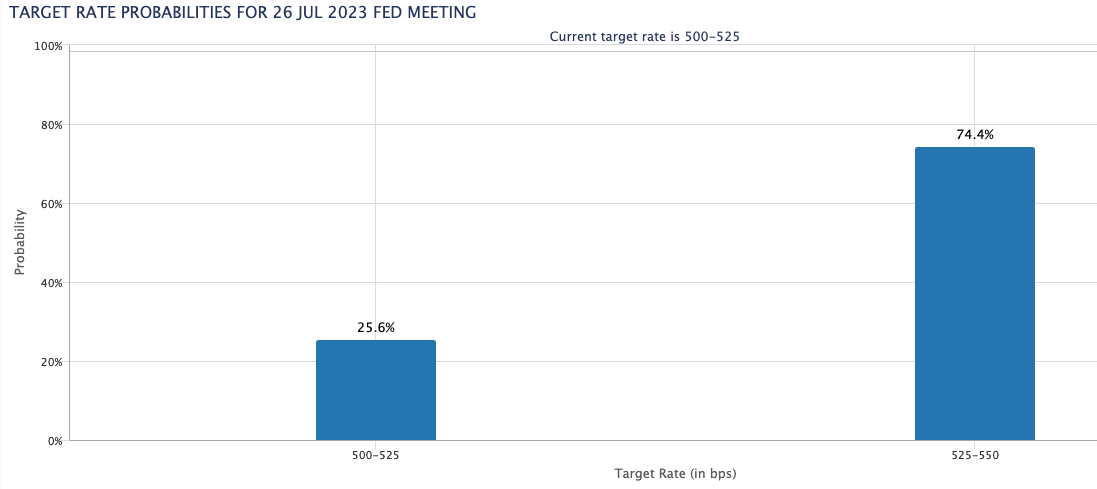

On the latter, it is worth mentioning that the ECB Christine Lagarde, as well as many of her colleagues at the Governing Council, already advocated for an extra quarter-point rate raise in July, while Chief Jerome Powell also left the door open to a similar move at the July 26 gathering. This scenario is favoured with nearly 75% of probability according to CME Group’s FedWatch Tool.

Still around the ECB, Board members I. Schnabel stressed that the inflation outlook remains tilted to the upside, while her colleague P. Lane suggested that another quarter-point rate hike in July looks approproate.

Changing the subject and looking at the latest CFTC positioning report, speculative net longs in the EUR dropped for the fifth consecutive week in the week ended on June 13 to around 151.8K contracts, as investors increased their prudence ahead of the key ECB meeting on June 15.

In the US data space, housing market will be in the limelight following the release of the NAHB Housing Market Index for the month of June.

Daily digest market movers: Euro could face some near-term consolidation

- The US Dollar flirts with the 55-day SMA near 102.50.

- Markets’ focus will likely be on the meeting between US A. Blinken and China's Xi Jinping.

- Fed’s J. Powell’s testimonies will be the salient events later in the week.

- ECB's G. Simkus deemed premature any talk regarding the September meeting.

- The ECB-Fed policy divergence remains the almost exclusive driver of the pair’s price action for the time being

Technical Analysis: Further upside keeps targeting 1.1000

The Euro (EUR) has retreated slightly from its new monthly high of 1.0970 reached on June 16. To make further gains, it needs to overcome this level quickly, which would allow it to potentially reach the psychological barrier of 1.1000. If it continues to climb, the next major resistance levels are the 2023 high of 1.1095 (April 26), followed by the round level of 1.1100, and then the weekly top of 1.1184 (March 31, 2022). The latter is supported by the 200-week SMA, which currently stands at 1.1181.

If the bears take control, there is a temporary support at the 55-day SMA at 1.0881. If this level is breached, there are no significant levels of support until the May low of 1.0635 (May 31) prior to the March low of 1.0516 (March 15) and the 2023 low of 1.0481 (January 6).

Interest rates FAQs

What are interest rates?

Interest rates are charged by financial institutions on loans to borrowers and are paid as interest to savers and depositors. They are influenced by base lending rates, which are set by central banks in response to changes in the economy. Central banks normally have a mandate to ensure price stability, which in most cases means targeting a core inflation rate of around 2%.

If inflation falls below target the central bank may cut base lending rates, with a view to stimulating lending and boosting the economy. If inflation rises substantially above 2% it normally results in the central bank raising base lending rates in an attempt to lower inflation.

How do interest rates impact currencies?

Higher interest rates generally help strengthen a country’s currency as they make it a more attractive place for global investors to park their money.

How do interest rates influence the price of Gold?

Higher interest rates overall weigh on the price of Gold because they increase the opportunity cost of holding Gold instead of investing in an interest-bearing asset or placing cash in the bank.

If interest rates are high that usually pushes up the price of the US Dollar (USD), and since Gold is priced in Dollars, this has the effect of lowering the price of Gold.

What is the Fed Funds rate?

The Fed funds rate is the overnight rate at which US banks lend to each other. It is the oft-quoted headline rate set by the Federal Reserve at its FOMC meetings. It is set as a range, for example 4.75%-5.00%, though the upper limit (in that case 5.00%) is the quoted figure.

Market expectations for future Fed funds rate are tracked by the CME FedWatch tool, which shapes how many financial markets behave in anticipation of future Federal Reserve monetary policy decisions.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.