The Call Option

It is important that you understand how call options work before moving into more complex option definitions and advanced trading strategies.

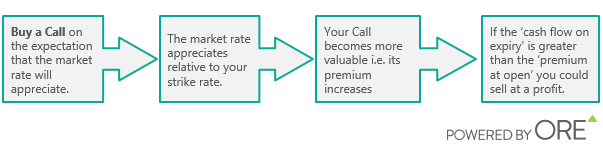

A Call gives the holder the right, but not the obligation, to buy at an agreed upon price up until expiry.

The agreed sell/buy price available to an option holder is called the strike rate. An option buyer will benefit if the strike rate can beat the market! If you are holding a Call option, the strike will become more attractive as the market rises.

Let’s look at a scenario where the buyer (holder) of an option on the EUR/USD might buy a call option expiry in 7 days for the premium of 160 USD assuming the current strike price of the call option is at 1.2500.

It is important to note that the premium of a buy Call trade increases as the market rises. Why? Because the Call's strike rate becomes more attractive relative to the market rate.

For now, let’s look at two possible results for the buyer in the above scenario:

1. The market price for the EUR/USD goes above 1.2540 (break-even point) before 7 days expire: The buyer will sell the option at a higher premium and profit from the difference. If on expiry the rate is 1.2700, they make a profit from the difference between the cash flow at expiry and the premium at open equaling 300 USD, as seen below. Alternately, if you are the seller (writer) of the option in this case, you have lost 300 USD.

2. The market price does not go above 1.2540: The buyer is not going to exercise their option as option’s buyers have the right, but not the obligation, to exercise their options. So, even though the option buyer bought the option, they never have to exercise it! This means the buyer is out the value of the option premium and the seller gains the value of the option premium, in this case 160 USD. Unlike with the direct purchase of an underlying asset, options buyers are only obligated for paying the premium amount not the cost of the underlying asset until they exercise their options.

In the next lesson, I will explain in more detail buying Put options.

A Call gives the holder the right, but not the obligation, to buy at an agreed upon price up until expiry.

The agreed sell/buy price available to an option holder is called the strike rate. An option buyer will benefit if the strike rate can beat the market! If you are holding a Call option, the strike will become more attractive as the market rises.

Let’s look at a scenario where the buyer (holder) of an option on the EUR/USD might buy a call option expiry in 7 days for the premium of 160 USD assuming the current strike price of the call option is at 1.2500.

It is important to note that the premium of a buy Call trade increases as the market rises. Why? Because the Call's strike rate becomes more attractive relative to the market rate.

For now, let’s look at two possible results for the buyer in the above scenario:

1. The market price for the EUR/USD goes above 1.2540 (break-even point) before 7 days expire: The buyer will sell the option at a higher premium and profit from the difference. If on expiry the rate is 1.2700, they make a profit from the difference between the cash flow at expiry and the premium at open equaling 300 USD, as seen below. Alternately, if you are the seller (writer) of the option in this case, you have lost 300 USD.

2. The market price does not go above 1.2540: The buyer is not going to exercise their option as option’s buyers have the right, but not the obligation, to exercise their options. So, even though the option buyer bought the option, they never have to exercise it! This means the buyer is out the value of the option premium and the seller gains the value of the option premium, in this case 160 USD. Unlike with the direct purchase of an underlying asset, options buyers are only obligated for paying the premium amount not the cost of the underlying asset until they exercise their options.

In the next lesson, I will explain in more detail buying Put options.

Author

Davina Becker is a Product Specialist at ORE with over 10 years of experience in the financial markets.

More from Davina Becker