The US Dollar (USD) continues to slide, posting its worst first-semester performance in nearly forty years, according to Bloomberg data reported by SMM.

While US President Donald Trump's re-election was initially seen as a supportive factor for the Greenback, recent developments reflect a very different reality: unstable trade policy, worsening fiscal imbalances and declining foreign demand for assets denominated in US Dollars are now weighing heavily on the US currency.

Is this recent weakness a short-term blip or an indication of the end of an era for King Dollar?

A historic downturn for the US Dollar

The current sequence of a falling US Dollar is unprecedented in its scale and speed. The US Dollar Index (DXY), which measures the currency against a basket of six foreign peers, has fallen by more than 10% since the start of the year, dropping towards 97 points for the first time since February 2022. This is the worst first half-year for the DXY in decades.

US Dollar Index H1 performance. Source: FXStreet

The movement is not confined to the currency markets. It reflects a broader recomposition of global capital flows in the face of persistent political and economic uncertainty in the United States.

"The dynamics observed in the foreign exchange market are a direct reflection of a crisis of confidence in US fundamentals and the stability of its economic governance," Barry Eichengreen, professor of economics at UC Berkeley, told CNN.

The paradoxical effect of Trump's policies

Initial expectations of a strengthening US Dollar were based on two pillars of US President Donald Trump's policies: fiscal stimulus via tax cuts, and tariff barriers supposed to boost the balance of trade. But these measures have had the opposite effect.

Variable-geometry announcements on tariffs – whether imposed, suspended or extended – have increased volatility and worsened the investment climate. The uncertainties generated by US trade policy have also diminished the appeal of the US Dollar as a safe-haven asset.

"We're seeing a significant drop in the safety premium traditionally associated with Dollar-denominated assets," notes Francesco Pesole, FX strategist at ING, according to CNN.

"The Dollar's status as a safe-haven currency is now being called into question", he adds.

Reallocation of capital flows

One of the most notable developments concerns cross-border capital flows. Several indicators, notably the cross-currency basis swap – a financial contract where two entities exchange an equivalent amount of principal in different currencies – point to a decline in demand for US Dollars on international markets, in favor of the Euro (EUR) and the Japanese Yen (JPY).

According to Goldman Sachs and BNP Paribas, European institutional investors, notably pension funds and insurers, have reduced their exposure to the US Dollar to historically low levels, notes SMM. At the same time, China has stepped up its sales of US Treasuries, reinforcing its strategy of reserve diversification.

"We are witnessing a systemic reallocation towards markets considered more predictable from a macroeconomic point of view. This reflects a paradigm shift in sovereign risk perception", notes Richard Chambers, Global Head at Goldman Sachs.

Increased vulnerability to structural imbalances

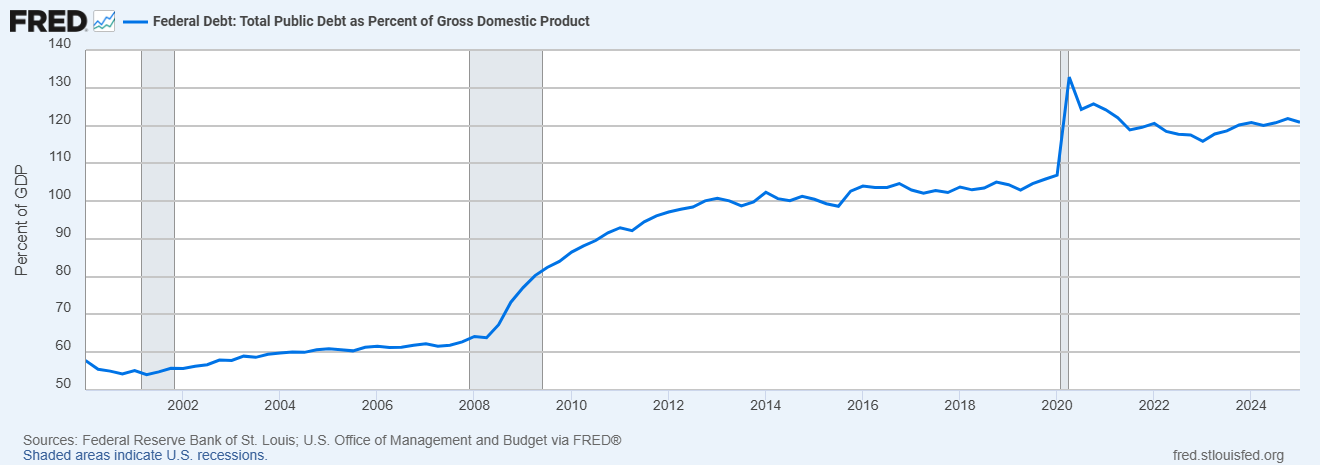

This phenomenon is amplified by concerns about the United States' fiscal trajectory. The public deficit exceeds 6.8% of GDP, and federal debt is now approaching $36,200 billion, or over 120% of GDP, according to Fed data.

Against this backdrop, Moody's downgraded the US sovereign rating to AA1 in May, citing structurally worsening deficits and rising interest costs.

Many investors are now demanding higher yields to finance US debt, mechanically increasing the cost of government and private-sector financing.

Global rebalancing accelerates

The fall in the DXY has benefited several currencies:

- The Euro has risen by 13% since January, reaching its highest level since 2021.

- The Japanese Yen, the Swedish Krona (SEK) and the Swiss Franc (CHF) also recorded significant gains over the period.

- In Asia, the Taiwanese Dollar (TWD), the Korean Won (KRW) and the Thai Baht (THB) posted gains of between 6% and 12%.

EUR, CHF, JPY and SEK performances against USD. Source: FXStreet

These movements reflect a change in perception regarding the relative economic stability of regional blocs, but also a heightened anticipation of future currency divergences.

What can we expect for the second half of the year?

The decline in the US Dollar during the first half of the year came despite the Federal Reserve’s decisions to keep interest rates high. But it doesn’t look like this will last much more: The Fed could make up to three rate cuts between now and the end of the year, according to market expectations, while the inflation, measured by the PCE index (2.3% in May), is closer to the Fed’s target of 2%.

If this monetary easing is not offset by credible deficit reduction or trade stabilization policies, the US Dollar could continue to depreciate in an orderly but sustained fashion.

According to Arun Sai, multi-asset strategist at Pictet AM, "Current conditions argue in favor of a further weakening of the US Dollar, barring a major overhaul of US fiscal policy", according to CNN.

A strategic turning point for the US Dollar

The US Dollar's decline in 2025 goes beyond a simple market correction. It reflects a structural repositioning of global investors and a rethinking of the fundamentals that have historically supported the central role of the Greenback.

The US currency remains dominant, but its systemic role could gradually be scaled back if the current risk factors, political instability, fiscal imbalances and loss of monetary credibility are not rapidly brought under control.

Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. FXStreet does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility. The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of FXStreet nor its advertisers. The author will not be held responsible for information that is found at the end of links posted on this page.

If not otherwise explicitly mentioned in the body of the article, at the time of writing, the author has no position in any stock mentioned in this article and no business relationship with any company mentioned. The author has not received compensation for writing this article, other than from FXStreet.

FXStreet and the author do not provide personalized recommendations. The author makes no representations as to the accuracy, completeness, or suitability of this information. FXStreet and the author will not be liable for any errors, omissions or any losses, injuries or damages arising from this information and its display or use. Errors and omissions excepted.

The author and FXStreet are not registered investment advisors and nothing in this article is intended to be investment advice.

Recommended content

Editors’ Picks

EUR/USD turns positive, targets 1.1450

EUR/USD now picks up pace and advances toward the 1.1440 region on Friday, up modestly for the day. With no major economic data due, lingering uncertainty over the US-Iran conflict keeps investors cautious, limiting the pair's upside.

USD/JPY recedes to four-day lows near 161.50

USD/JPY remains under bearish pressure as the week draws to a close, extending its decline further south of the 162.00 level. In the meantime, the Japanese Yen draws support from firm PPI data and announcements on fiscal and financial reforms in Japan.

Gold remains offered, still below $4,100

Gold struggles to extend Thursday’s rebound and navigates below the $4,100 mark per troy ounce on Friday. Uncertainty surrounding the Middle East conflict limits the precious metal’s upside, which is also under pressure amid rising US Treasury yields across the curve.

GBP/USD surrenders some gains, back to 1.3420

GBP/USD holds on to moderate gains above 1.3400 the figure on Friday. Optimism surrounding the UK government’s leadership transition and expectations of further BoE tightening support the British Pound, while easing tensions in the Middle East and fading Fed rate-hike expectations weigh on the US Dollar.

Week ahead – US CPI and Warsh testimony to take centre stage, BoC eyed too

US inflation report and Warsh testimony to headline the week. Dollar to dominate amid slew of other US data and Mideast tensions. Amid fresh Iran escalation, China GDP to shed light on Q2 impact. Bank of Canada not expected to follow RBNZ with rate hike.

Visa breaks higher after completing A-B-C correction, wave five targets new highs

Visa has delivered a very clean and almost textbook retracement from the 2025 highs. The decline unfolded as a clear three-wave A-B-C correction, reaching the 293–300 support zone, where we were looking for the completion of the pullback and a reaction from the previous gap area.